Fresh Start Tax Relief: fresh start tax relief – Quick Solutions for Tax Debt

When you're staring down a mountain of tax debt, it's easy to feel like you're completely on your own. But there’s a genuine lifeline available: fresh start tax relief. This isn't just one single program, but rather a collection of IRS policies built to help people like you get back on solid ground without causing a financial catastrophe. It's a structured path back to good standing.

What The IRS Fresh Start Program Really Means For You

Think of the IRS Fresh Start Initiative less as a formal "program" and more as a shift in philosophy. The IRS came to realize that hammering taxpayers with aggressive collection tactics wasn't always the most effective way to get what they were owed. Instead, they created structured, realistic ways for people to manage and ultimately resolve their tax liabilities.

The whole point is to find a solution that allows you to pay what you can reasonably afford, rather than demanding a lump sum that would push your family's finances over a cliff.

This initiative opens up several different avenues for relief, and we'll walk through each one in this guide. The main options you'll encounter are:

- Offer in Compromise (OIC): This is a powerful tool that allows certain taxpayers to settle their entire tax debt with the IRS for less than the full amount they owe.

- Installment Agreements (IA): These are essentially structured payment plans. They let you chip away at your tax debt over time with manageable monthly payments.

- Lien Withdrawal and Subordination: These options provide ways to deal with federal tax liens, which can be crucial for protecting your credit and your ability to get a loan.

A More Flexible Approach To Tax Collection

One of the most significant changes that came out of the Fresh Start Initiative was making it much harder for the IRS to slap a lien on your property. When the initiative first launched back in 2011, it immediately raised the minimum debt amount required for the IRS to file a Notice of Federal Tax Lien from $5,000 to $10,000.

That single change had a massive impact. Between 2010 and 2023, the number of liens filed each year dropped by nearly 76%. It was a clear signal that the IRS was willing to work with taxpayers, not just against them. You can read more about these historical changes and their effects on taxpayer relief programs at CBSNews.com.

To help you get a clearer picture of the options, we’ve put together a quick comparison table.

Overview of Fresh Start Tax Relief Options

| Relief Option | What It Does | Best For |

|---|---|---|

| Offer in Compromise (OIC) | Settles your tax liability for a lower amount than you originally owed. | Taxpayers with significant debt who can prove they lack the income and assets to pay it in full. |

| Installment Agreement (IA) | Sets up a monthly payment plan to pay your full tax debt over an extended period. | Those who can't pay the full amount now but can afford consistent monthly payments over time. |

| Currently Not Collectible (CNC) | Temporarily pauses IRS collection efforts due to severe financial hardship. | Individuals experiencing extreme financial difficulty (e.g., unemployment, illness) who cannot afford any payments. |

| Penalty Abatement | Removes or reduces penalties assessed on your tax debt for a valid reason. | Taxpayers who have a "reasonable cause" for failing to file or pay on time, like a death in the family or a natural disaster. |

Each path is designed for a different financial situation, so understanding which one fits your circumstances is the critical first step.

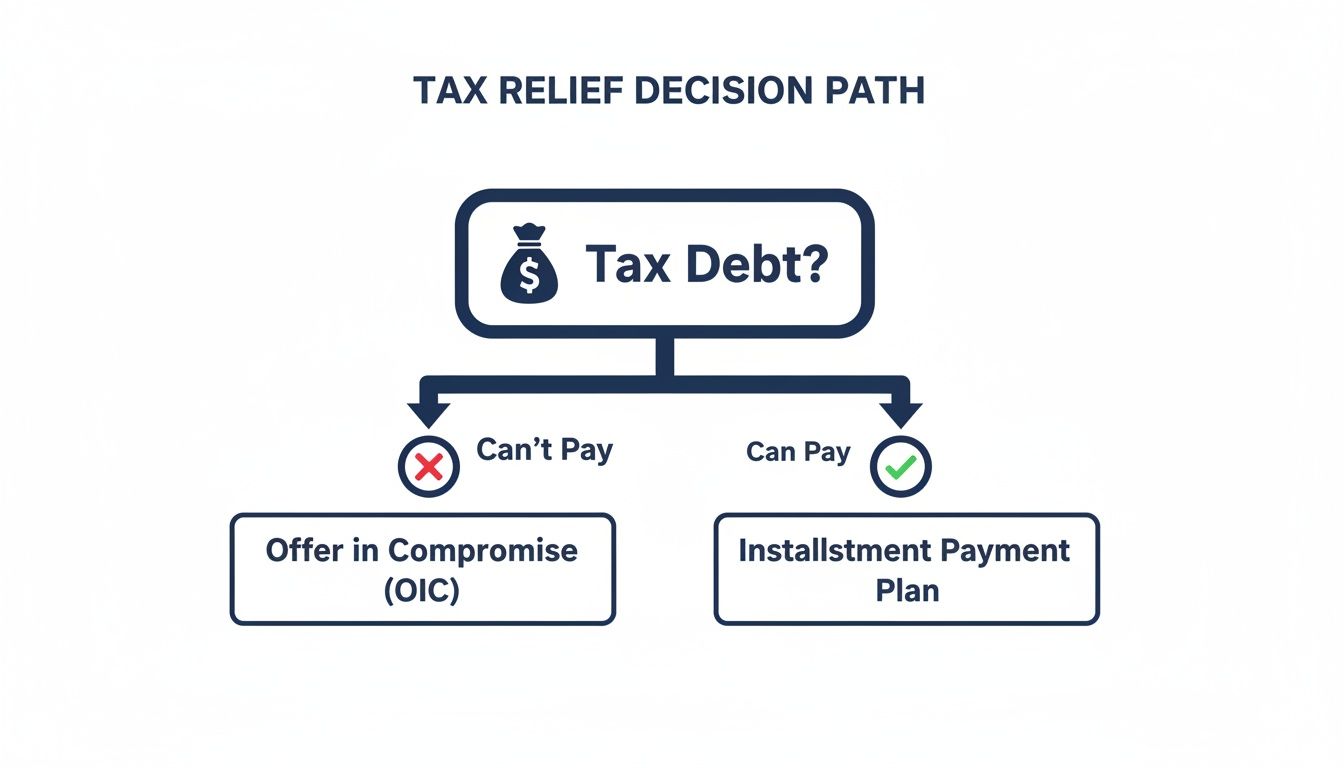

This infographic helps visualize the decision-making process you'll go through when exploring your options.

As you can see, the right path forward really boils down to your ability to pay. It will guide you toward either a settlement (like an OIC) or a payment plan. For some, there's another possibility: being temporarily deemed uncollectible. You can learn much more about how the IRS Currently Not Collectible status works in our guide.

Settling Tax Debt with an Offer in Compromise

Of all the fresh start tax relief tools, the Offer in Compromise (OIC) is easily the most well-known—and often, the most misunderstood. It’s the closest thing to a "tax settlement" that exists, allowing you to resolve a federal tax debt for less than what you originally owed.

Think of it as a formal negotiation. You're not just asking for forgiveness; you're presenting a detailed financial case to the IRS proving that paying the full amount would cause an extreme economic hardship.

When the IRS accepts an OIC, it’s a business decision. They’ve concluded that the amount you're offering is the most they can realistically expect to collect before the legal time limit on your debt expires. For taxpayers trapped under a mountain of tax debt, it can be a powerful lifeline.

Who Qualifies for an Offer in Compromise

Qualifying for an OIC is a high bar. The IRS scrutinizes every detail of your financial life—your income, your regular living expenses, and the equity you have in any assets like a home or car.

This isn't a program for someone who just had a rough year. It’s designed for situations where a major life event has permanently changed your ability to pay.

Picture a small business owner in Detroit whose primary client suddenly went bankrupt, wiping out most of their income for good. Or a family in Grand Rapids now buried in medical debt from a serious illness. These are the kinds of circumstances where an OIC can become a legitimate pathway to financial recovery.

An Offer in Compromise hinges on a specific IRS calculation called your "Reasonable Collection Potential" (RCP). This is the formula they use to determine the minimum amount they believe they could collect from you. A successful offer must meet or exceed that number.

Your job is to build a case that is so thorough and persuasive that the IRS has to agree with your assessment.

The Grounds for a Successful Offer

The IRS will generally only accept an OIC for one of three specific reasons. Figuring out which one fits your situation is the critical first step.

- Doubt as to Collectibility: This is the most common reason by far. It's used when your income and assets are simply not enough to pay your tax liability in full.

- Doubt as to Liability: This is a much rarer argument. It applies when you have legitimate evidence to prove that you don't actually owe the tax in the first place.

- Effective Tax Administration: This is a special consideration for unique cases where paying the debt, even if you technically could, would be unfair or create a severe economic hardship.

The OIC program is a core part of the Fresh Start Initiative, and its use has grown significantly. In 2023 alone, the IRS accepted over 33,000 Offers in Compromise from taxpayers. You can see more statistics on the historical growth of the OIC program with the Taxpayer Advocate Service.

Because the process is so demanding and reliant on perfect documentation, getting professional help can mean the difference between getting your offer accepted or rejected. An experienced tax attorney knows how to navigate the complex IRS rules, calculate your RCP correctly, and frame your financial story in the most compelling way possible.

Making Your Tax Debt Manageable with a Payment Plan

Think of it this way: if an Offer in Compromise is like negotiating a final, discounted settlement on a huge bill, an Installment Agreement (IA) is like setting up a practical monthly payment plan for that same bill. It’s one of the most straightforward paths to fresh start tax relief because it lets you pay what you owe over a set period, instead of forcing you to come up with a lump sum you just don't have.

This approach stops the bleeding, fast. As soon as your IA is approved, the IRS has to back off. The aggressive collection actions cease, which means no more threatening letters showing up in your mailbox. More importantly, it shields you from sudden wage garnishments or bank levies that can throw your entire financial life into chaos. You get a predictable monthly payment and a clear finish line for your tax problems.

For a lot of folks, this is the ideal solution. You're acknowledging the debt, but you're given a structured, manageable way to pay it off without completely derailing your life.

The Power of the Streamlined Installment Agreement

The Fresh Start initiative really opened the door for more people by creating the Streamlined Installment Agreement. As the name suggests, it simplifies the whole application process, but only if your total tax debt—including penalties and interest—falls under a certain amount. The big advantage here is that you typically don't have to submit a mountain of financial paperwork, making approval much quicker.

This program has become a cornerstone of Fresh Start tax relief, and the IRS has bumped up the eligibility limits over the years. It started out for debts of $25,000 or less, then jumped to $50,000, and now there's even a program for debts up to $100,000. The proof is in the numbers: in just one fiscal year, the IRS brought in about $10.7 billion through these agreements alone. You can find more details on the evolution of IRS Installment Agreements on TaxFortress.com.

The immediate benefit of a Streamlined Installment Agreement is the automatic stop to collections. For someone here in Michigan worried about a wage garnishment, getting this agreement in place offers instant protection and some much-needed breathing room while they get back on track.

This accessibility has been a game-changer for millions of taxpayers who can afford to pay off their debt over time, just not all at once.

Key Requirements for an IA

Even though the streamlined option is easier, there are a couple of hard-and-fast rules you have to follow to get any kind of Installment Agreement. Before the IRS will even talk about a payment plan, you must:

- File All Required Tax Returns: You can't have any outstanding returns from prior years. The IRS needs a complete picture of what you owe before they'll agree to a payment schedule.

- Be Current on Withholding/Estimated Taxes: You have to prove you're on the right track for the current tax year. This shows the IRS you're committed to not falling behind again.

Getting these two things in order is your first real step toward securing an IA and finally putting these tax issues in the rearview mirror.

Protecting Your Assets from Tax Liens and Levies

Many people use the terms "lien" and "levy" as if they mean the same thing. But in the world of IRS collections, they represent two very different stages of a worsening problem. Knowing the difference is your first line of defense in protecting your property.

Think of a tax lien as a warning shot. It's the government’s legal claim against your property—your house, car, or business assets—to secure their interest in the tax debt you owe. The IRS isn't seizing anything yet, but they're putting a public notice on the record that tells other creditors they get first dibs if you sell the asset.

A tax levy, however, is when the gloves come off. This is the actual seizure of your property. A levy is the IRS actively taking your car, draining your bank account, or garnishing your paycheck to pay off the debt. The goal is always to get things sorted out long before a lien ever escalates into a levy.

How the Fresh Start Initiative Reduces the Risk

The IRS Fresh Start program was designed to directly address the threat of liens by simply making them less frequent. One of the most significant changes was raising the minimum debt threshold that triggers the filing of a Notice of Federal Tax Lien (NFTL). This was a smart move by the IRS, preventing them from slapping liens on taxpayers with smaller balances.

This gives people crucial breathing room. It means taxpayers with more manageable debts aren't immediately hit with a public lien that can tank their credit and make it nearly impossible to secure a loan. This is a core part of what fresh start tax relief is all about: focusing on resolution, not just punishment.

A Notice of Federal Tax Lien is a public document. It can seriously damage your credit score for years, even after you’ve paid the debt. The best strategy is always to prevent it from being filed in the first place.

Solutions to Remove a Tax Lien

What if a lien has already been filed against you? Don't panic. The Fresh Start Initiative also created clear paths to get it removed, which is absolutely vital for your financial recovery.

- Lien Withdrawal: After you set up a Direct Debit Installment Agreement and prove you can make a few payments on time, you can often request a lien withdrawal. This pulls the public notice entirely, essentially erasing it from your credit report as if it never existed.

- Lien Subordination: This option doesn't remove the lien, but it lets another creditor jump ahead of the IRS in line. This can be a lifesaver if you need to refinance a mortgage or get a business loan, which in turn could give you the funds to pay off the tax debt.

By getting a payment plan in place, you not only stop a levy in its tracks but also open the door to reversing the damage from a lien. You can explore the specific steps required when you read our guide on how to remove tax liens. Taking decisive action is what keeps a financial roadblock from turning into a dead end.

How to Avoid Common Tax Relief Pitfalls

Taking the first step toward fresh start tax relief is a huge win, but navigating the process has its share of landmines. Knowing what they are ahead of time is the best way to build a solid case with the IRS and avoid a denial that puts you right back where you started.

One of the worst things you can do? Ignore those IRS notices piling up in your mailbox. Each letter comes with a deadline and a specific purpose. When you don't respond, the IRS sees it as a deliberate refusal to cooperate, which almost always escalates their collection efforts. It's like ignoring a small roof leak—before you know it, you've got a much bigger, more expensive problem on your hands.

Another classic mistake is trying to negotiate with the IRS before you're even in the game. To the IRS, "in the game" means you are fully compliant. Before they will even look at an Offer in Compromise or an Installment Agreement, you must have all of your past-due tax returns filed. They simply can't resolve a debt when they don't know the full amount you owe.

Getting the Financial Details Wrong

Submitting financial information that's incomplete or just plain wrong is a fast track to getting your application rejected. I’ve seen it happen time and again: someone applying for an Offer in Compromise conveniently "forgets" to list a small savings account or puts down a wildly inaccurate value for their car. To an IRS agent, this isn't a simple oversight—it's a major red flag that calls your entire story into question.

This is where meticulous record-keeping becomes your best friend. Keeping your financial documents in order is non-negotiable, and modern tools can make a world of difference. For instance, using good receipt scanning apps for taxes and expense tracking can help you create a bulletproof record of your expenses.

A successful tax relief application tells a clear, consistent, and verifiable financial story. Any missing chapter or factual error gives the IRS a reason to close the book on your case.

Finally, a lot of people underestimate just how complex the required paperwork is. This leads to simple, avoidable errors that end up costing them dearly. If it’s penalty relief you’re after, for example, you'll need to know exactly how to file a request for abatement using IRS Form 843.

The application process is designed to be tricky. Below are some of the most common stumbles we see taxpayers make and how a professional approach makes all the difference.

Fresh Start Application Pitfalls and Solutions

| Common Mistake | Why It's a Problem | How We Can Help |

|---|---|---|

| Ignoring IRS Notices | This allows penalties and interest to accumulate and can trigger aggressive collection actions like liens or levies. | We immediately establish communication with the IRS on your behalf, pausing collection activity while we build your case. |

| Filing with Unfiled Returns | The IRS will automatically reject any relief application if you aren't fully compliant with your filing obligations. | Our team can prepare and file all your back taxes quickly and accurately to get you into compliance and eligible for relief programs. |

| Inaccurate Financials | Understating income or assets, even by accident, destroys your credibility and leads to an immediate denial. | We conduct a thorough financial analysis to ensure your forms are precise, complete, and present your situation in the most favorable light. |

| Applying for the Wrong Program | Choosing a relief option you don't actually qualify for wastes time and can result in a denial that goes on your record. | We analyze your unique tax and financial situation to identify the specific relief program you have the highest chance of qualifying for. |

Getting every detail right from the start is the key. Having an expert in your corner ensures that your application doesn't just get filed—it gets approved.

Answering Your Questions About IRS Fresh Start Relief

When you're trying to get a handle on tax debt, questions always come up. It's completely normal. Here are some clear, practical answers to the questions we hear most often from clients just like you.

I'm Self-Employed. Can I Still Get Relief Through This Program?

Absolutely. In fact, self-employed individuals and small business owners are often prime candidates for the Fresh Start program.

The IRS will want to see two key things from you: that you're caught up on filing all your past-due tax returns and that you're making your current estimated tax payments. From there, they'll look at your business's real-world financial situation—income, expenses, and overall viability—to figure out which relief option makes the most sense.

If I Apply for an Offer in Compromise, Will the IRS Stop Collections?

For the most part, yes. Once the IRS officially accepts your Offer in Compromise (OIC) application for review, they usually hit pause on aggressive collection actions like wage garnishments or bank levies.

This gives you some much-needed breathing room while your offer is being evaluated. But be warned: this protection only kicks in if your application is complete and properly submitted. Any mistakes can get it kicked back, leaving you exposed.

While an accepted OIC application provides a temporary shield, the review process itself can drag on for months. Keep in mind that the clock on the statute of limitations for collecting your debt also stops during this period. If your offer is ultimately denied, you could find yourself right back where you started.

What Happens if My Financial Situation Changes After I Set Up a Payment Plan?

Life happens. If you lose a job, have a medical emergency, or your income drops and you suddenly can't afford your agreed-upon monthly payments, the worst thing you can do is nothing.

You need to contact the IRS immediately. It's often possible to rework the terms of your Installment Agreement or even see if you now qualify for a different option, like an Offer in Compromise. Ignoring the problem will cause you to default on the agreement, making it void and triggering the IRS to resume aggressive collection efforts.

Does the Fresh Start Initiative Also Apply to My Michigan State Taxes?

No, and this is a critical distinction. The IRS Fresh Start Initiative is a federal program that only applies to tax debt you owe the IRS.

The Michigan Department of Treasury has its own set of tax relief programs, which include things like installment agreements and their own version of an offer in compromise. While the names sound similar, the eligibility rules, application processes, and standards for acceptance are completely different. You have to tackle your federal and state tax debts as two separate problems.