How to file back tax returns: Quick, Clear Steps

The weight of unfiled tax returns can feel crushing, but getting compliant is a straightforward process. It boils down to gathering your old financial records, grabbing the right tax forms for those past years, and filing everything in the correct order.

I can't stress this enough: the worst thing you can do is nothing. If you wait too long, the IRS might file a Substitute for Return (SFR) for you, and trust me, you don't want that. It will almost certainly overstate what you owe.

Taking the First Steps to Resolve Unfiled Taxes

It’s easy to feel stuck when you're facing several years of unfiled taxes. But every day you wait, the penalties and interest just keep piling up. The IRS has a long memory. If you don't file, they can and will create that SFR on your behalf, using only the income information they've received from places like your employer or bank.

This automated guess almost always leads to a much higher tax bill—sometimes by as much as 40-50%—because it ignores every single deduction and credit you were entitled to. Imagine someone else doing your taxes but only including the parts that cost you money. That's an SFR. The only way to fix it is to regain control by filing an accurate return yourself.

Create Your Action Plan

The key is to have a clear methodology to tackle this systematically. You don't have to fix it all in one weekend. Just focus on a few key objectives to get the ball rolling.

- Figure Out the Scope: First, pin down exactly which tax years you missed. As a general rule, the IRS wants the last six years filed to consider you compliant, but your situation might require more or less.

- Start the Paper Chase: Begin hunting down all your financial documents. This means W-2s from old jobs, 1099s from freelance work, and any receipts or bank statements that prove business expenses or deductions.

- File in Order: This is non-negotiable. You have to file chronologically, starting with the oldest year first. This is critical because things like losses or credits can carry forward, and filing out of order messes all of that up.

Breaking it down this way turns a massive, intimidating problem into a series of smaller, manageable tasks. You’re not just shuffling papers; you’re accurately rebuilding your financial story.

A lot of people I've worked with assume they're in for a huge tax bill. But you'd be surprised how often they discover they were actually due a refund, especially if they had taxes withheld from their paychecks all along. You won't know until you file.

Why You Should Act Now

The fallout from unfiled taxes goes way beyond what you might owe. It can stop you from getting a mortgage, jeopardize a professional license, and even hold up your Social Security benefits when you're ready to retire.

Taking the initiative to fix this shows the IRS and state tax agencies that you’re acting in good faith. That simple act can make a world of difference if you later need to negotiate a payment plan or ask for penalty relief.

You're not alone in this. Millions of people face this exact problem every year and get through it. By following a plan, you can go from feeling overwhelmed and uncertain to being in control of your financial future.

Assembling Your Past Financial Records

Let's be honest, the biggest hurdle for most people trying to file old tax returns is simply finding the paperwork. It’s a scavenger hunt through years of forgotten files, and the thought of it is often more paralyzing than the taxes themselves. But here’s what I tell my clients: piecing together your financial past is absolutely doable, even if you’re starting from scratch. You just need to know where to look.

Your first move shouldn't be digging through shoeboxes. It should be going straight to the source: the IRS. They keep detailed records of all income reported under your Social Security number, and this data is your single most powerful tool for this entire process.

Your Best Friend: The IRS Transcript

The IRS provides a free "Get Transcript" service, which is the fastest way to get your hands on the official income data they have on file for you. There are a few different types of transcripts available, but the one you need is the Wage and Income Transcript.

This document is a goldmine. It lists all the information returns the IRS has received in your name, including:

- W-2s from your employers

- 1099 forms (like 1099-NEC or 1099-K for freelance and gig work)

- 1099-INT and 1099-DIV for interest and dividend income

- 1098 forms showing mortgage interest you paid

You can get these transcripts instantly online through the IRS website. If you prefer, you can also mail in Form 4506-T, Request for Transcript of Tax Return, but be prepared to wait a few weeks. This transcript gives you the baseline for accurately reporting every penny of income.

Don't Forget the Other Side of the Ledger: Your Expenses

While the IRS has a great view of your income, they have zero visibility into your deductible expenses. This is where your own records become mission-critical, especially if you're self-employed. Forgetting deductions is like leaving money on the table for the IRS to pick up. As you start this process, figuring out how to organize receipts with a good system will save you a world of headaches.

I recently worked with a freelance graphic designer from Oakland County who hadn't filed in three years. His IRS transcripts showed over $180,000 in 1099 income, and he was staring down a massive tax bill.

He knew he had business expenses, but the records were a mess. So, we started rebuilding.

- First, we went through every bank and credit card statement, highlighting and categorizing business-related purchases like software, supplies, and web hosting.

- Next, we had him search his email for words like "receipt" and "invoice" to dig up digital proof of his spending.

- Finally, we reconstructed his business mileage by looking at his old calendars and project files to see when he drove to client meetings.

That deep dive uncovered over $60,000 in legitimate business expenses he almost missed. By meticulously putting the pieces back together, we dramatically lowered his taxable income and made his tax debt far more manageable.

Key Takeaway: Your IRS transcript only tells half the story—your income. You are responsible for documenting the other half—your expenses and deductions. A little bit of digging can turn a terrifying tax bill into something you can actually handle.

File From Oldest to Newest. No Exceptions.

Once you have your documents, you need to file the returns in chronological order. Start with the oldest unfiled year and work your way forward. This isn't just a helpful tip; it's a procedural necessity.

Filing in order ensures that items from one year correctly carry over to the next. For example, a business loss in 2019 could be used to offset income in 2020. If you file 2020 first, you lose that benefit. Filing out of order messes up the math and can create a cascade of errors that will only cause more problems with the IRS later on.

Getting Your Hands on the Right Federal and Michigan Tax Forms

One of the first traps people fall into when tackling back taxes is grabbing the most recent tax forms. I’ve seen it happen countless times—someone tries to file a 2018 return using the latest Form 1040. It’s a surefire way to get your return rejected right out of the gate.

Tax laws aren't static; they change every single year. The deductions, credits, and even the tax brackets are a snapshot in time. You absolutely must use the specific forms and instructions that were in effect for the exact year you're filing. This goes for both your federal and Michigan returns.

Securing the Right Federal Tax Forms

The good news is the IRS isn't trying to hide these old forms from you. They keep a comprehensive library of everything you could possibly need on their website. Just look for the "Prior Year Forms & Publications" section.

Your main target will be Form 1040, U.S. Individual Income Tax Return, for the specific year you need. Filing for 2019? You need the 2019 version of the 1040. Don't stop there, though. You also need to grab the instructions for that year. That booklet is your roadmap, containing the precise standard deduction amounts, tax tables, and credit rules that applied back then.

But what if the IRS has already stepped in and filed for you? This is called a Substitute for Return (SFR), and it's never in your favor. In that case, you can't just send in a regular 1040. You have to file Form 1040-X, Amended U.S. Individual Income Tax Return, to set the record straight and claim all the deductions and credits the IRS ignored.

A Pro Tip From Experience: When you're using a 1040-X to override an SFR, do yourself a favor and write "Substitute for Return" clearly at the top of the form. This little note acts as a signpost for the IRS agent reviewing your file, helping them understand exactly what you're correcting and potentially speeding things up.

Finding Michigan State Tax Forms

The process is pretty much the same for your state obligations. The Michigan Department of Treasury maintains its own online archive of prior-year tax forms. You'll be looking for the MI-1040, Michigan Individual Income Tax Return, for each specific year you're catching up on.

And just like with the federal returns, grabbing the corresponding instruction booklet is non-negotiable. It’s the only way to know the specific rules for Michigan exemptions or to see if you qualified for things like the property tax or home heating credits in a particular year.

E-Filing vs. Paper Filing for Back Tax Returns

Once your returns are accurately prepared, you need to get them filed. When you're dealing with past-due returns, your options for how to submit them become a bit more limited than they are for a current-year filing. Here’s a quick breakdown of what to expect.

| Filing Method | Available Years | Average IRS Processing Time | Confirmation of Receipt | Common Issues |

|---|---|---|---|---|

| E-Filing | Current year + 2 prior years | 2-4 weeks | Instant electronic confirmation | Limited to recent years only. |

| Paper Filing | All prior years | 6+ months (or longer) | Requires certified mail for proof | Extremely slow; risk of lost mail; no status updates. |

For returns that are more than a few years old, you're pretty much stuck with paper filing. The IRS systems just aren't set up to electronically accept returns beyond a certain window.

If you have to go the paper route—and for many unfiled returns, you will—don't just drop them in a blue mailbox and hope for the best. Always use a tracked service like USPS Certified Mail with Return Receipt. That receipt is your legal, postmarked proof that you filed and when. It’s a small, inexpensive step that can save you from a massive headache down the road.

This kind of careful documentation is crucial in all IRS dealings. For instance, the detailed financial proof required for an Offer in Compromise is a perfect example of why precision matters. You can see just how thorough you need to be in our guide on Form 433-A (OIC). Being diligent in how you submit your returns is a simple form of self-defense.

Understanding and Mitigating Tax Penalties

The real financial pain of unfiled returns isn't just the tax you originally owed—it's the penalties and interest that quietly snowball over time. The IRS has specific penalties that can quickly turn a manageable debt into a serious financial crisis, which is why tackling them is a critical part of filing back taxes.

Ignoring the problem is truly the most expensive mistake you can make. These penalties are designed to encourage compliance, and they add up alarmingly fast. The two big ones you'll almost certainly encounter are the Failure to File and Failure to Pay penalties.

The High Cost of Waiting

The Failure to File penalty is notoriously harsh. The IRS charges 5% of your unpaid taxes for each month or even part of a month that your return is late. This penalty keeps climbing until it hits a cap of 25% of your unpaid tax bill.

In contrast, the Failure to Pay penalty is much lower at 0.5% per month, though it also maxes out at 25%.

If both penalties happen to apply in the same month, the Failure to File penalty gets reduced by the Failure to Pay amount. But the main takeaway here is crystal clear: the penalty for not filing is a staggering 10 times higher than the penalty for not paying. This is exactly why your first move should always be to file those back returns, even if you don't have a dime to pay toward the balance. On top of all this, interest compounds daily on both the unpaid tax and the penalties themselves, making your debt grow even faster.

Seeking Penalty Relief Through Abatement

Just because the IRS slaps a penalty on your account doesn't mean it has to stay there. You can formally ask the IRS to remove or reduce penalties through a process called penalty abatement. It's a powerful tool, but you can't just ask nicely—you need a valid reason and the paperwork to back it up.

You generally have two main avenues for seeking penalty abatement:

- First-Time Abatement (FTA): This is your best shot if you have a good track record. You can often qualify if you've been compliant for the last three years (filed and paid on time), you've now filed all your required returns, and you've either paid the tax due or set up a plan to do so.

- Reasonable Cause: This argument is for situations where life simply got in the way. If circumstances beyond your control prevented you from filing or paying, you may have a case. This isn't for simple forgetfulness; you have to show that you acted with ordinary business care and prudence but were still unable to comply.

What counts as a valid "Reasonable Cause"? Think serious, documented events. A severe illness, a death in your immediate family, or a natural disaster that destroyed your records would all be strong arguments. Even getting incorrect advice from a tax professional can qualify. However, simply not having the money to pay your tax bill is not, on its own, considered a valid reasonable cause.

Building a Strong Case for Abatement

Successfully getting penalties removed comes down to building a persuasive, well-documented case. For example, identity theft is an increasingly common basis for a reasonable cause argument. TIGTA reports have shown that identity theft impacts roughly 1 in 15 taxpayers, and it can completely derail your ability to file an accurate return. It’s a reminder that when you file back returns, it’s not just about getting compliant; it's a vital lifeline. With the IRS receiving 165,824,000 returns during a recent filing season, the system is clearly built to process a high volume, including late filings from people sorting out complex issues. You can read more about the tax season wrap-up and statistics on nstp.org.

To make your official request, you'll typically file Form 843, Claim for Refund and Request for Abatement. You need to attach a clear, concise letter explaining your situation, supported by third-party documents like hospital records, police reports, or insurance claims. Our attorneys often handle these negotiations directly with the IRS, which can significantly boost the chances of getting penalties wiped from your account. You can explore a deeper dive into this process in our article on using Form 843 for penalty abatement. Successfully removing thousands of dollars in penalties can make resolving your entire tax debt far more achievable.

Finding the Right Solution for Your Tax Debt

Okay, you’ve filed your back tax returns. That initial wave of relief is real, but it’s often followed by a sobering question: how am I going to pay for this?

This is where you pivot from getting compliant to finding a resolution. The good news is that both the IRS and the Michigan Department of Treasury have programs designed to help people manage tax debt without destroying their financial lives. The key is figuring out which path makes the most sense for your specific situation.

Creating a Sustainable Payment Plan

For many people, the most direct route is an Installment Agreement. It’s exactly what it sounds like—a structured plan to make manageable monthly payments over time. This is often the simplest solution for taxpayers who just can't pay the full balance right away.

Setting one up shows the tax authorities you're acting in good faith. More importantly, it immediately stops aggressive collection actions like wage garnishments or bank levies.

I recently worked with a small business owner in Lansing who, after filing several years of returns, found herself owing just over $25,000. Writing a check for that amount was out of the question, but her business had steady cash flow. We helped her establish a Direct Debit Installment Agreement. Not only did this give her a predictable monthly payment, but it also lowered the setup fees. What felt like an insurmountable mountain of debt became a manageable line item in her budget.

The most important part? Proposing a payment you can actually afford every single month. Defaulting on an agreement will undo all your progress and put you right back in the collections crosshairs.

When a Fresh Start Is Needed

But what if the debt is so large that even a monthly payment plan isn't realistic? In those situations, we start looking at an Offer in Compromise (OIC).

An OIC is a formal agreement with the IRS to settle your tax liability for less than the full amount you owe. It’s not just a simple negotiation, though. It’s an intensive process where you have to prove, with detailed financial records, that you lack the income and assets to ever pay the full debt.

The success of an OIC comes down to a specific IRS formula called "Reasonable Collection Potential" (RCP). This calculation looks at your income, essential living expenses, and the equity in your assets to determine what the IRS believes it could realistically collect from you. A successful offer requires meticulous documentation.

The IRS accepted over 25,000 OICs in a recent year, but it's important to remember that many more were rejected. Usually, rejections happen because of incomplete applications or because the IRS determines the taxpayer can afford to pay more than they offered. Understanding the fine print of this program is critical, which is why we put together a detailed guide on what an Offer in Compromise truly is. Having a professional guide you through the process can dramatically increase the chances of getting an OIC approved.

Relief for Spouses Unfairly Burdened with Tax Debt

When you file a joint tax return, you create joint liability. That means the IRS can come after either spouse for the entire tax bill, no matter who earned the income or made the mistake. This can be devastating if one spouse was hiding income or making fraudulent claims without the other’s knowledge.

This is exactly why Innocent Spouse Relief exists. It’s a lifeline.

By filing Form 8857, Request for Innocent Spouse Relief, you can formally ask the IRS to release you from responsibility for your spouse's (or ex-spouse's) tax issues. It’s a complicated process, but the relief it provides can be life-changing. While it's tough to get exact numbers for Michigan, we know that nationwide, relief is granted in about 40% of claims where a spouse can prove they were truly unaware of the tax discrepancy. This just goes to show how vital a well-prepared and well-argued case is.

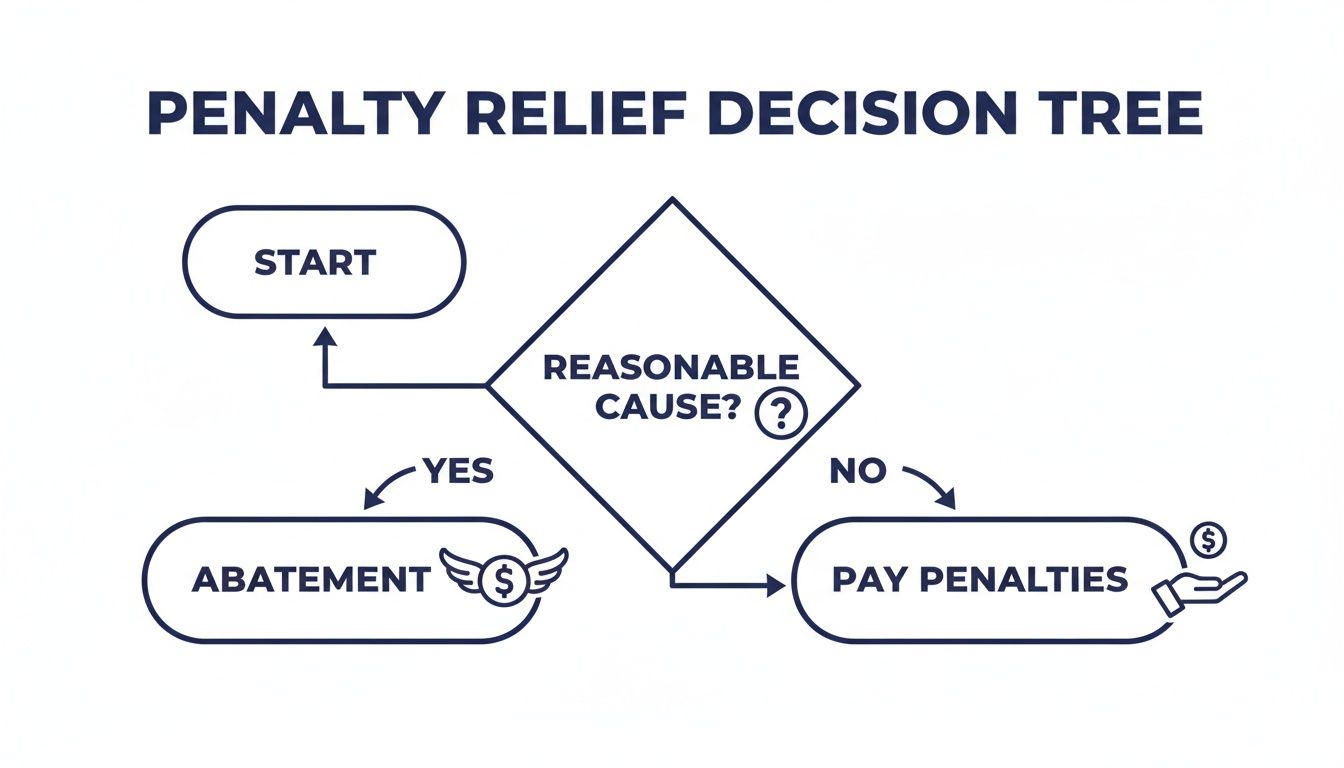

This decision tree gives you a good idea of the thought process behind seeking penalty relief, which is often a key step before negotiating a final payment solution.

As the flowchart shows, being able to establish "reasonable cause" is the critical fork in the road. Getting that right can lead directly to penalty abatement, potentially saving you thousands of dollars.

Navigating these options—from payment plans to OICs and innocent spouse claims—requires a clear strategy. Each path has its own strict eligibility rules and documentation standards. This is where an experienced tax professional can analyze your unique financial landscape and fight for the solution that best protects your assets and gives you a clear path back to solid ground.

Answering Your Top Questions About Filing Back Taxes

Even with a solid plan, catching up on old tax returns can feel like navigating a minefield. You're bound to have questions. This is where we'll tackle the most common concerns we hear from Michigan taxpayers trying to get right with the IRS and the state.

From crucial deadlines to the nightmare of identity theft, let's clear up the confusion so you can move forward.

How Far Back Do I Really Need to Go?

This is the big one, the question almost everyone asks first. While the IRS technically has an unlimited amount of time to come after you for unfiled returns, their own internal policy usually limits their focus to the last six years. Getting those six years filed is typically enough to be considered "compliant" in their eyes and halt any escalating collection efforts.

But—and this is a big but—it's not a universal rule. Certain situations demand a deeper dive:

- Significant Past Income: If you had years with very high earnings, the IRS will likely want to see those returns, even if they're more than six years old.

- Business Tax Complications: Unfiled business returns, especially those involving payroll taxes, are a major red flag for the IRS and often require more extensive filing.

- Applying for Loans: Trying to get a mortgage or a small business loan? Lenders have their own requirements and may insist on seeing specific tax returns that fall outside that six-year window.

The best strategy is to start by gathering what you need for the last six years. Then, it's wise to have a tax professional take a look at your specific circumstances to confirm that's all you need to do.

What Happens if I Just Keep Ignoring It?

Doing nothing is the single most expensive mistake you can make. Eventually, the IRS's automated system will take matters into its own hands and file what's called a Substitute for Return (SFR) for you. They create this return using only the income information they've received from third parties—like W-2s from your old jobs or 1099s from clients.

An SFR is the absolute worst-case scenario. The IRS calculates your tax bill based on gross income alone, without giving you a single credit or deduction you’re entitled to. We've seen this inflate a person's actual tax liability by 40-50% or even more.

The pain doesn't stop there. Once an SFR is on the books, it paves the way for aggressive collection actions. This means wage garnishments, levies on your bank accounts, and federal tax liens slapped on your property. The only way to stop the bleeding and correct the record is to file your own, accurate tax return.

Is It Too Late to Claim a Refund from an Old Return?

Yes, there's a strict, non-negotiable deadline. You have exactly three years from the original due date of a tax return to file it and claim a refund. If you miss that window, the money is gone for good—it's forfeited to the U.S. Treasury.

Let that sink in. If you had money withheld from your paychecks back in 2020 but never filed a return, you have until the 2024 filing deadline to claim it. After that, it's gone. Billions of dollars in refunds go unclaimed every year simply because people don't file in time.

What if I Was a Victim of Identity Theft?

Tax-related identity theft can throw a wrench into everything, making it impossible to file electronically and creating a massive headache. If a fraudster has already filed a return using your Social Security number, you have to act fast.

Michigan residents are part of a nationwide problem that saw over 500,000 federal cases in a recent year. The first step is to file IRS Form 14039, Identity Theft Affidavit. This officially puts the IRS on notice and kicks off the process of cleaning up your account.

This is critical because unfiled returns often lead to an automated SFR from the IRS, which assesses taxes without any of your deductions and robs you of valuable credits. Think about the Earned Income Tax Credit (EITC), which recently returned $56 billion to 25 million families. You can see more about recent filing season statistics and trends on IRS.gov.

The experienced attorneys at Defense Tax Partners can take this burden off your shoulders. We handle the entire process, working directly with the IRS's Identity Theft Protection Specialized Unit to untangle the mess and restore your proper filing status.