A Practical Guide to IRS Form 843 Abatement

Getting a penalty notice from the IRS can be a gut-punch, but don't panic. If you have a legitimate reason for a mistake, the IRS provides a specific tool to ask for forgiveness: Form 843, Claim for Refund and Request for Abatement.

Think of this form as your formal way to ask the IRS to cancel—or "abate"—certain penalties. It's not for asking for an income tax refund, but it’s absolutely the right tool when circumstances beyond your control, like a severe illness or a natural disaster, made it impossible to meet your tax obligations on time. Knowing if and when to use this form is your first move toward getting that penalty waived.

When to Use Form 843 for Penalty Abatement

When that IRS notice lands in your mailbox, it's easy to feel cornered. The important thing is to understand which path to take. A Form 843 abatement isn't a way to haggle over your tax bill or settle for a lower amount—that’s what an Offer in Compromise is for. Instead, Form 843 is your official statement arguing that the penalty was unfair and shouldn't have been charged in the first place.

Your argument will almost always boil down to one of two things:

- Reasonable Cause: You need to show that you did everything a responsible person would do to manage their taxes, but something happened that was completely out of your hands.

- Administrative Waiver: This is where programs like the First-Time Abate (FTA) policy come in. If you have a squeaky-clean compliance record for the past three years, the IRS may grant you a one-time pass.

The distinction is critical: an Offer in Compromise is about your inability to pay. A Form 843 abatement is about the fairness of the penalty itself.

Identifying the Right Scenarios for Form 843

Knowing when to file Form 843 is half the battle. It isn't a catch-all solution, but it’s the right move for certain types of penalties.

Let's say you're a small business owner in Detroit, and a major flood knocks out your power and floods your office for two weeks. You missed the deadline for making payroll tax deposits. That's a classic case for Form 843. You'd argue "reasonable cause" and provide photos, news articles, and repair bills to back up your claim.

Or imagine an individual in Grand Rapids who was in a serious car accident and hospitalized for a month, causing them to miss the tax filing deadline. They have a very strong case for having the late-filing penalty abated.

Key Takeaway: Form 843 is your official channel for explaining why a penalty is unjust. It requires a compelling story backed by solid proof, shifting the focus from simply owing money to demonstrating that circumstances made compliance impossible.

A Word on the Low Success Rate

Winning a Form 843 abatement is far from a sure thing. The IRS doesn't just hand these out. In fact, the odds can feel stacked against you.

Back in 2019, data showed that only 12% of failure-to-file and failure-to-pay penalties were actually abated. For individual taxpayers, that number dropped to a grim 9%. You can dig into more of these IRS penalty statistics on JacksonHewitt.com.

These numbers aren't meant to discourage you; they're meant to prepare you. They show why a carefully prepared request is non-negotiable. Many people either don’t bother asking for relief or throw in the towel after the first denial. For Michigan residents, this reality means your documentation and your explanation have to be airtight.

A vague excuse or missing paperwork is the quickest way to get a rejection letter. The IRS needs to see a direct, logical link between the event you’re citing and your failure to file or pay. This is precisely why many taxpayers facing steep penalties in Michigan decide to work with a tax attorney. A professional knows how to frame the argument, gather the right evidence, and handle the appeals process if the IRS says no the first time.

Choosing the Right IRS Penalty Relief Tool

It's easy to get confused by the different IRS resolution options. This quick table can help you pinpoint the right tool for your specific challenge.

| Situation | Best IRS Tool | Key Consideration |

|---|---|---|

| You have a clean tax history but made a one-time mistake. | First-Time Abate | You haven't had any penalties in the prior 3 tax years. Often handled by phone. |

| An unforeseen event (illness, disaster) caused you to miss a deadline. | Form 843 (Reasonable Cause) | You must provide strong evidence linking the event to your non-compliance. |

| You can't afford to pay your tax debt in full. | Offer in Compromise (OIC) | This is for financial hardship, proving you can't pay. It's not for penalty fairness. |

| An IRS error caused the penalty. | Form 843 (IRS Error) | You need to prove the IRS provided incorrect advice or made a clear mistake. |

| You are experiencing immediate and severe financial hardship. | Form 911 (Taxpayer Advocate) | This is an emergency measure when an IRS action is causing significant hardship. |

This table is just a starting point. Your situation is unique, and sometimes the best path forward involves a combination of strategies.

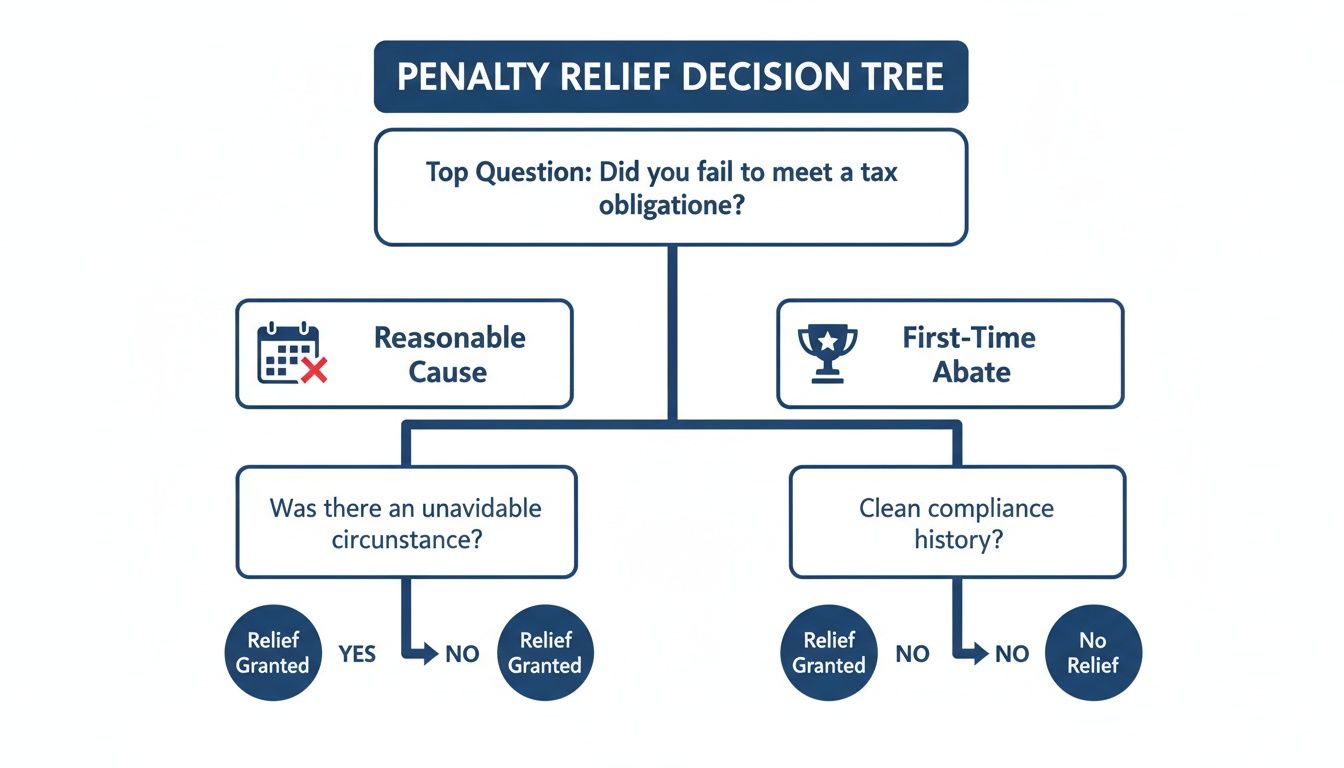

Do You Qualify for Penalty Relief? Let's Find Out.

Before you even think about filling out Form 843, the first and most important step is to figure out if you actually have a case. The IRS provides two main avenues for getting penalties waived, and knowing which one fits your situation is key. Are you eligible for the straightforward First-Time Abatement, or will you need to build a more detailed argument for Reasonable Cause?

This decision tree gives you a quick visual on how the two paths diverge.

As you can see, everything starts with your compliance history. That one factor will point you toward either the simple administrative waiver (FTA) or the more involved, evidence-based argument for reasonable cause.

The Easiest Path: First-Time Abatement

For many taxpayers here in Michigan, the First-Time Abatement (FTA) program is a godsend. It's the simplest and fastest way to get relief. Think of it as a one-time "free pass" from the IRS, reserved for people who have a great track record of paying their taxes on time.

The qualifications are refreshingly simple:

- A Clean Three-Year Record: You can't have had any penalties for the three tax years just before the year you're asking for relief.

- You're All Caught Up: All your required tax returns have been filed (or you've filed for a valid extension).

- The Bill Is Settled: You've either paid the tax you owe or have set up a formal plan to pay it.

This is a really powerful option. In my experience, a simple phone call to the IRS is often all it takes to get FTA approved. If you qualify, they might even grant it automatically. You'll get a confirmation letter in the mail a few weeks later, and that's it.

Sometimes you don't even need to file Form 843 to get this relief. But even if you do, the IRS is instructed to check for FTA eligibility first, no matter what other reason you put down on the form.

When Things Get Complicated: Building a Case for Reasonable Cause

What if you don't qualify for that clean-slate approach? That's when you have to make a case for "Reasonable Cause." This is a more involved argument where you need to prove you did everything a responsible person would do—exercising ordinary business care and prudence—but you still couldn't file or pay on time because of circumstances completely out of your control.

This isn't for when you just forgot or were too busy. The IRS wants to see a direct line connecting a major life event to your tax problem.

Common Scenarios That Qualify as Reasonable Cause:

- Death or Serious Illness: This could be your own illness or that of an immediate family member. If you were the primary caregiver for a parent who had a sudden stroke, for instance, it's completely understandable that filing taxes wasn't your top priority.

- Unavoidable Absence: Maybe you were stuck overseas on an unexpected business trip, or you were incarcerated and simply couldn't get to your records to file.

- Destruction of Records: Picture this: a fire or flood in your Lansing home destroys all your tax documents a week before the filing deadline. That’s a classic, and very strong, case for reasonable cause.

- Bad Advice from the IRS: If an IRS employee gave you the wrong information over the phone and you relied on it, you can argue for abatement. The trick here is having proof—you'll need notes from the call, including the date and the employee's name or ID number if you got it.

Making a case for reasonable cause is all about the evidence. It's not enough to just tell your story; you have to back it up with documentation. We’ll get into exactly what kind of proof you need later on. For a closer look at the different types of penalty abatement, you can dig into our detailed guide.

Ultimately, your goal is to paint a clear, honest picture for the IRS agent reviewing your case, showing them you're a responsible person who just got hit by a tough situation.

A Step-by-Step Guide to Filling Out Form 843

Alright, let's move from theory to practice and walk through the Form 843 itself. While the form looks simple enough, a few key lines can make or break your request for a Form 843 abatement. Precision is your best friend here—it helps the IRS agent understand your situation right from the start and ensures your request gets processed without a hitch.

We'll focus on the parts that tend to trip people up, especially the all-important "Explanation" section where you get to tell your story.

The Essential Details: Lines 1 Through 6

First things first. Before you can make your case, you have to give the IRS the right administrative details. Getting these lines correct is crucial for preventing your form from being kicked back on a technicality.

-

Line 1: This is where you specify the type of tax involved. Most of the time, penalty abatement requests are for employment, estate, gift, or excise taxes. But what if your penalty is for a personal income tax return, like a failure-to-file penalty on your Form 1040? In that case, you’d check "Other" and simply write in "Income."

-

Line 2: Pinpoint the exact tax period or year you're asking for relief. Precision matters. For payroll taxes, use the specific quarter (e.g., "Quarter ending 03/31/2023"). For an annual return, just list the year (e.g., "2022").

-

Line 3: State the exact dollar amount of the penalty you want abated. Don't guess. Pull this figure directly from the IRS notice you received.

-

Line 4: You'll need to note which IRS office sent you the notice. This is usually printed in the top right corner of the letter. If for some reason you can't find it, you can list the IRS service center where you originally filed your return.

Think of these initial fields as setting the stage. An agent who can quickly identify the what, when, and how much is far more likely to give your detailed explanation on Line 7 the attention it truly deserves.

Crafting Your Narrative in Line 7: The Explanation

This is the heart of your Form 843 abatement request. Line 7 is your single best opportunity to build a clear, compelling, and persuasive argument for why you deserve penalty relief. It's not just a box to fill; it’s where you connect the dots for the IRS.

Your explanation should read like a short, factual story. Start by clearly stating your purpose, then outline the sequence of events, and finally, draw a direct line between those events and your inability to file or pay on time. Your goal is to show that you acted with ordinary business care and prudence, but circumstances beyond your control got in the way.

A winning explanation always includes these elements:

- A Clear Opening: State exactly what you're requesting and for which tax period.

- A Chronological Story: Lay out the events as they happened. Use specific dates.

- The Direct Link: Explain precisely how these events prevented you from meeting your tax obligations.

- Proof of Responsibility: Show what you did to get back into compliance as soon as you could.

- A Reference to Evidence: Briefly mention the supporting documents you’ve attached.

Here's a sample opening to give you an idea: "I am requesting an abatement of the Failure to Pay penalty assessed for the 2022 tax year due to reasonable cause. My business was forced to shut down for three weeks following a state-mandated emergency declaration on [Date], making it impossible to access my records and remit payment on time."

This kind of direct, factual opening immediately tells the agent what they need to know and sets a professional tone.

What to Include and What to Leave Out

The content and tone of your explanation matter more than you might think. Stick to the facts. Avoid overly emotional language or placing blame on the IRS. Just remember, the agent reviewing your form is a person doing a job—making their job easier can only work in your favor.

Do Include:

- Specific dates of events (e.g., "I was hospitalized from March 5 to March 20").

- Names of relevant parties, if applicable (e.g., "My long-time accountant, John Smith, passed away unexpectedly").

- Facts that demonstrate you tried to comply.

- A brief list of the evidence you're attaching (e.g., "Attached are copies of my hospital admission records and a letter from my doctor.").

Don't Include:

- Vague excuses like "I was really busy" or "I forgot."

- Complaints about the tax system or how unfair the laws are.

- Emotional pleas that aren't backed up by hard facts.

- Unnecessary private medical details. Instead of describing a complex surgery, just stating the dates of hospitalization is sufficient.

Your explanation needs to be concise but complete. If you run out of room on the form, type your explanation on a separate sheet of paper, write "See Attached Statement" in the Line 7 box, and attach your letter. In my experience, this is often the best approach for complex situations because it allows you to present a clean, well-organized narrative that’s easy for the agent to follow.

Assembling Strong Supporting Documentation

Think of your explanation on Form 843 as the story, and your supporting documents as the undeniable proof. Without solid evidence, even the most legitimate reason for a Form 843 abatement is likely to be denied. The IRS agent reviewing your case needs to see a clear, direct line connecting the event you describe to your failure to file or pay.

Simply put, your request is only as strong as the evidence you bring to the table. The key is to carefully match your documentation to your specific "reasonable cause" argument. Each situation calls for a different set of proof points, and your goal is to present a professional, organized package that makes it easy for the IRS to say "yes."

Evidence for Serious Illness or Death

When you're citing a medical crisis or the death of a close family member, you have to show exactly how that event prevented you from managing your financial responsibilities.

- Hospitalization Records: Admission and discharge summaries are perfect. They establish a concrete timeline of when you were out of commission. Crucially, you do not need to provide sensitive, private medical details.

- Doctor's Note: A letter from a physician can be incredibly helpful. It just needs to confirm the dates you were under their care and state that your condition made it impossible to handle financial matters.

- Death Certificate: If the death of a family member is the reason for your delay, a copy of the death certificate is non-negotiable. You should also briefly explain your relationship and how their passing—or your duties as executor—threw your tax compliance off track.

Documentation for a Natural Disaster

If your troubles stem from a fire, flood, hurricane, or another disaster, your evidence needs to paint a vivid picture of the event's devastating impact. The goal is to prove the disaster happened and that it directly affected you or your business.

- Insurance Claims: Copies of claims filed with your home or business insurance carrier are powerful.

- Photographs: Dated pictures showing the damage to your property, office, or records can be very persuasive.

- Official Declarations: Include a copy of the federal or state disaster declaration for your area. You can usually find these on FEMA’s website or your state government's emergency management page.

Proving Reliance on Incorrect IRS Advice

This one is notoriously tough to prove, but it's a winner if you have the right documentation. You must demonstrate that you specifically asked for guidance, the IRS gave you bad information, and you relied on that advice in good faith.

The burden of proof here is high. Your best evidence will always be contemporaneous notes. Make it a habit: after any call with the IRS, jot down the date, time, the agent's name or ID number, and the specific advice they gave you.

This kind of meticulous record-keeping can be the single factor that tips the scales in your favor. For a deeper dive into what qualifies, our guide on the abatement of penalties for reasonable cause has more real-world examples.

To help you get started, here is a quick checklist of the kind of evidence you’ll need for the most common reasonable cause claims.

Evidence Checklist for Common Reasonable Cause Claims

| Reasonable Cause Scenario | Primary Evidence | Secondary Evidence |

|---|---|---|

| Serious Illness | Hospital admission/discharge records | Doctor's note confirming incapacity, prescription records |

| Death in Family | Death certificate | Proof of relationship (e.g., birth certificate), executor appointment letters |

| Natural Disaster | Insurance claims, repair estimates | Dated photos of damage, official disaster declarations |

| Records Destroyed | Police or fire department report | Photos of damage, insurance claim for record loss |

| Bad IRS Advice | Contemporaneous notes from call (date, agent ID, advice) | Copy of IRS written correspondence with incorrect information |

| Postal Service Error | Proof of mailing (e.g., certified mail receipt) | Written statement from postal worker, if possible |

This isn't an exhaustive list, but it covers the core documents the IRS will be looking for. Always aim to provide clear, direct proof that backs up every part of your story.

Presenting Your Evidence Professionally

How you package your documents really matters. Don't just cram a messy stack of papers into an envelope and hope for the best.

- Lead with a Cover Letter: Start with a simple cover letter that lists every single document you're including. This serves as a helpful table of contents for the IRS agent.

- Organize It Logically: Arrange your documents in the same order you refer to them in your Line 7 explanation. This creates a story that’s easy for the agent to follow.

- Send Copies, Keep Originals: This is a big one. Never send original documents to the IRS. Make clear, high-quality copies and store your originals somewhere safe. Knowing how long to keep your financial documents is also a good practice for the future.

By putting together a well-organized and thoroughly documented claim, you dramatically increase your odds of a successful Form 843 abatement. You also show the IRS that you're a responsible taxpayer who just ran into an obstacle you couldn't overcome.

Getting Your Form 843 Filed and What to Do Next

You’ve carefully put together your Form 843 and all your supporting evidence. Now comes the final, crucial part: getting it submitted correctly and knowing how to handle the follow-up. Getting these last steps right is just as important as all the prep work you've already done.

Where and How to Send Your Request

The mailing address for your Form 843 isn't one-size-fits-all. It actually depends on the specific tax and penalty you're trying to get abated.

As a rule of thumb, you'll send it to the same IRS service center where you filed the original return that triggered the penalty. Check the IRS notice you received—the address is often listed there. If you can't find it, the IRS website has a list of filing addresses you can reference.

Here’s a pro tip that can save you a world of headaches: always use U.S. Certified Mail with a return receipt. Yes, it costs a few extra dollars, but it's worth every penny. You get a stamped receipt as proof of mailing and a signature confirmation when the IRS physically receives your package. This paper trail is invaluable if your submission is ever questioned or gets lost in the shuffle.

The Waiting Game: Managing Expectations

Once you've mailed your form, the waiting begins. It’s important to set realistic expectations because this is rarely a quick process. The timeline for a decision on a Form 843 abatement can vary quite a bit depending on how complex your situation is.

For a straightforward First-Time Abatement request, you're generally looking at a two to three-month wait for a decision. However, claims based on "reasonable cause" require a much more detailed investigation by an IRS agent, and that can easily stretch the wait to three or four months, sometimes longer.

Keep in mind that while your request is pending, failure-to-pay penalties and interest will continue to rack up if you haven't paid the underlying tax. This is a strategic point to consider. Paying the base tax you owe can stop the clock on these additional charges while you wait for a decision on the penalty itself. You can find more practical insights about these timelines by reviewing the IRS penalty abatement information from HRBlock.com.

What to Expect in the Mail: Interpreting the IRS Decision

After a few months, a letter from the IRS will arrive with their decision. It’s going to be one of two things, and your next move depends entirely on what it says.

- Approval Notice: If your request is granted, congratulations! You'll receive a notice confirming the penalty has been wiped out. If you already paid the penalty, a refund check will follow.

- Denial Letter: If your request is turned down, the IRS will send a letter explaining why. This isn't necessarily the end of the road.

This is Critical: That denial letter is the most important piece of paper you can receive. It outlines your appeal rights. Do not throw it away or ignore it. The clock for your next move starts ticking the moment you receive it.

Your Right to Appeal a Denial

If the IRS denies your Form 843 abatement request, you have the right to fight their decision. The denial letter will clearly state that you have 30 days to file a formal protest and ask for a hearing with the IRS Independent Office of Appeals.

This is a big deal. The Office of Appeals is a separate branch within the IRS, and their job is to provide a fresh, impartial review of your case. An appeals officer who had nothing to do with the initial denial will re-examine all your evidence and arguments.

Frankly, this is the point where professional help becomes almost essential. An experienced Michigan tax attorney can dissect the IRS's reasoning for the denial, help you craft a much stronger argument for your appeal, and represent you at the hearing. They know the ins and outs of the appeals process and can dramatically increase your odds of turning that initial "no" into a "yes."

Missing that 30-day window could mean you forfeit your right to appeal entirely, so you have to act quickly and strategically.

Common Questions About Form 843 Abatement

Once you've sent Form 843 off to the IRS, a whole new set of questions tends to pop up. Let's walk through some of the most common ones we hear from Michigan taxpayers. Knowing the answers can help you set realistic expectations and navigate what comes next.

Can I Use Form 843 to Get Rid of Interest Charges?

This is probably the number one question people ask. The short answer is usually no—at least not directly. The IRS is required by law to charge interest on unpaid taxes, so you can't simply request an interest abatement based on "reasonable cause."

But here’s the good news: if the IRS approves your penalty abatement, they will automatically remove any interest that was charged on that specific penalty. So, if they forgive a $1,000 penalty, the interest tied to that $1,000 goes away with it. Just remember, this doesn't touch the interest that's been building on the original tax you owed.

There are very rare exceptions, like when an unreasonable error or delay was caused by an IRS employee, but for most people, the interest abatement is a side effect of a successful penalty abatement.

What Happens If the IRS Denies My Request?

A denial letter can feel like a final blow, but it’s not the end of the road. You absolutely have the right to appeal.

Your denial notice will lay out your appeal rights and, most importantly, give you a deadline to file a protest—you typically only have 30 days. This is a firm deadline, so you can't afford to sit on it.

Filing an appeal sends your case to the IRS Independent Office of Appeals. This is where an impartial officer, who had nothing to do with the initial decision, gives your situation a fresh look. This is a crucial point in the process where having an experienced tax attorney in your corner can make a world of difference.

Should I Pay the Penalty While My Form 843 Is Being Processed?

This is a strategic call, and it really comes down to your financial circumstances. If you don't pay the penalty, interest keeps piling up on it while you wait for the IRS to make a decision. If your request is denied, you'll be on the hook for the penalty plus all the interest that accrued in the meantime.

To avoid that headache, many people choose to pay the penalty in full and then file Form 843 as a "Claim for Refund." If your request is approved, the IRS simply sends you a check for the amount you paid. This is often the safest play to prevent the debt from getting any bigger.

Is There a Deadline for Filing Form 843?

Yes, and the IRS is incredibly strict about it. You're up against the statute of limitations.

To claim a refund for a penalty you already paid, you must file Form 843 within three years from the date you filed the original tax return or two years from the date you paid the tax—whichever is later.

If you never filed a return for that tax period, the clock is set at two years from the date you paid the tax. Miss this window, and your claim will be denied, even if you have a rock-solid "reasonable cause" argument. This is why it’s so critical to act quickly.

Sometimes, a penalty is just one piece of a much larger tax puzzle where the underlying debt itself is unaffordable. In those cases, you might need a different strategy altogether. You can learn more about how to tackle significant tax debt by exploring our guide on the Offer in Compromise program.