What Is an Offer in Compromise and How Does It Work

Ever wonder if you can settle your tax debt for less than you owe? It’s not a myth. It’s a formal government program called an Offer in Compromise (OIC), and it’s designed to give taxpayers a fresh start when they’re facing true financial hardship.

This isn’t just about getting a discount on your tax bill. An OIC is a serious agreement between you and the IRS (or the Michigan Department of Treasury) to resolve your tax liability for an amount that reflects what you can realistically pay.

Understanding The Offer in Compromise

Think of an OIC as a final negotiation with the government. If your tax debt feels like an impossible mountain to climb, this program can offer a way through it—not over it. The goal is to arrive at a settlement figure that the government believes is the most it can ever hope to collect from you, given your complete financial picture.

Let’s be clear: this is no loophole. The IRS and Michigan tax authorities will put your finances under a microscope before they even consider your offer. It’s a formal, structured process for people truly buried under a tax burden they can’t manage. For a deeper look at this powerful debt relief option, this guide on What Is Offer in Compromise: A Complete Taxpayer Guide is an excellent resource.

To help you get a quick handle on what an OIC involves, here’s a simple breakdown of its key elements.

Offer in Compromise At a Glance

| Component | Brief Description |

|---|---|

| Purpose | To resolve federal or state tax debt for less than the full amount owed. |

| Eligibility Basis | Based on the taxpayer’s ability to pay, income, expenses, and asset equity. |

| Key Metric | The government calculates your “Reasonable Collection Potential” (RCP) to set the minimum offer. |

| Common Scenarios | Used when a taxpayer’s assets and income are not enough to pay the full debt. |

| Commitment | The taxpayer must stay compliant with all tax laws for five years after acceptance. |

This table summarizes the core of the OIC program, showing it’s a serious commitment based on a detailed financial review.

The Reality of OIC Acceptance Rates

It’s absolutely critical to go into this with realistic expectations. The OIC program is notoriously tough, with stringent requirements and surprisingly low acceptance rates that have been falling in recent years. This is why a perfectly prepared application is non-negotiable.

An Offer in Compromise is a powerful IRS program that lets taxpayers settle their tax debt for less than what they owe, but it’s far from a guaranteed win—especially in recent years.

Consider the numbers from a recent fiscal year: the IRS received 33,591 OIC applications but only accepted 7,199. That’s a stark 21% acceptance rate, a significant drop from the 40% average seen over the previous decade. You can find this kind of data published in the official IRS Data Book, which highlights recent enforcement trends.

Why The Government Offers This Program

So, why would the government ever agree to take pennies on the dollar? The answer is pure pragmatism. It all comes down to a concept called “Reasonable Collection Potential” (RCP), which we’ll dive into later.

Essentially, the government would rather collect a smaller, achievable amount today than spend years and resources chasing a massive debt that a taxpayer will likely never be able to repay. The OIC program is a final resolution tool. It allows the government to close the book on a difficult case and gives the taxpayer a chance to get back on solid financial ground. If you’re a Michigan taxpayer drowning in tax debt, the team at https://www.michigantaxattorneys.net/ can help you figure out if an OIC is the right move for you.

How the IRS Decides Who Qualifies for an OIC

The IRS isn’t swayed by a sob story, no matter how compelling it is. When you submit an Offer in Compromise, their decision comes down to a cold, hard financial calculation. It all hinges on a single, critical concept: your Reasonable Collection Potential (RCP).

Think of your RCP as the government’s bottom line. It’s the maximum amount the IRS believes it can realistically squeeze from you over the next few years. If you owe $80,000 in back taxes but your RCP is only calculated to be $12,000, the IRS might just agree to settle for that $12,000. Why? Because, from a purely pragmatic standpoint, it’s the most they ever expect to get.

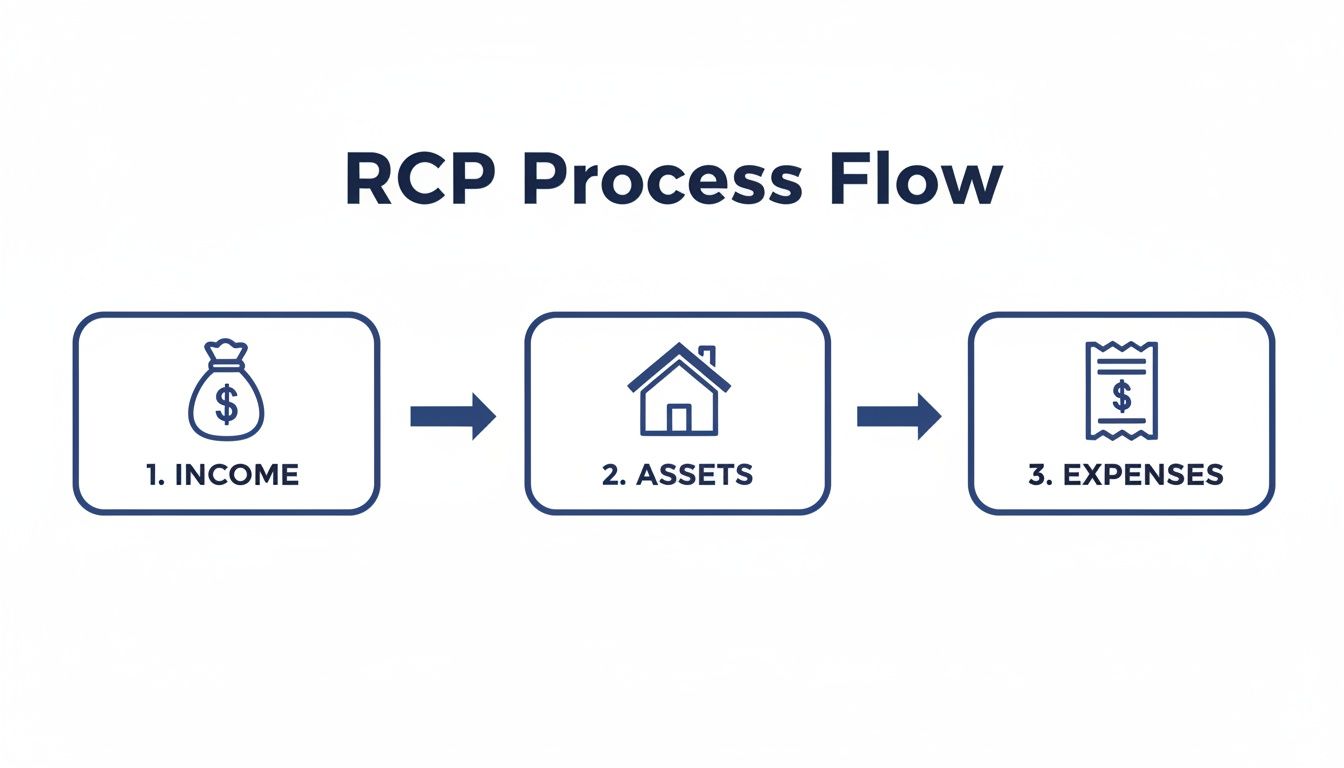

The Three Pillars of Reasonable Collection Potential

So, how does the IRS arrive at this number? They build your RCP by dissecting three core areas of your financial life, leaving no stone unturned to get a complete picture of your true ability to pay.

- Your Income: This isn’t just about your last paycheck. They look at everything coming in—wages, self-employment income, rental income, you name it. They’re trying to project your future earning potential, not just your current situation.

- Your Assets: The government will tally up the equity you have in everything you own. This means your house, cars, boats, bank accounts, retirement funds, and any investments. They’re interested in the “quick sale value,” which is what those assets would be worth if they had to be liquidated fast.

- Your Allowable Expenses: Here’s where many people get tripped up. The IRS doesn’t care about your actual monthly budget. They use a rigid set of national and local standards for essential costs like housing, food, transportation, and healthcare. If your spending goes above these strict allowances, the IRS generally won’t count it.

This formulaic approach can lead to some eye-opening results. A family in Michigan might feel like they’re barely scraping by, but if their mortgage payment is higher than the local IRS housing standard, that “excess” amount gets added right back into their calculated ability to pay.

The Official Grounds for an OIC

Once the IRS has a clear financial snapshot, your case must fit neatly into one of three official categories. These are the only legal justifications the IRS will accept for settling your debt for less than you owe.

An Offer in Compromise isn’t a right; it’s a concession. Your application has to prove that taking your smaller offer is a better deal for the U.S. Treasury than trying to collect the full amount.

Here are the three valid reasons:

- Doubt as to Collectibility: This is the big one—the most common path to an OIC. You’re arguing that, based on your income and assets, you will never be able to pay the full tax debt. Your RCP calculation is the key piece of evidence here.

- Doubt as to Liability: This is a much rarer argument. Here, you’re claiming the tax itself was assessed incorrectly and you don’t actually owe the money in the first place. You’ll need concrete evidence to challenge the original tax bill.

- Effective Tax Administration (ETA): This is essentially a fairness argument. You might technically have the assets to pay in full, but doing so would create an exceptional economic hardship. This could apply to an elderly taxpayer who would have to sell their only home, leaving them with no funds to cover basic living expenses.

Critical Prerequisites Before You Apply

Before the IRS will even glance at your offer, you have to get your house in order. Missing any of these non-negotiable requirements means your application will be rejected right out of the gate.

- You must have filed all of your required tax returns.

- You need to be current on all required estimated tax payments for the current year.

- If you’re a business owner with employees, you must be current on all required federal tax deposits for the most recent quarter.

The numbers show just how selective the IRS is. In a recent year, out of 33,591 OICs submitted, only 7,199 were accepted. When the stakes are high—often with unpaid taxes of $50,000 or more—the process gets even more intense. This led to 2,918 of those civil cases, plus another 46 criminal ones, requiring a deep-dive review from the Chief Counsel’s office. You can learn more about how the IRS handles OIC applications on their official payments page.

The Step-by-Step OIC Application Process

Applying for an Offer in Compromise is less like filling out a form and more like building a detailed, compelling case for why the government should settle your tax debt for less than you owe. It’s a thorough, multi-stage journey that demands absolute precision and honesty from beginning to end.

Think of it as preparing for a comprehensive financial audit. You’re laying all your financial cards on the table, and every single number needs to be backed by solid proof. This isn’t the time for ballpark figures; the IRS and the Michigan Treasury need to see the complete, documented story of your financial situation.

Gathering Your Financial Documentation

The first real step is rolling up your sleeves and collecting all the required paperwork. I won’t sugarcoat it—this is the most time-consuming part of the whole process, but it’s where successful applications are made or broken.

You’ll need to pull together a file that proves everything you claim about your income, assets, and living expenses. Key documents almost always include:

- Proof of Income: Your last six months of pay stubs are a must. If you’re self-employed, you’ll need profit and loss statements. Don’t forget records of any other income you receive.

- Bank Statements: Gather at least the last three to six months of statements for all of your accounts, both personal and business.

- Asset Information: This includes deeds for any real estate, titles for your vehicles, and recent statements for retirement accounts like a 401(k) or an IRA.

- Proof of Expenses: You’ll need to show what you pay for essentials. This means pulling utility bills, mortgage or rent statements, car payments, and records of significant medical expenses.

Properly organizing this mountain of paperwork is half the battle. You can find some great tips on how to organize receipts for taxes that can really help you get everything in order.

Completing the Official IRS Forms

Once your documents are in hand, it’s time to tackle the official forms. These are the heart of your application, and they have to be filled out perfectly.

The two main forms you’ll be working with are:

- Form 656, Offer in Compromise: This is where you formally state your offer amount and explain the reason for your request—most commonly, Doubt as to Collectibility.

- Form 433-A (OIC) or 433-B (OIC): This is your Collection Information Statement. Individuals and sole proprietors use Form 433-A, while businesses use Form 433-B. This is an exhaustive form that provides the IRS with a fine-tooth-comb view of your finances, which they use to calculate your Reasonable Collection Potential.

When you submit these forms, you also have to include a non-refundable $205 application fee and your first payment toward the offer. There are waivers for this fee available for low-income taxpayers, so it’s worth checking if you qualify.

The government scrutinizes three core financial pillars to see what you can truly afford to pay.

This graphic really boils it down. The IRS looks at what you bring in and what you own, then subtracts your necessary living expenses to figure out what they believe they could realistically collect from you over time.

What Happens After You Submit Your Application

After you’ve mailed your package, the waiting begins. First, the IRS does an initial screening to make sure your application is complete and that you’re up-to-date on all your tax filings. If it passes that first hurdle, your case gets assigned to an Offer Specialist or Offer Examiner.

This specialist is your point person. They will dig deep into every document you sent, cross-reference your information with third-party data, and will almost certainly come back to you with questions or requests for more information.

This isn’t a passive waiting game. It’s an active negotiation. How quickly and thoroughly you respond to the Offer Specialist can make or break your case.

It is absolutely critical to respond to any IRS request right away. If you drag your feet or provide incomplete answers, they won’t hesitate to reject your offer. The whole review process can take anywhere from 6 to 12 months, sometimes longer for more complex cases. The good news is that during this period, most of their collection actions against you are put on hold.

Finally, you’ll receive a formal letter in the mail with their decision: an acceptance, a rejection, or a counteroffer.

Navigating a Michigan State Offer in Compromise

If you’re staring down both federal and state tax debt, getting a deal with the IRS is only half the battle. Many Michigan taxpayers are caught off guard when they realize an accepted IRS Offer in Compromise means nothing to the Michigan Department of Treasury.

The state runs its own, entirely separate OIC program with its own rulebook. An IRS settlement won’t automatically fix your state tax problem; you have to start a new fight on a different front.

Michigan’s Unique Eligibility Requirements

Think of the IRS process as a math problem and the Michigan process as a compelling story you have to prove. While the IRS leans heavily on a formula called Reasonable Collection Potential, Michigan’s decision-makers are focused on one key question: Would forcing you to pay the full amount cause an “extreme financial hardship”?

This is a much higher bar to clear. Just having a tight budget won’t cut it. You typically need to prove one of two things:

- Insolvency: This is a straightforward, if painful, calculation. You have to show that your total liabilities—everything you owe to everyone—are greater than the fair market value of your assets.

- Doubt as to Liability: This is the “I don’t actually owe this” argument. It’s similar to the IRS version, but you’ll need rock-solid evidence to convince the state that its original tax assessment was wrong.

The state needs to see clear proof that paying in full is not just difficult, but truly impossible without depriving you of basic necessities.

A common misconception is that if the IRS accepts your offer, Michigan will automatically follow suit. This is incorrect. The Michigan Department of Treasury conducts an independent review and may arrive at a completely different conclusion based on its own guidelines.

State-Specific Forms and Documentation

To plead your case to the state, you need to build a new application package from the ground up, starting with Form 5181, Offer in Compromise. This document, along with a meticulously detailed financial statement, is the cornerstone of your request.

Just like with the IRS, you’ll have to lay all your financial cards on the table. Be prepared to provide:

- Recent pay stubs and proof of all other income.

- Bank statements for every single personal and business account.

- Records for all assets, including real estate, vehicles, and retirement funds.

- Proof of essential living expenses like rent or mortgage payments, utilities, and medical costs.

Any inconsistency or missing piece of information is a red flag for the state and one of the quickest ways to get your offer denied.

Key Differences Between Federal and State OICs

Understanding how the two programs differ is critical for any Michigan taxpayer hoping for a fresh start. It’s a complex landscape, and having a local tax attorney who knows Michigan’s specific enforcement trends can make all the difference. For those seeking help from Detroit to Grand Rapids, you can learn more about our tax attorney locations and how we can support you.

To make things clearer, let’s break down the most important differences you’ll face when dealing with the IRS versus the Michigan Department of Treasury.

IRS vs. Michigan Offer in Compromise Key Differences

| Feature | IRS OIC (Federal) | Michigan OIC (State) |

|---|---|---|

| Primary Basis | Based on a formula calculating your Reasonable Collection Potential (RCP). | Primarily based on proving insolvency or extreme financial hardship. |

| Key Forms | Form 656 and Form 433-A/B (OIC). | Form 5181, Offer in Compromise, and supporting financial statements. |

| Application Fee | A non-refundable $205 application fee is typically required. | There is generally no application fee required for a Michigan OIC. |

| Review Process | A structured review process conducted by an IRS Offer Specialist. | An independent review conducted by the Michigan Department of Treasury. |

When it comes down to it, tackling a Michigan state tax debt requires a tailored strategy. Success hinges on building a powerful, convincing case that demonstrates your inability to pay, backed by transparent and flawless financial documentation that meets the state’s exacting standards.

Common Reasons Your OIC Might Be Rejected (And How to Avoid Them)

Getting an Offer in Compromise approved isn’t as simple as filling out a few forms. It’s about building a rock-solid case that can withstand intense scrutiny. With notoriously low acceptance rates, the best way to get your offer accepted is to first understand why so many others get denied.

Most rejections come down to preventable errors. If you approach your application with the same seriousness as a financial audit, you can steer clear of the common pitfalls that sink otherwise strong cases.

Incomplete or Inaccurate Financials

By far, the number one reason an OIC is rejected is a flawed Collection Information Statement (Form 433). The IRS and state examiners don’t just take your word for it; they will comb through your finances and cross-reference every number against public records and other data sources. Even a small discrepancy can derail your entire application.

Watch out for these common mistakes:

- Forgotten Assets: Did you forget about that old 401(k) from a previous job? A small savings account you rarely use? Equity in a second vehicle? They will find it.

- Understated Income: You have to account for everything, including income from side hustles, freelance projects, or any other irregular payments.

- Inflated Expenses: This is a big one. The IRS doesn’t care what your actual expenses are; they care what their national and local standards say your expenses should be. Claiming more than these allowable living costs is a red flag.

The only way to succeed is with complete transparency. Gather every bank statement, pay stub, and financial record you can find, and make sure every line on your Form 433 is accurate and backed up by proof.

Think of it this way: your application tells a story about your financial life. If the IRS finds even one chapter that doesn’t add up, they’ll shut the book on your entire case.

Falling Out of Tax Compliance

Here’s a critical point many people miss: applying for an OIC doesn’t give you a break from your current tax duties. One of the fastest ways to have your offer rejected is to fall behind on new tax obligations while your application is under review.

This means you absolutely must continue to:

- File all required tax returns on time.

- Make all required estimated tax payments if you’re self-employed.

- Stay current on federal tax deposits if you own a business with employees.

The government views this as a simple test of good faith. If you can’t handle your current responsibilities, they have zero confidence that you’ll honor the terms of a settlement.

The Five-Year Compliance Rule After Acceptance

Even if your offer is accepted, you’re not out of the woods just yet. You immediately enter a mandatory five-year compliance period, and you’ll be under a microscope the entire time. During these five years, you have to file and pay all of your taxes in full and on time, without exception.

One misstep—a late filing or a missed payment—can void the entire agreement. If that happens, the original tax debt comes roaring back, complete with all the penalties and interest that had been wiped away.

After acceptance, existing tax liens also remain in place until you’ve fully paid the offer amount. While this process is strict, an OIC is a powerful lifeline, especially when combined with penalty abatements that can further reduce what you owe. With IRS enforcement on the rise, getting an offer through is tougher than in past years, which saw higher acceptance rates. You can always find more official data about IRS collections activities and appeals online.

Powerful Alternatives to an Offer in Compromise

Getting an Offer in Compromise accepted is a huge win, but it’s a tough road with strict eligibility rules. Not everyone makes the cut, and that’s okay—it’s far from the only tool in the toolbox.

The good news is that both the IRS and the Michigan Department of Treasury have other relief programs designed for different financial circumstances. Chasing an OIC when another option is a better fit can burn through precious time and money. Let’s walk through the other paths available so you can find the right one to get back on solid ground.

Installment Agreements

If you can eventually pay your tax bill in full but just can’t do it all at once, an Installment Agreement is your most straightforward option. It’s essentially a payment plan that lets you make predictable monthly payments over time.

For federal taxes, these agreements can stretch out for up to 72 months. Think of it less as a settlement and more as a financing arrangement. You still owe the full amount, and interest and penalties will keep adding up, but it immediately stops aggressive collection tactics like wage garnishments or bank levies. This is the go-to solution for people with reliable income who just need to break a large tax debt into manageable pieces.

Currently Not Collectible Status

What happens when you can’t afford to pay anything at all? If a job loss, medical emergency, or another crisis has left you without the means to cover even your basic living expenses, you might qualify for Currently Not Collectible (CNC) status.

Getting your account placed in CNC status presses the pause button on all collection efforts. The IRS acknowledges that you simply don’t have the ability to pay right now and will temporarily stop sending notices and demands.

CNC is a temporary reprieve, not a permanent fix. The IRS will check in on your financial situation periodically. If your income recovers, they’ll expect you to start paying again.

It’s important to know that while your account is in CNC, the debt doesn’t go away—interest and penalties continue to accrue. However, the ten-year clock on the statute of limitations for collection keeps ticking. CNC provides a critical safety net when you’re facing extreme financial hardship.

Penalty Abatement

Sometimes the penalties are the biggest part of the problem, ballooning a manageable tax bill into an overwhelming one. If you have a solid history of filing and paying on time but hit a rough patch for reasons outside your control, you can ask for Penalty Abatement.

The IRS may grant this for what they call “reasonable cause.” Some common examples include:

- A serious illness or death of an immediate family member.

- A fire, flood, or another natural disaster.

- Receiving incorrect advice from a tax professional.

If your request is approved, the IRS can remove some or all of the penalties. This can dramatically lower what you owe, often making the remaining balance something you can handle with a simple Installment Agreement.

For taxpayers facing a tangled web of tax issues, exploring every angle, including an IRS tax settlement in Westphalia, MI, is the best way to find a clear resolution. Each of these alternatives serves a unique purpose, offering a flexible solution for nearly any financial situation.

Frequently Asked Questions About Offers in Compromise

When you’re staring down a serious tax debt, the idea of an Offer in Compromise can bring up a lot of questions. Let’s tackle some of the most common ones we hear from Michigan taxpayers.

How Long Does the Offer in Compromise Process Take?

Here’s the hard truth: this is not a quick fix. You need to be patient. From the moment you mail your application to the day you get a final answer from the IRS or the state, you’re typically looking at a timeline of 6 to 12 months.

For more complicated situations, like those involving a business or unusual assets, it can take even longer. The one silver lining is that while your offer is under review, the most aggressive collection actions—things like wage garnishments and bank levies—are usually put on hold.

What Happens to a Tax Lien if My OIC Is Accepted?

Getting your OIC accepted is a huge step forward, but it doesn’t mean existing tax liens just vanish overnight. The lien will stay in place until you’ve held up your end of the bargain completely.

To get the lien released, you have to do two things:

- First, pay the full settlement amount you agreed to, whether as a lump sum or in installments.

- Second, you must stay clean for the next five years. This is a mandatory compliance period where you have to file and pay all your future taxes on time, no exceptions.

Once you’ve paid the offer and successfully completed that five-year period, the IRS will finally release the lien.

Can I Apply for an OIC if I Own a Business?

Absolutely, but you need to be prepared for a much deeper dive into your finances. The government will examine both your personal and business financial health with a fine-toothed comb.

For individuals, the main financial form is the 433-A. As a business owner, you’ll also need to tackle Form 433-B, the Collection Information Statement for Businesses. They will scrutinize every detail—your business assets, income, expenses, and what they believe its future earning potential is—all of which gets rolled into that crucial Reasonable Collection Potential calculation. It makes for a far more complex application.