What Is Penalty Abatement and How Can It Help You?

Penalty abatement is a formal request to the IRS asking them to remove—or abate—penalties they've added to your tax account. It’s a form of tax relief designed for people who have a legitimate reason for not filing, paying, or depositing their taxes on time.

Think of it as a financial second chance when an honest mistake was made.

Understanding IRS Penalty Abatement

Let's use an analogy. Imagine you have a perfect driving record, but one day, you're rushing a family member to the emergency room and get a speeding ticket. You could later go to court and explain the circumstances. A reasonable judge might dismiss the ticket, acknowledging the emergency. You still have a responsibility to drive safely, but the penalty for that specific instance is forgiven.

IRS penalty abatement operates on a similar principle. It's not a secret loophole to avoid your tax bill. Instead, it’s an official process that acknowledges that life sometimes gets in the way. The IRS understands that unexpected events—a severe illness, a natural disaster, or even getting bad advice from a tax professional—can cause you to fall behind.

The Foundation of Penalty Forgiveness

At its heart, penalty abatement is about fairness. The tax system recognizes that while everyone has a duty to pay their taxes, it’s not always productive to penalize someone for a situation that was genuinely out of their control.

To get relief, you have to show the IRS that your failure to comply wasn't due to carelessness or a deliberate choice (willful neglect), but rather a specific, justifiable reason. Getting this right can save taxpayers thousands, sometimes even tens of thousands, of dollars.

And this kind of relief is more common than you might think. In a recent fiscal year, the IRS initially charged taxpayers $73.6 billion in civil penalties. However, they ended up abating $50.9 billion of that amount—a remarkable 69%. These penalty abatement trends show just how important it is to know your options.

Quick Guide to IRS Penalty Abatement Types

While the specific reasons can vary, most successful requests fall into one of three main categories. We'll dive deeper into each of these, but this table gives a quick overview of the main paths to getting penalties removed.

| Abatement Type | Primary Justification | Common Penalties Covered |

|---|---|---|

| First-Time Abatement | A clean compliance history for the past 3 years. | Failure to File, Failure to Pay, Failure to Deposit. |

| Reasonable Cause | Circumstances beyond your control prevented you from complying. | Most penalties, including accuracy-related penalties. |

| Administrative Waiver | You relied on erroneous written advice from the IRS. | Any penalty resulting directly from the wrong advice. |

Understanding which path best fits your circumstances is the first and most crucial step in building a compelling case for the IRS and getting back on solid financial ground.

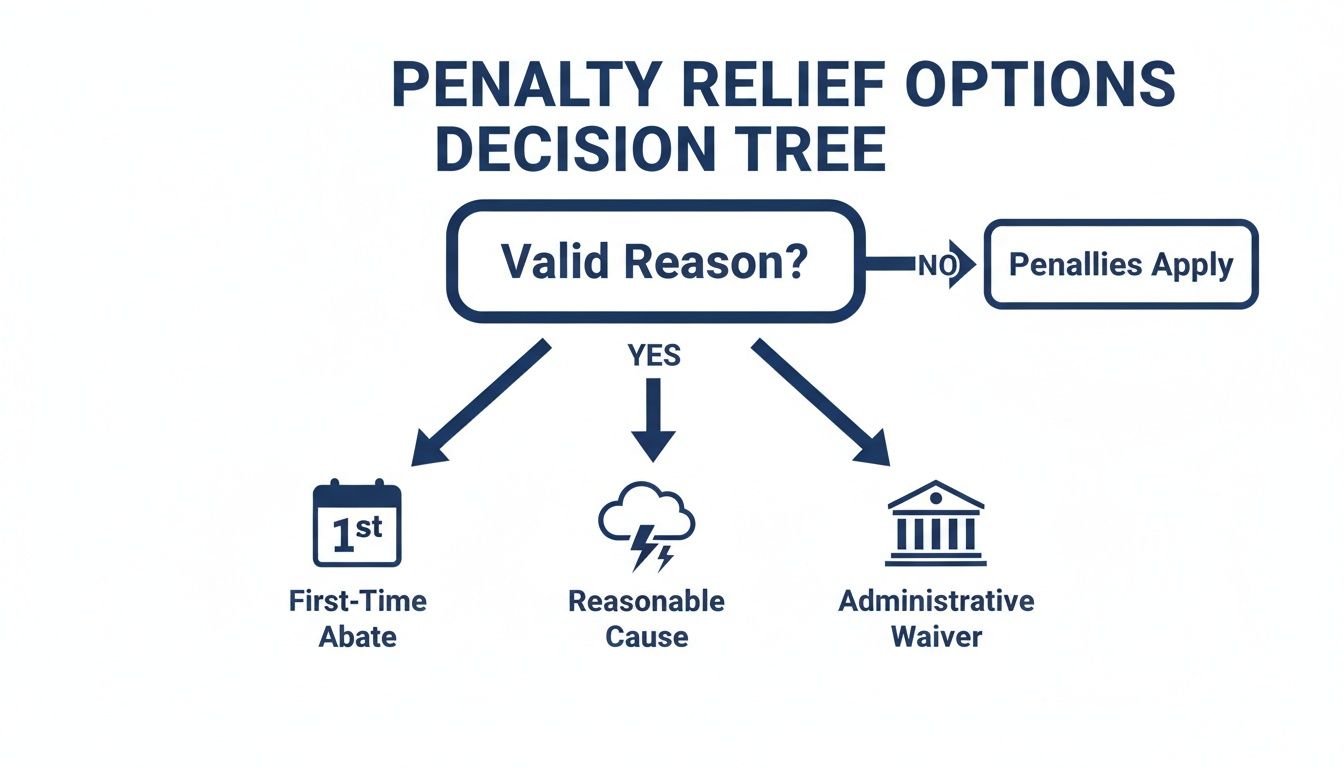

The Three Main Pathways to Qualify for Penalty Relief

Getting hit with an IRS penalty can feel like a final, non-negotiable judgment. But it's not. The tax code actually provides several ways to get relief, recognizing that sometimes, life just gets in the way. Knowing your options is the first step to building a solid case for penalty abatement.

Most successful requests fall into one of three main categories: First-Time Penalty Abatement, Reasonable Cause, and Administrative Waivers.

Think of these as different keys for the same lock. You don't need all of them; you just need the one that fits your specific situation. Your eligibility hinges entirely on the facts—from your past tax history to unforeseen events that threw you off course.

The decision tree below gives you a bird's-eye view of how a valid reason can steer you toward the right relief strategy.

As you can see, the journey begins with establishing a legitimate reason for the lapse, which then points to the best approach for your circumstances.

First-Time Penalty Abatement (FTA)

This is the simplest, most straightforward path to relief, often called the IRS's "one-time get out of jail free card." The First-Time Penalty Abatement (FTA) program is designed for taxpayers with a clean track record who just made a mistake. It’s an acknowledgment that even the most organized person can slip up.

To qualify for an FTA, you need to check three boxes:

- A Clean Slate: You can’t have had any IRS penalties in the three tax years before the year in question.

- You're Caught Up on Filing: You've filed all your required tax returns (or have a valid extension).

- You're Settled Up on Taxes: You have paid or have an arrangement to pay the underlying tax you owe.

What makes FTA so powerful is that your good history is your reason—no need to prove a catastrophic life event. The IRS is even moving to grant this relief automatically to about 1 million taxpayers annually, a major shift you can read more about in the IRS's initiative to automate penalty relief.

Reasonable Cause

What if you don't have a perfect three-year record? Your next best bet is to argue for Reasonable Cause. This is for situations where you couldn't file or pay on time due to circumstances completely beyond your control, even though you tried your best to comply.

When considering a Reasonable Cause request, the IRS essentially asks one question: "Did you do everything a normally careful and prudent person would do to meet your tax obligations, but were still unable to?"

You need to tell a compelling story and, more importantly, back it up with proof. Common grounds for Reasonable Cause include:

- Serious Illness or Death: A major health crisis affecting you or an immediate family member that made managing finances impossible.

- Natural Disasters: Fires, floods, or other disasters that destroyed your home, business, or records. For someone in Michigan, this could be a severe ice storm that knocks out power for weeks, paralyzing your ability to work.

- Inability to Get Records: Essential documents were lost, destroyed, or otherwise unavailable for reasons you couldn't control.

- Bad Advice or Errors: You relied on incorrect advice from a tax professional or made an unavoidable mistake despite taking proper care.

Unlike FTA, Reasonable Cause is subjective. Success depends on building a strong narrative supported by documents like hospital records, police reports, or dated correspondence.

Administrative Waivers and Statutory Exceptions

Finally, there's a third, less common pathway that covers specific, niche situations. These are penalty removals granted due to particular IRS policies or laws written by Congress.

The most well-known of these is an Administrative Waiver. This applies if you received erroneous written advice from an IRS employee. If you followed that bad advice and it led to a penalty, the IRS will typically waive it.

Statutory Exceptions are even rarer. These are exemptions written directly into the tax law itself. They apply to very specific circumstances and provide automatic relief if you meet the strict criteria. An experienced tax attorney can help you figure out if one of these long-shot exceptions might apply to your case.

How to Request Penalty Abatement Step by Step

Knowing you might qualify for penalty relief is one thing; actually asking the IRS for it is another. The process can feel daunting, but it's more straightforward than you might think. I always tell my clients to approach it like preparing for an important meeting: get your facts straight, organize your documents, and know exactly what you're going to say before you ever start writing.

But before you do anything else, there's one non-negotiable first step: you have to be in compliance. The IRS won't even look at a penalty forgiveness request until you're current on your obligations. That means every single overdue tax return is filed and you've either paid the tax you owe or have an approved payment plan in place.

Once you’ve taken care of that, you can officially make your request. The best way to do this really depends on your specific situation and the kind of relief you're after.

Choosing Your Method of Contact

Your first big decision is how to ask. Each option has its own pros and cons, and picking the right one is crucial.

- Verbal Request by Phone: For simple, clear-cut cases—especially a First-Time Penalty Abatement—a phone call might be all it takes. Just call the toll-free number on your IRS notice. Be ready to explain things clearly and have all your tax information right in front of you.

- Written Request via Letter: If you're building a case for Reasonable Cause, a formal letter is almost always the best bet. It gives you the space to lay out a detailed timeline, explain the nuances of your situation, and attach all your supporting proof.

- Official IRS Form 843: For some specific requests, especially if you're asking for a refund of penalties you've already paid, the IRS requires you to use Form 843, Claim for Refund and Request for Abatement. It's a structured form that guides you through presenting your case.

No matter which path you take, clarity is your best friend. A well-organized, logical request has a much higher chance of success.

Crafting a Persuasive Written Request

If you're writing a letter, remember that its quality can make or break your entire case. Your job is to build a compelling, fact-based narrative that convinces the IRS agent that your failure to file or pay on time was truly excusable.

Whether you're writing a letter or filling out Form 843, it absolutely must include these key pieces of information:

- Your Basic Info: Name, address, Social Security Number (or TIN), and the specific tax years involved.

- The Penalty Details: Clearly identify the exact penalties you want removed, including the dollar amounts. If you have an IRS notice, reference the notice number.

- A Clear Timeline of Events: Walk the agent through what happened, step by step. Explain the events that caused the tax problem and directly link them to why you couldn't file or pay on time.

- A Strong Reasonable Cause Argument: This is the heart and soul of your request. Explain why the penalties should be forgiven, referencing your specific circumstances (like an illness or natural disaster) and showing how you still tried to be responsible.

- Reference Your Proof: List every piece of evidence you're including and briefly explain what it proves.

Think of it this way: a successful penalty abatement request tells a story. It should guide the IRS agent through your hardship, highlight your good-faith efforts, and prove that the tax problem was an unfortunate anomaly caused by things you couldn't control.

Gathering and Submitting Your Request

Once your letter or form is ready, gather all your supporting documents. Make copies of everything—the request and all the evidence—for your own records. Don't skip this.

Send the entire package to the IRS using certified mail with a return receipt requested. This gives you undeniable proof of when they received it.

Finally, be patient. It can take the IRS several months to process an abatement request. If you get a denial letter, don't give up. You have the right to appeal the decision, but the clock is ticking—you typically have just 30 days to act. This is often the point where bringing in a professional can make all the difference.

Building a Compelling Case with Strong Evidence

When you ask the IRS to waive penalties, a good story isn't enough—you need to prove it. The burden of proof is 100% on you, the taxpayer, to show why you couldn't file or pay on time. Think of it like you're building a legal case, and every single claim you make has to be backed up with cold, hard facts.

Your job is to create a clear, undeniable narrative that directly connects your difficult circumstances to the tax delinquency. This isn't just about writing a letter; it's about assembling an organized file of documents that an IRS agent can quickly understand and verify. Without solid evidence, even the most sympathetic excuse will likely fall flat.

Tailoring Evidence to Your Reasonable Cause

Every situation is unique, and so is the proof required. The secret is to gather documents that are specific, dated, and, whenever possible, from an official third party. An IRS agent will always find a hospital admission record far more persuasive than a handwritten note saying you were sick.

Let's look at the kind of proof you'll need for some of the most common "Reasonable Cause" arguments:

-

Serious Illness or Injury: A simple doctor's note won't cut it. You need the heavy hitters: hospital admission and discharge papers, detailed statements from physicians explaining the severity of your condition, and records that show how your illness physically prevented you from managing your finances.

-

Death of an Immediate Family Member: A death certificate is the starting point, not the end. You also need to include documents that prove your relationship to the deceased. If you were the executor of the estate, for example, the legal documents appointing you to that role can powerfully illustrate how your responsibilities made it impossible to deal with your own taxes.

-

Natural Disaster or Fire: You need official documentation to back this up. Think FEMA disaster declarations for your county, insurance claim filings for property damage, and official police or fire department reports. Dated photos showing the damage to your home, business, or financial records are also incredibly effective.

-

Inability to Obtain Records: If your records were stolen, destroyed, or just plain inaccessible, you have to prove it. This could mean a police report detailing a burglary, a copy of a restraining order that kept you from your home, or even a paper trail of emails showing your repeated, unsuccessful attempts to get documents from a bank or former partner.

-

Bad Advice from a Tax Professional: This is a tough argument to win, but it’s not impossible. To succeed, you’ll need a signed statement from the tax pro admitting their mistake, a copy of the incorrect advice they gave you in writing, and proof that you gave them all the correct information to begin with.

Constructing a Clear Timeline

Once you’ve gathered all your documents, the next step is to arrange them chronologically. Your request letter should be a roadmap for the IRS agent, walking them step-by-step through the sequence of events. You’ll want to reference each piece of evidence along the way.

A successful penalty abatement request doesn't just list hardships; it connects the dots for the IRS. The letter should clearly state, "This event happened on this date, as you can see in Exhibit A, and as a direct result, I was unable to file my taxes, as demonstrated by Exhibit B."

This methodical approach turns a messy pile of papers into a coherent, persuasive argument. It signals to the IRS that you are serious, organized, and have a legitimate reason for your request. By making your case easy for them to follow and verify, you dramatically increase your chances of getting those penalties wiped away.

Navigating Federal vs. Michigan State Penalty Relief

Dealing with tax penalties is a headache. But for those of us in Michigan, it’s a double-decker headache. You’ve got the IRS on one side and the Michigan Department of Treasury on the other, and a big mistake many people make is thinking they play by the same rules.

They don’t. Not even close.

Assuming an IRS strategy will work for a state tax issue is like using a map of downtown Chicago to navigate Grand Rapids—you’ll end up frustrated and completely lost. Understanding the unique landscape of each agency is absolutely critical if you want to successfully resolve penalties at both the federal and state levels.

The Standard of Proof: Michigan vs. The IRS

The single biggest difference comes down to the legal standard you have to meet. With the IRS, the magic words are "Reasonable Cause." This means you have to show that you acted with ordinary business care and good sense but, for reasons beyond your control, just couldn't file or pay on time.

Michigan, however, often uses a different yardstick: "Good Cause." It sounds similar, but in practice, it’s often a much tougher standard to meet. The state doesn't just want to see that you had a hardship; they want proof that this specific hardship was the direct and undeniable reason you fell behind on your taxes.

Think of it this way: For the IRS, you can often build a compelling "Reasonable Cause" case by connecting several contributing factors. For Michigan's "Good Cause," you almost always need to draw a straight, undeniable line from one major event—like a severe illness or a natural disaster—directly to your tax problem.

Key Procedural and Policy Differences

Beyond the legal jargon, the actual day-to-day procedures and options are completely different. A cookie-cutter approach is a surefire way to get a denial letter from at least one, if not both, of these agencies. For instance, navigating an IRS tax settlement in Westphalia, MI, requires a totally different playbook than what you'd use for a state-level negotiation in Lansing.

To really see the contrast, let's put them side-by-side.

Comparing IRS and Michigan Penalty Abatement

Here’s a quick look at how the two agencies stack up when it comes to penalty relief.

| Aspect | IRS (Federal) | Michigan Department of Treasury (State) |

|---|---|---|

| Primary "Get Out Free" Card | First-Time Penalty Abatement (FTA) is a huge help for taxpayers with a clean 3-year history. | Michigan has no formal equivalent to the FTA program. Every request is judged on its own merit. |

| Legal Standard | Primarily "Reasonable Cause," which can be a more flexible standard. | Often "Good Cause," which is typically interpreted much more strictly. |

| Request Method | You have options: a phone call, a formal letter, or filing IRS Form 843. | The state almost always requires a formal written request or a specific state form, like Form 5572. |

| Supporting Evidence | The IRS will consider a wide range of documents to paint a full picture of your situation. | Michigan puts a very high value on official, third-party documentation that directly proves your claim. |

The bottom line is simple: you have to treat the IRS and the Michigan Department of Treasury as two completely separate opponents. Each one requires its own unique strategy and a carefully crafted argument tailored to its specific rules. If you don't, you could find yourself paying hefty state penalties that might have easily been waived at the federal level.

When Should You Hire a Tax Attorney for Abatement?

Knowing you can ask the IRS to waive a penalty is one thing, but deciding whether to handle it yourself or bring in a professional is a whole different ballgame. It's a crucial decision.

For some straightforward situations, a DIY approach can work just fine. But when the stakes get higher and the facts get complicated, the guidance of an experienced tax attorney isn't just helpful—it's essential.

A simple request for First-Time Penalty Abatement (FTA) is a perfect example of a situation you can often handle on your own. If your compliance history is clean for the past three years and you've filed and paid everything, a phone call or a clear, concise letter to the IRS might be all it takes to get that penalty wiped away, especially if the amount is small.

But the moment your case involves serious money, complex reasons, or a prior rejection from the IRS, the game changes. This is where professional help becomes a strategic necessity, not just a convenience.

Signs It’s Time to Call in a Pro

Certain red flags should tell you it's time to stop trying to navigate the system alone and call in an expert. Trying to manage these scenarios without legal counsel can easily lead to costly mistakes and missed opportunities for relief.

Think about hiring a tax attorney if you find yourself in any of these situations:

- The Penalty is Large: When you're looking at penalties in the thousands or even tens of thousands of dollars, the financial risk is simply too high to leave things to chance. An attorney ensures your case is presented as strongly and professionally as possible.

- Your Request Has Already Been Denied: If the IRS has already said "no" once, your next move is a formal appeal. This isn't just another letter—it's a legal process that demands a deep understanding of tax law and IRS procedure.

- You're Also Under Audit: An abatement request tangled up with an ongoing IRS audit adds serious layers of complexity. A tax attorney can manage both issues at once, making sure one doesn't negatively impact the other and protecting your interests across the board.

- Your 'Reasonable Cause' Argument is Complicated: Building a persuasive case based on messy business issues, convoluted financial records, or bad advice from a tax preparer requires a sophisticated legal argument. This is exactly what tax attorneys are trained to do.

The Value a Tax Attorney Brings to the Table

An experienced tax attorney does so much more than just fill out paperwork. They become your advocate, your negotiator, and your shield. To get started, you'll typically sign a Tax Power of Attorney form, which authorizes them to speak directly to the IRS on your behalf. No more waiting on hold for hours.

An attorney understands the subtle nuances of tax law that can make or break a case. They know precisely what kind of evidence an IRS agent is looking for and how to frame your story in the most compelling way.

This expertise is incredibly valuable. Tax laws and IRS procedures are always changing, and these shifts can create new opportunities for penalty relief that most taxpayers would never even hear about. An attorney stays on top of these developments.

Ultimately, when you're facing a significant tax problem, you don't just need to fill out a form; you need a strategy. At Defense Tax Partners, that's what we provide. We take over the stressful communications with the IRS and the Michigan Department of Treasury, build powerful arguments backed by solid evidence, and explore every possible path to relief.

Sometimes, that might even mean looking beyond abatement to other solutions. If you want to learn more, you can https://www.michigantaxattorneys.net/blog/what-is-an-offer-in-compromise/. If your tax penalties feel overwhelming, don't face them alone.

Common Questions About IRS Penalty Abatement

When you're staring down a penalty notice from the IRS, a lot of questions can start swirling. Even with a good grasp of the basics, the "what ifs" and "how longs" can be stressful. Let's clear up some of the most common things taxpayers ask when they're looking to get penalties waived.

How Long Do I Have to Request Penalty Abatement?

Timing is everything here, and the clock is definitely ticking. The IRS generally gives you a specific window to ask for relief: three years from the date you filed your return, or two years from when you actually paid the tax—whichever date is later.

This deadline is officially called the Refund Statute Expiration Date (RSED). Miss it, and the door to relief slams shut, no matter how compelling your reason is.

Does Requesting Abatement Stop IRS Collections?

No, and this is a critical point to understand. Just sending in a penalty abatement request doesn't put a pause on IRS collection actions. If they've already started the process for a bank levy or wage garnishment, that train keeps moving while they review your case.

If you’re under threat of active collection, you have to deal with that separately. Abatement is about removing the penalty itself, not stopping the collection of the underlying tax you owe. You'll need to look into other solutions, like an installment agreement or requesting a temporary hold, to stop those more aggressive actions.

Can I Get Penalties Removed if My Tax Preparer Made a Mistake?

Yes, this is definitely a possibility, but the burden of proof is on you. This situation falls squarely under the Reasonable Cause argument. You'll have to show the IRS that you did your part by acting with ordinary business care and prudence—meaning you gave your preparer all the correct information in a timely manner.

To make this argument stick, you have to prove the mistake was your preparer's, not yours. Evidence is key here. A sworn statement from the preparer admitting the error or a clear email trail showing you provided the right documents can make or break your case.

What Happens if the IRS Denies My Abatement Request?

An initial "no" from the IRS doesn't have to be the final answer. You have the right to appeal the decision. Your case will go to the IRS Independent Office of Appeals, where a new officer—someone who had nothing to do with the first denial—will give it a fresh look.

But be aware, you only have 30 days from the date on the denial letter to file your appeal. This is where things get serious and having a professional in your corner can make a huge difference. An appeal requires a strong, structured legal argument. Navigating the maze of federal and state tax law is tough, but the experienced team at Defense Tax Partners can guide Michigan taxpayers through every step of this complex process.