Unlock the Answer: how long can the irs collect back taxes

When you’re staring down a mountain of tax debt, the most pressing question is often the simplest: how long can the IRS actually come after me for it? The answer, in most cases, is 10 years. This time limit is governed by a critical deadline called the Collection Statute Expiration Date (CSED), but there's a common misconception about when that 10-year clock starts ticking.

It doesn’t start when you miss the April filing deadline or even on the last day of the tax year in question. Instead, it all hinges on one specific date: the day the IRS officially assesses your tax liability.

Understanding the IRS 10-Year Collection Clock

Think of the assessment date as the moment the starting gun fires on the 10-year race. It's the day the IRS officially logs your tax debt into its books, making it a legal, collectible liability. Until that happens, the clock can't begin to run.

This is a crucial detail that can completely change your financial outlook and the timeline for getting your tax problems behind you. Getting this date wrong is one of the most common mistakes taxpayers make.

Pinpointing Your Assessment Date

So, how do you know when your assessment date is? It’s not always obvious, but it generally happens in one of a few ways:

- When You File a Return: For most people, this is straightforward. You file your tax return, and shortly after, the IRS processes it and officially records the tax you owe. That becomes your assessment date.

- When the IRS Files for You: If you don't file, the IRS won't just forget about you. Eventually, they will create a Substitute for Return (SFR) on your behalf using data from your employer or clients. The date they assess the tax from that SFR is when your 10-year clock begins.

- After an Audit: Let's say you get audited and the IRS finds you owe more. The date they assess that new, additional tax liability starts a separate 10-year clock just for that added amount.

The bottom line is this: No matter how the debt came about, the 10-year collection clock is always tied to a specific assessment date. Without one, the collection period is stuck in limbo, which is exactly why ignoring unfiled returns is a terrible strategy.

To make this clearer, let's break down the key events that lead to your CSED.

Your IRS Collection Timeline at a Glance

This table breaks down the key dates involved in the IRS collection process to help you pinpoint when your 10-year clock actually starts.

| Key Event | What It Means for You | Impact on the 10-Year Clock |

|---|---|---|

| Tax Year Ends | December 31 for most individuals and businesses. | None. This date is just the end of the accounting period. |

| Tax Filing Deadline | Typically April 15. This is the due date for your return. | None directly, but missing it can lead to an assessment. |

| Assessment Date | The IRS officially records your tax liability. | This is the official start date. The 10-year countdown begins now. |

| CSED | The Collection Statute Expiration Date. | This is the finish line. The IRS's legal authority to collect expires. |

Understanding these distinctions is the first step toward gaining control over your tax situation.

A Real-World Michigan Example

Let’s put this into perspective. Imagine you're a Detroit-based contractor who fell behind on taxes from 2015. You finally filed that overdue return, and the IRS officially assessed the tax on November 15, 2015.

That’s your starting line. The IRS now has exactly 10 years from that date to collect what you owe, which puts your Collection Statute Expiration Date (CSED) on November 15, 2025. Once that date passes, their legal power to levy your bank account, garnish your wages, or seize your property for that 2015 debt is gone.

But make no mistake—they will use every day they have. In a recent fiscal year alone, the IRS collected over $77 billion in unpaid taxes, proving they are relentless right up to the deadline. For a deeper dive into their methods, you can learn more about how the IRS collection process works from the experts.

While the CSED provides a clear finish line, the road to getting there isn't always a straight shot. As we'll see, certain actions you take can pause or even extend the clock, which makes understanding the full picture absolutely essential before you assume your debt is about to vanish.

When Does the 10-Year Collection Clock Never Start?

That 10-year collection rule feels like a light at the end of the tunnel, doesn't it? It offers a sense of finality, an eventual end to the stress of a tax debt. But what if that countdown never actually begins? It's a dangerous myth that the IRS will just forget about an old tax debt if you lay low long enough. In reality, a couple of specific situations can keep that 10-year clock from ever starting, leaving you in a state of permanent financial limbo.

If you don't understand these exceptions, you're playing with fire. Without a starting point for the collection clock, there can be no finish line. That means your wages, your bank accounts, and your future are on the table indefinitely until you finally take action to get right with the IRS.

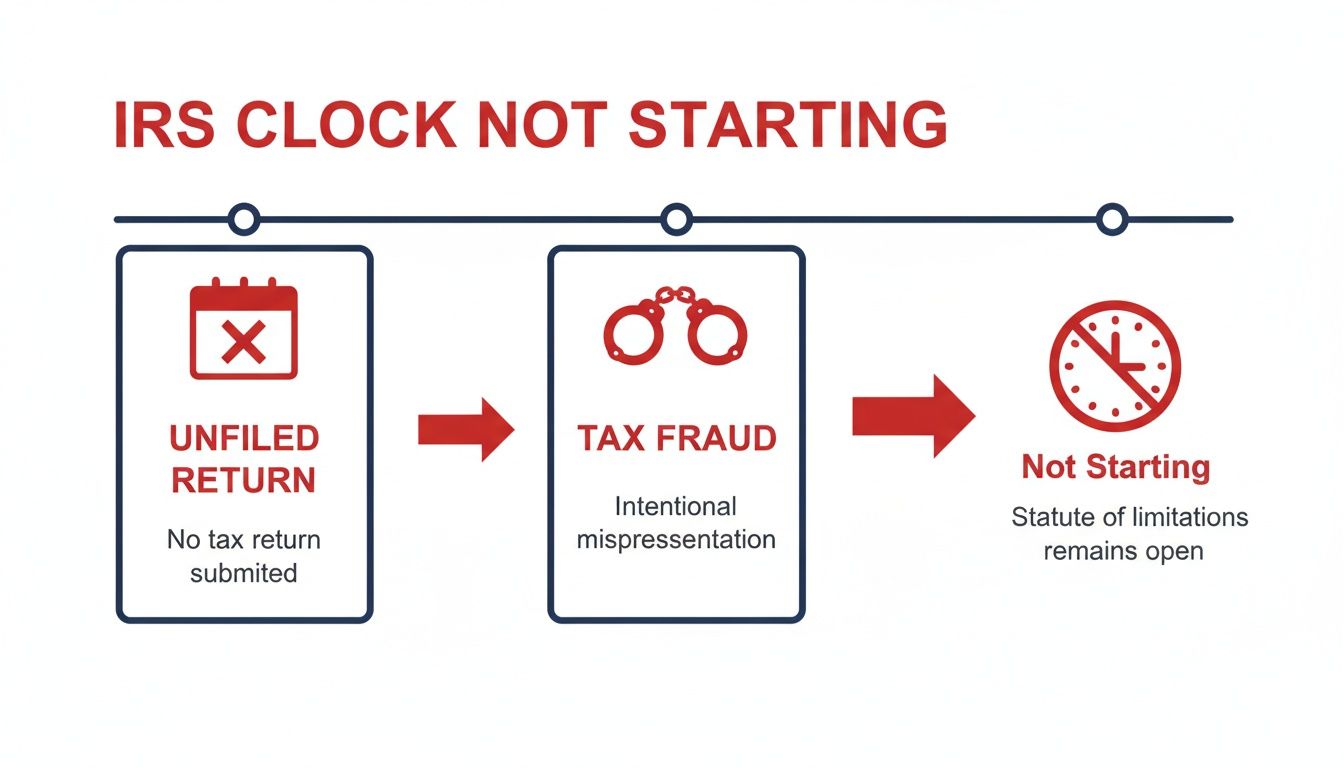

The Unfiled Tax Return Trap

The most common reason the 10-year clock never gets going is shockingly simple: you never filed a tax return. The whole process is built around the "assessment date," which is the day the IRS officially logs your tax bill into its system. But if you never file a return, the IRS has nothing to assess in the first place.

Think of it this way: the 10-year collection period is a race, and the assessment date is the starting pistol. Filing your return is what allows the IRS to fire that pistol. Until you file, the race against your tax debt can't even begin, leaving you exposed to collection action whenever the IRS finally catches up to you.

This puts taxpayers in a truly precarious spot. Imagine you’re a contractor in Oakland County who never filed your 2014 taxes. A decade has passed, but that means nothing to the IRS. Because you didn’t file, the collection statute never started. At any point—next week or next year—the IRS can create a Substitute for Return (SFR) for you, officially assess the tax, and then start their 10-year collection window. This is a huge reason the national tax gap exists—unfiled returns create a never-ending source of liability. If you want to dive deeper, you can read about the effects of the IRS statute of limitations on unfiled taxes.

The Unlimited Reach of Tax Fraud

The second scenario is far more serious: filing a fraudulent tax return. If the IRS can prove you willfully and intentionally filed a false return to duck your tax obligations, the 10-year statute of limitations on collections is completely wiped off the books.

Once fraud is on the table, there is no time limit on how long the IRS can pursue the debt. The back taxes essentially never expire, and the agency can legally chase you for collection for the rest of your life.

This is the nuclear option of tax non-compliance. While an unfiled return just keeps the clock from starting, a fraudulent one breaks the clock entirely. The IRS doesn't see this as an honest mistake; they see it as a deliberate attempt to cheat the government, and the penalties are designed to match that severity.

- Civil Fraud: When the IRS proves civil fraud—usually by showing a major understatement of income or bogus deductions made with intent to deceive—the collection statute is eliminated.

- Criminal Fraud: For the most egregious cases, taxpayers can face criminal fraud charges. This means you’re looking at not only unlimited collection but also massive fines and even prison time.

It’s crucial to know the difference between fraud and a simple error. A typo, a math mistake, or a genuine misunderstanding of a confusing tax rule isn't fraud. The government has to prove intent—that you knew you were breaking the law and did it anyway. But if they succeed, the protection of that 10-year CSED disappears completely, which just goes to show how critical it is to file honest and accurate tax returns every single year.

Actions That Can Pause the 10-Year Clock

Many people I talk to have that 10-year IRS collection deadline, the Collection Statute Expiration Date (CSED), circled on their mental calendars. They see it as a hard finish line. But here’s something that often catches them by surprise: the IRS collection clock isn't a simple countdown.

Certain actions you take to deal with your tax debt can actually hit a pause button on that clock. In the tax world, we call this tolling. Tolling temporarily stops the 10-year clock from running, which can stretch the collection period far beyond the original decade. Understanding what triggers these pauses is absolutely critical—a well-intentioned move to fix your tax problem could inadvertently give the IRS more time to collect if it's not handled with care.

Filing for Bankruptcy Protection

When you're buried in debt, filing for bankruptcy can feel like the only way out. It provides an immediate shield from creditors, including the IRS, by putting a stop to their collection efforts. However, that protection comes with a trade-off: it automatically freezes your CSED clock.

The clock stays paused for the entire time your bankruptcy case is active, from the moment you file until the case is officially discharged, dismissed, or closed. And it doesn't stop there. The law gives the IRS an extra six months after the bankruptcy ends to get back to their collection activities.

Let’s say a couple in Lansing is facing wage garnishment over a joint tax debt from a 2018 audit. They file for bankruptcy to get their finances in order. The second they file, that IRS collection clock stops ticking. If their bankruptcy case takes two years to resolve, the clock will be paused for those two years plus another six months. That adds a total of 2.5 years to their CSED, giving the IRS a much longer runway to collect.

Submitting an Offer in Compromise

An Offer in Compromise (OIC) is a fantastic tool that allows some taxpayers to settle their tax bill for less than the full amount they owe. But submitting an OIC application is another major event that pauses the CSED.

The clock stops the moment the IRS gets your OIC paperwork and remains paused for the entire time your offer is under review.

- If the IRS accepts your offer, the clock becomes irrelevant.

- If the IRS rejects your offer, the clock stays paused for another 30 days.

- If you appeal that rejection, the clock remains paused through the entire appeals process.

This rule exists to prevent people from submitting an OIC just to try and run out the clock on their tax debt.

Requesting a Collection Due Process Hearing

When the IRS sends a Final Notice of Intent to Levy, you have a legal right to request a Collection Due process (CDP) hearing. This is your chance to formally contest the levy and negotiate alternatives, but it's another action that pauses the collection statute.

The CSED is suspended from the day the IRS receives your hearing request until the Appeals Officer issues a final decision.

It's crucial to understand this part: If the Appeals Officer's decision becomes final when there are fewer than 90 days left on your original CSED, the law automatically extends the collection deadline to 90 days from the date of that final decision. This gives the IRS a fresh window to act.

The flowchart below shows two critical situations where the collection clock doesn't even start, highlighting just how important it is to file your returns and steer clear of fraud.

As you can see, failing to file or committing fraud means there's no statute of limitations to protect you. The IRS can pursue you indefinitely.

Common Events That Pause the IRS Collection Clock

Several other common taxpayer actions can add time to the IRS's collection calendar. Because each situation has its own specific rules for how long the pause lasts, getting professional guidance is incredibly important.

The table below breaks down some of the most frequent tolling events.

| Action (Tolling Event) | How Long the Clock Is Paused | Real-World Scenario |

|---|---|---|

| Offer in Compromise (OIC) | From submission until 30 days after rejection, or for the duration of an appeal. | You submit an OIC to settle a $50,000 debt. The clock pauses while the IRS reviews it. |

| Bankruptcy Filing | For the entire duration of the bankruptcy case, plus an additional 6 months. | You file Chapter 13, which takes 3 years. The clock is paused for a total of 3.5 years. |

| Collection Due Process (CDP) Hearing | From the date the request is received until the appeal determination is final. | You appeal a bank levy, and the process takes 8 months. Your CSED is extended by 8 months. |

| Installment Agreement Request | While the request is pending, plus 30 days if rejected, and for the duration of any appeal. | Your request for a payment plan is reviewed for 45 days. The clock pauses for those 45 days. |

| Innocent Spouse Relief Request | From the date of the request until 60 days after a final determination is made. | You claim you shouldn't be liable for your ex-spouse's tax debt. The clock on your portion of the debt is paused. |

| Living Outside the U.S. | For the entire time you are out of the country, if you're gone for at least 6 consecutive months. | You take a job overseas for 2 years. Your CSED clock is paused for the entire 2-year period. |

Navigating these rules requires a clear strategy. Sometimes, pausing collections is a worthwhile trade-off to secure a long-term solution. In other situations, a taxpayer might be better off seeking a temporary hardship placement. You can learn more about this option in our article about the IRS Currently Not Collectible status.

How Michigan State Tax Collection Rules Differ

It’s a common—and often costly—mistake to think that state tax rules just mirror the federal system. While most people are familiar with the IRS's 10-year collection statute, you have to remember that the Michigan Department of Treasury plays by an entirely different playbook. For anyone living or doing business in Michigan, knowing these differences isn't just academic; it's critical for resolving state tax debt.

If you don't grasp what makes Michigan's tax laws unique, you could be in for a rude awakening. You might find yourself facing aggressive collection actions long after you thought a tax debt had simply aged out. The state has its own timeline and, more importantly, its own ways of extending its power to collect.

Michigan's Statute of Limitations for Tax Collection

Unlike the straightforward 10-year rule from the IRS, Michigan’s statute of limitations isn't so simple. As a general rule, the state has six years from the date a tax is assessed to collect on it. But don't let that number fool you into a false sense of security.

This six-year window typically applies to common debts like individual income tax. The real trouble starts when you realize the state has powerful tools to secure its right to collect, especially on other types of tax. This is exactly where many taxpayers get tripped up—they apply what they know about the IRS to a state-level problem, and the outcomes can be disastrous.

The single biggest difference you need to understand is Michigan's ability to renew its collection authority. While the IRS clock usually runs out for good after 10 years (plus any pauses), Michigan can hit a reset button on its own clock through the court system.

How Michigan Can Extend Its Collection Power

The Michigan Department of Treasury has a powerful legal tool at its disposal that the IRS simply doesn't use: it can turn a tax assessment into a formal court judgment. By filing a lawsuit against a taxpayer, the state can obtain a judgment that remains valid for a full 10 years.

And here’s the real kicker: that judgment can be renewed for another 10 years. This legal maneuver completely transforms what started as a six-year collection window into a potential two-decade-long ordeal.

This process fundamentally changes the game for anyone with an outstanding Michigan tax bill. Here’s what you absolutely must keep in mind:

- The Starting Point: The state generally gets six years from the assessment date to start its collection efforts.

- The Game Changer: Before that six-year clock runs out, the Treasury can sue you to get a court judgment.

- The Judgment Power: This judgment is good for 10 years and gives the state serious collection muscle, including liens and levies.

- The Second Wind: The state can then renew that judgment for a second 10-year term, effectively doubling its collection timeframe.

Because the state can secure and renew these judgments, just waiting out a Michigan tax debt is an incredibly risky and usually failed strategy. The Michigan Department of Treasury is known to be proactive in protecting its right to collect, especially on larger tax balances. Dealing with this system requires specific, localized knowledge of Michigan law—making expert guidance not just helpful, but absolutely essential for protecting your assets.

Your Strategic Plan to Resolve Back Taxes

Knowing the rules of the game is one thing, but using them to build a winning strategy is another entirely. It's time to move from theory to action. Simply crossing your fingers and hoping the 10-year collection clock runs out is a passive—and frankly, dangerous—approach. The only way forward is to take control, find out exactly where you stand with the IRS, and build a concrete plan to put this debt behind you for good.

This isn't a process of guesswork. It’s about making precise, strategic decisions based on official records. You can shift from a position of uncertainty to one of empowerment by following a clear, structured roadmap to resolution.

Start with Verifiable Facts

The absolute first move is to get the facts straight from the source. You need to obtain your official IRS account transcripts for every single tax year in question. These documents are the bedrock of any successful resolution strategy because they hold the one date that truly matters: the Collection Statute Expiration Date (CSED).

Your transcripts will show you the exact date the IRS assessed your tax, which is when that 10-year clock started ticking. They also detail any events that paused the clock, ensuring you aren’t miscalculating this critical deadline. While you can request these online or by mail, learning to interpret them correctly is a skill in itself.

Analyze Your Transcripts and CSED

Once the transcripts are in your hands, the real analysis begins. You’ll be looking for specific transaction codes, like the "290" code that often signals the initial assessment date. From there, you have to carefully scan the account history for any actions—like a submitted Offer in Compromise or a bankruptcy filing—that would have suspended the collection period.

This is where having an expert in your corner becomes invaluable. Misreading a single code or date could trick you into believing your CSED is much closer than it is, completely derailing your strategy. When you're putting your plan together, considering services in professional tax preparation can be a crucial step for making sure all your financial details are in order.

A correctly calculated CSED is your strategic advantage. It tells you exactly how much time you and the IRS have left, which directly dictates which resolution options are actually on the table for you.

Evaluate Your Resolution Options

With a verified CSED, you can finally evaluate your options from a position of strength. Your best move will almost always depend on two things: how much time is left on the clock and your current financial situation.

- Significant Time Remaining (3+ years): If your CSED is still years away, waiting it out isn't a strategy. It's a liability. This is the time to proactively pursue solutions like an Installment Agreement for manageable monthly payments or an Offer in Compromise (OIC) to settle the debt for a fraction of what you owe. You can learn more about this powerful tool in our guide on what an Offer in Compromise is.

- Limited Time Remaining (1-2 years): As the clock winds down, your leverage increases. It might be possible to negotiate a more favorable payment plan or even be placed in Currently Not Collectible (CNC) status, which temporarily pauses collections if you're facing financial hardship.

- CSED is Imminent (Under 1 year): When the finish line is in sight, the focus shifts to defense. The primary goal is to avoid taking any accidental actions that could extend the deadline. You want to run out the clock without giving the IRS a last-minute reason to stop it.

Each path requires careful, deliberate planning. For instance, an ill-timed OIC submission could pause the clock just weeks before it's set to expire, completely undoing years of waiting. By taking these methodical steps, you can build a solid plan to finally resolve your back taxes and achieve lasting financial freedom.

Why a Michigan Tax Attorney Is Your Best Ally

Trying to figure out the Collection Statute Expiration Date (CSED) on your own is a recipe for disaster. The rules that dictate how long the IRS can collect back taxes are a labyrinth of exceptions, pauses, and extensions. One wrong move—like filing an Offer in Compromise at the worst possible time—could stop the clock just before it runs out, adding years to your financial nightmare.

This is exactly why you need a specialized Michigan tax attorney in your corner. We don't just take a guess at your CSED. We pull your official IRS transcripts and comb through them line by line to find the precise date your tax debt is supposed to disappear. Even more important, we know how to spot errors the IRS makes in its own math—and believe me, it happens more often than you'd think.

Protecting You from Costly Mistakes

Think of a tax attorney as your strategic shield. We stand between you and the IRS, handling every phone call and every letter so you never accidentally say or do something that gives them more time to collect. When you're facing down aggressive revenue officers, that protection is priceless.

Our expertise becomes absolutely critical in a few key situations:

- Collection Due Process (CDP) Hearings: We represent you in these formal proceedings, fighting back against proposed levies and liens while carefully managing how it affects the CSED clock.

- Strategic Offers in Compromise (OICs): We don't just fill out forms. We build a case designed for acceptance, drastically reducing the chance of a rejection that pauses the statute of limitations for no good reason.

- Defending Against Liens and Levies: When the IRS tries to seize your bank account or garnish your wages, we move fast to protect what's yours by asserting your legal rights.

For taxpayers in Detroit, Lansing, and all over Michigan, expert guidance is the only reliable way to a resolution. Going it alone is like walking through a legal minefield without a map—the risk of a misstep is just too great.

Local Expertise for State and Federal Issues

Whether your problem is with the IRS or the Michigan Department of Treasury, having a local team makes a real difference. We know the specific tactics and legal quirks that are unique to Michigan, offering a depth of insight a big national firm simply can't provide. We can also help you explore options like requesting a Form 843 for tax abatement if you've been hit with unfair penalties or interest.

Ultimately, hiring a tax attorney isn't just another cost—it's an investment in your financial future. It means your game plan is built on solid legal ground and accurate information, giving you the best shot at finally closing this chapter for good.

Your Questions About the CSED, Answered

Let's be honest, the rules around how long the IRS can chase you for back taxes are confusing. To clear things up, we've tackled the most common questions we hear from taxpayers about the Collection Statute Expiration Date (CSED). Getting these answers straight is the first step toward getting control of your situation.

Can the IRS Really Collect a Tax Debt After 10 Years?

In most cases, no. Once that CSED finally arrives, the IRS legally loses its power to collect on that specific tax debt. But here’s the critical catch: it's rarely a simple 10-year countdown from when you filed the return.

The clock can be paused by certain actions, which we call “tolling” events. Filing for bankruptcy, submitting an Offer in Compromise, or requesting a Collection Due Process hearing all stop the clock and extend the collection period. This is why you can't just guess your CSED; you have to pull your official IRS transcript to know for sure.

Will the IRS Send a Letter When the Collection Statute Is About to Expire?

Absolutely not. The IRS will not send you a friendly reminder that your collection deadline is approaching. Tracking this critical date is 100% on your shoulders as the taxpayer.

This is exactly why getting and reviewing your IRS account transcripts is so important. Without them, you’re flying blind, with no real idea of when your liability will finally be resolved. Staying on top of this date is your best defense.

Think of the CSED as a finish line that the IRS has no obligation to point out to you. Your financial freedom hinges on you knowing where that line is and understanding what moves it further away.

If I Make a Payment on an Old Tax Debt, Does It Restart the 10-Year Clock?

This is one of the most persistent—and dangerous—myths out there. Making a voluntary payment on an old tax debt does not restart the 10-year collection clock. The CSED is fixed by the initial assessment date and is only extended by specific legal events, not by sending the IRS a check.

Where people get into trouble is by signing certain documents. For instance, the IRS might ask you to sign a waiver to extend the collection period as part of a deal. Be extremely careful and make sure you understand every single document you sign.

What Happens to an IRS Tax Lien After the CSED Expires?

Once the CSED on your tax debt passes, the IRS is legally required to release any federal tax lien tied to it. This should happen on its own within 30 days of the expiration date.

But what if it doesn't? A lingering lien can wreak havoc on your credit and public record. If the IRS drags its feet, you have the right to request a Certificate of Release of Federal Tax Lien. This is the official document that proves the debt is gone and clears your name.