What is a Tax Levy? A Clear Guide to Understanding and Stopping It

Receiving an official notice from the IRS or the Michigan Department of Treasury can be unsettling, especially when it includes the words "tax levy." It’s a term that carries a lot of weight, and for good reason. A tax levy is the government’s legal seizure of your property to settle a tax debt.

Let's put it this way: a tax lien is a claim the government places on your property, signaling to other creditors that they have a right to it. A tax levy, on the other hand, is the government actually taking your property.

Answering the Core Question: What Is a Tax Levy?

A tax levy is one of the most serious enforcement actions the IRS or a state tax agency can take. It doesn't happen out of the blue. It’s the final, powerful step after all other attempts to collect an unpaid tax bill—like letters and official notices—have gone unanswered. This isn't a warning; it's the government actively seizing your assets to cover what you owe.

The idea is simple: if taxes are due and you don't pay or make arrangements to settle the debt, the government has the legal authority to take what you own. A tax levy is that formal, legal seizure. This powerful collection tool has deep roots in U.S. history, evolving significantly since the Civil War era to become the system we know today.

Key Characteristics of a Tax Levy

Knowing what defines a levy is the first step in figuring out how to deal with one. It's an aggressive collection method with a few key features that set it apart from other tax collection efforts.

- It’s an Action, Not Just a Claim: A tax lien is a legal claim filed against your property, securing the government's interest. A levy is the actual seizure of that property.

- It Targets Specific Assets: The government can levy a wide range of assets, including your bank accounts, wages, personal property like cars, and even your home.

- It Follows a Strict Legal Process: A levy can't just happen overnight. The law requires the IRS to send several notices first, culminating in a Final Notice of Intent to Levy, before any seizure can occur.

To better grasp the legal framework that gives tax authorities these enforcement powers, it's helpful to look at some of the landmark income tax cases that have shaped tax law over the years. This context can shed light on why these agencies have such significant collection capabilities.

A levy is the government’s ultimate collection tool. Its purpose isn’t just to secure the debt—it’s to actively collect it by taking ownership of your property and turning it into cash.

To break it down even further, here's a quick reference table that summarizes the most important aspects of a tax levy.

A Quick Guide to Understanding a Tax Levy

| Attribute | Description |

|---|---|

| What It Is | The legal seizure of property to satisfy a tax debt. |

| Who Issues It | Federal (IRS) or state (Michigan Department of Treasury) tax agencies. |

| What Can Be Seized | Bank accounts, wages, Social Security, vehicles, real estate, and more. |

| Prerequisites | Tax assessment, demand for payment, and a Final Notice of Intent to Levy. |

This table provides a snapshot of what a levy entails, from who can issue it to the types of assets that are at risk.

The Path from Unpaid Tax to Seized Assets

One of the biggest misconceptions about tax levies is that they happen out of the blue. They don't. A levy is actually the final, predictable step in a long process of ignored warnings from the IRS or the Michigan Department of Treasury. Understanding this timeline is your best defense because it reveals several chances to step in and fix the problem before your assets are on the line.

The process kicks off the moment a tax bill is officially calculated (assessed) and you don't pay it. The first piece of mail you'll get is a formal Assessment of Tax Due and a Demand for Payment. For federal taxes, this is usually an IRS Notice CP14, which spells out exactly what you owe and when it's due.

If you don't respond to that first notice, the letters will keep coming. Each one gets a little more serious, reminding you about the debt and what could happen if you continue to ignore it.

The Critical Final Notice

Pay close attention to this next part. The most important letter you will receive is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This is the government's last-ditch warning before they start taking action. The IRS typically sends this as Letter 1058 or LT11, and it's a legally required step before they can seize anything.

When this letter lands in your mailbox, a crucial countdown begins.

You have exactly 30 days from the date on the letter to either pay the debt or work out another solution. This 30-day window is your last, best opportunity to stop the levy in its tracks.

Ignoring this notice is the worst thing you can do. During these 30 days, you have a legal right to request what's called a Collection Due Process (CDP) hearing. Requesting this hearing immediately puts a temporary freeze on the levy process, giving you the breathing room to negotiate. This is the time to be decisive.

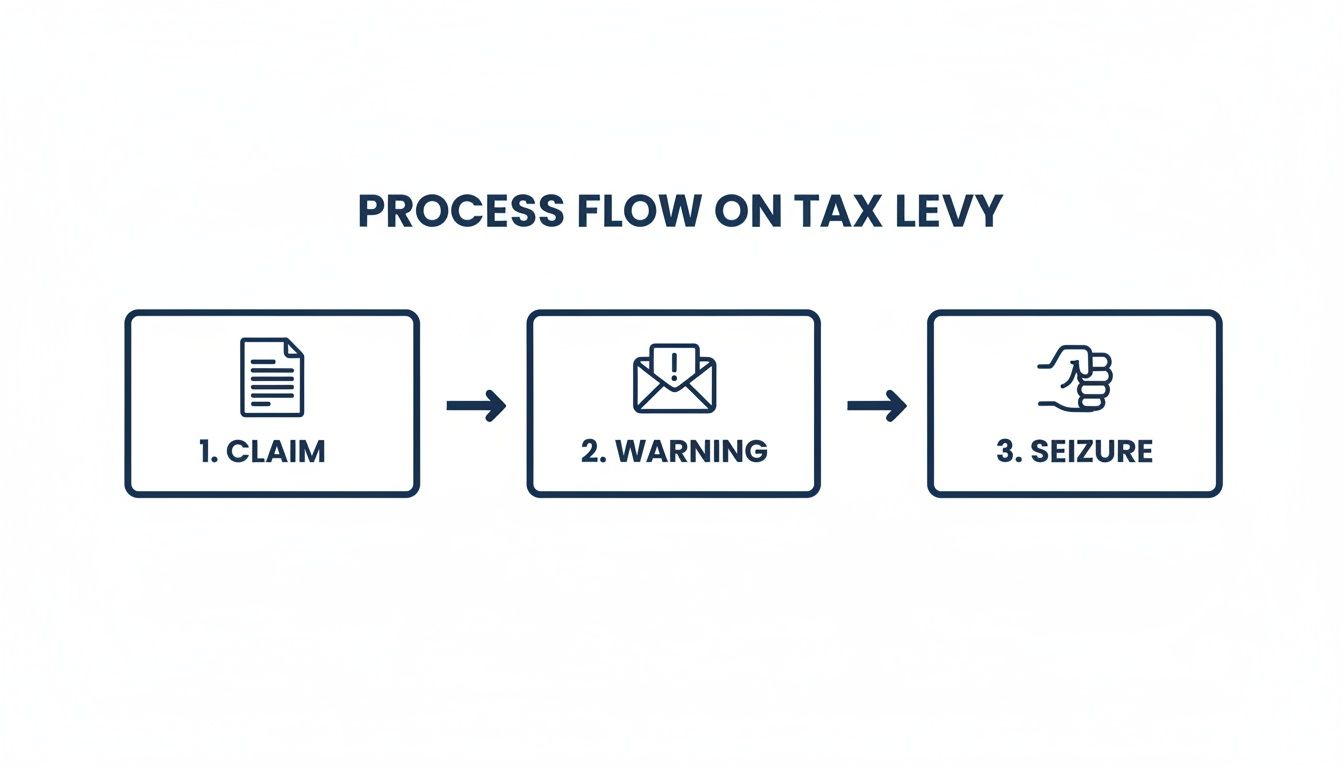

This simple chart breaks down the journey from the initial tax claim to the final seizure.

As you can see, a levy doesn't just happen. It’s the result of a process with clear warning signs, giving you a chance to respond before it's too late.

How Different Types of Levies Work

If that 30-day period passes with no resolution, the tax agency gets the green light to start seizing your assets. The type of levy they use will determine how it impacts you. It's worth noting that aggressive tax collection isn't new; it has often ramped up during times of national need. For instance, federal tax levies became much more common after World War II, a time when top marginal tax rates soared to 94% to fund Cold War initiatives. You can read more about the history of U.S. taxation on Wikipedia.

Today, levies generally fall into a few common categories:

- Bank Levy: Think of this as a one-time grab. The IRS instructs your bank to freeze funds in your account, up to the amount you owe, for 21 days. This gives you a small window to try and resolve the debt. If you don't, the bank sends the money to the IRS on day 22. While the levy is over at that point, the IRS can always issue another one later.

- Wage Levy (Garnishment): This is a continuous seizure that can be financially devastating. The IRS contacts your employer and orders them to take a portion of your wages from every single paycheck and send it directly to the government. This doesn't stop until the debt is paid, the levy is released, or the debt legally expires.

- Property Seizure: In the most serious cases, the IRS can seize physical assets like your car, a boat, or even your house. They then sell the property at auction and apply the money to your tax bill.

Knowing these steps is power. It demystifies the process and shows that a levy is almost always an avoidable outcome. By paying attention to the notices and acting within that critical 30-day window, Michigan taxpayers can stop the process cold and find a manageable way forward before their financial world is turned upside down.

Understanding The Key Differences: Tax Levy vs. Tax Lien

When you're dealing with the IRS or the Michigan Department of Treasury, a few terms get thrown around that can cause instant panic: tax levy, tax lien, and wage garnishment. They all sound bad, and they are, but they aren't the same thing. Knowing exactly what each one means is the first critical step in building a defense and getting your financial life back on track.

Think of it like this: a tax lien is a warning shot, while a tax levy is the direct hit. A lien is the government essentially placing a public "dibs" on your property. It doesn't take anything from you right away, but it clouds the title, craters your credit, and secures the government's place in line to get paid.

A levy is the government acting on that claim. It's the actual, forceful seizure of your assets to pay off the debt. They're no longer just calling "dibs"—they're walking away with your property.

Defining The Core Purpose Of Each Action

The real difference between a lien and a levy comes down to their function. One is a passive claim, and the other is an active collection tool.

A tax lien is a legal claim the government files against your property when you owe back taxes. It’s a public notice that says you have an outstanding tax debt, and its sole purpose is to secure that debt. This makes the government a secured creditor, meaning they get paid before almost anyone else if you try to sell the property. You can learn more about the specific steps you can take by checking out our guide on how to remove tax liens in Michigan.

On the other hand, a tax levy is an enforcement action. Its purpose isn't just to stake a claim; it's to actively collect the money you owe by taking your property. The government isn't just noting its interest anymore—it's forcefully taking your assets to satisfy the debt.

A tax lien is a public notice that says, "You owe us money." A tax levy is the action that says, "We are now taking your money."

So where does a wage garnishment fit in? A wage garnishment is just a specific, and particularly painful, type of levy. It’s a continuous levy, meaning your employer is legally ordered to send a chunk of every single paycheck to the tax agency until the debt is paid off.

Comparing The Impact On Your Financial Life

Each of these actions hits your financial stability, property rights, and overall life differently. A lien is a slow-burning problem that creates a long-term obstacle. A levy is an immediate, full-blown crisis.

To make this crystal clear, let's break down how these enforcement tools really compare in the real world. This table visually contrasts the key differences between these three common tax enforcement actions.

Comparing Tax Enforcement Actions

| Feature | Tax Lien | Tax Levy | Wage Garnishment |

|---|---|---|---|

| Purpose | Secures the government's interest in your property. | Actively seizes your property to satisfy the tax debt. | A continuous levy that seizes a portion of your wages. |

| Effect on Assets | Prevents you from selling or refinancing property with a clear title. | Immediately removes funds from bank accounts or other assets. | Reduces your take-home pay with every paycheck. |

| Immediacy | A passive claim that sits on public record until the debt is resolved. | An urgent, one-time seizure (bank) or ongoing seizure (property). | An ongoing, immediate reduction of your income. |

| Credit Impact | No longer appears on consumer credit reports but is still a public record. | Does not directly appear on credit reports, but the underlying lien might. | Does not appear on credit reports, but financial strain is obvious. |

Understanding these distinctions is everything. If you're facing a lien, your goal is to resolve the debt before it ever escalates into a levy. If you've just received a levy notice, you're in an emergency. You need to act fast to protect what you have left.

Know Your Rights and Protections Against a Levy

That official notice of an impending tax levy can make you feel powerless, like you've been backed into a corner with no way out. But the law isn’t a one-way street. The government has put a robust set of protections in place to make sure you’re treated fairly, even when you owe back taxes. Grasping these rights is the first step toward regaining control and actively managing your financial future.

The IRS doesn’t have free rein; it operates under a framework called the Taxpayer Bill of Rights. Think of it less like a mission statement and more like a legally enforceable set of ten fundamental rights. When you're staring down a levy, three of these rights become your most powerful tools.

- The Right to Be Informed: You have a right to know exactly what's going on. The IRS is required to explain its actions, why it's taking them, and what all of your options are. No surprises.

- The Right to Challenge the IRS’s Position and Be Heard: If you think the IRS has it wrong, you have the right to a formal appeal and to get a response. This right is the very foundation of the Collection Due Process (CDP) hearing.

- The Right to Retain Representation: You can hire an authorized professional, like a tax attorney, to speak for you. Once you’ve formally done that, the IRS generally has to communicate with your representative, not you.

Understanding Exempt Assets and Income

One of the biggest fears people have is that the IRS will take everything. It's a common misconception, but it's not true. Federal law actually protects certain types of property and a portion of your income from a tax levy. This is a critical shield designed to prevent a tax debt from turning into a complete financial disaster.

This idea isn't new. The concept of shielding taxpayers from government overreach has deep roots in American history. Property tax levies have been part of U.S. policy for over 160 years, and states started putting limits on them as far back as 1852 to protect their citizens. You can dig deeper into these historical tax levy limits and their impact to see how this has evolved.

The federal government carries this principle forward today.

The IRS cannot leave you with nothing. Specific exemptions are in place to ensure you and your family can still cover basic needs like food, shelter, clothing, and transportation.

What the IRS Cannot Take

While most assets are fair game for a levy, federal law draws a clear line around several categories. Knowing what's protected can bring immediate peace of mind and help you form a clear-headed strategy.

Here are some of the most common exemptions:

- A portion of your wages, salary, or other income. The exempt amount is based on your filing status and the number of dependents you claim.

- Certain unemployment and workers' compensation benefits.

- Specific public assistance payments, such as Supplemental Security Income (SSI).

- Undelivered mail.

- Your main home, though this is a complex area. Seizing a primary residence is rare and requires a court order, making professional guidance essential.

Knowing these rights and exemptions is your first line of defense. If you believe your financial hardship is severe enough to halt collection actions entirely, it's worth seeing if you qualify for IRS Currently Not Collectible status. By understanding these protections, you and a tax professional can work together to enforce your rights and shield the assets you absolutely need to run your household.

Proven Strategies to Stop or Remove a Tax Levy

When that levy notice shows up, your first reaction might be panic. It feels final, like the end of the line. But here’s what I tell my clients: a levy isn’t the end of the story. It’s actually the beginning of a conversation, and you have more power in that conversation than you think.

Both the IRS and the Michigan Department of Treasury have well-established programs to help people resolve their tax debts without having their lives turned upside down. This isn't about finding some secret loophole; it's about knowing the official pathways available and choosing the one that fits your situation. Tax agencies would much rather get voluntary, predictable payments than go through the hassle of seizing your property.

Let's walk through the most effective strategies to get a levy stopped in its tracks.

Set Up an Installment Agreement

The most direct way to halt a levy is to get on a formal payment plan. An Installment Agreement is a contract with the IRS or the State of Michigan that lets you pay off your tax debt in manageable monthly chunks. As soon as this agreement is approved, all levy actions have to stop, provided you keep up with your payments.

This is a great fit for anyone who can realistically pay the full debt but just needs more time. For many common tax situations, both the IRS and Michigan have streamlined applications that make this a quick and powerful solution.

Settle Your Debt with an Offer in Compromise

But what if you look at the total amount you owe and know there's simply no way you can ever pay it all back? That’s where an Offer in Compromise (OIC) comes in. This is a formal program that allows certain taxpayers to settle their tax liability for less than the full amount owed.

Think of it this way: the IRS would rather get something than nothing. To get an OIC approved, you have to open up your books and prove that your income and assets are not enough to cover the entire debt.

The IRS will analyze several factors:

- Your realistic ability to pay from your current assets and income.

- Your potential for future earnings.

- Your reasonable and necessary living expenses.

- Whether there's a genuine doubt you even owe the tax (Doubt as to Liability).

- Whether forcing you to pay the full amount would cause an extreme economic hardship or would simply be unfair (Effective Tax Administration).

The good news is that the moment you submit an OIC application, most collection activities—including levies—are put on hold while the IRS reviews your case. You can learn more about this powerful tool by reading our guide on what an Offer in Compromise is and how it works. Because the application is so detailed, getting professional help can make all the difference.

Request a Levy Release Due to Hardship

If a levy is already hitting your bank account or paycheck and you can’t pay for basic needs, you can demand a levy release. This doesn't make the debt disappear, but it forces the tax agency to back off immediately, giving you critical breathing room to work out a more permanent solution.

A levy release is granted when you can prove to the tax agency that the levy is preventing you from meeting basic, reasonable living expenses for yourself or your family.

You'll need to provide financial proof showing that the levy is making it impossible to pay for essentials like your rent, groceries, or critical medical bills. In Michigan, presenting a clear case of hardship can compel the Department of Treasury to release the levy and discuss other options, like a payment plan you can actually afford.

Explore Innocent Spouse Relief

Tax problems often come from joint tax returns. If a tax debt was created because your spouse (or ex-spouse) messed up the return without you knowing about it, you shouldn't have to pay for their mistake. Innocent Spouse Relief is designed to protect you from being held responsible for tax, interest, and penalties caused by someone else's actions.

To qualify, you generally have to show three things:

- You filed a joint return that has a tax deficiency.

- You can prove that when you signed the return, you had no idea—and no reason to know—about the error.

- Looking at all the facts, it would be fundamentally unfair to hold you liable for the debt.

This is a specific, and very powerful, form of relief for people caught in a tough situation.

Argue for Penalty Abatement

Finally, take a close look at your tax bill. A huge chunk of it might be penalties for filing late, paying late, or other compliance issues. If you had a good reason for the mistake, you might be able to get those penalties wiped away through Penalty Abatement.

"Reasonable cause" isn't just any old excuse. It has to be a legitimate, often unavoidable, event that kept you from doing what you were supposed to do. Think of things like a sudden serious illness, a death in your immediate family, or your business records being destroyed in a flood. Proving it takes good documentation, but if you're successful, it can drastically lower your total debt and make the whole problem much easier to solve.

How a Tax Professional Can Resolve Your Levy

Going up against the IRS or the Michigan Department of Treasury on your own is a daunting prospect. When you're facing a tax levy, it can feel like you're completely outmatched. Hiring an experienced tax professional isn't just about getting advice; it's about bringing in a seasoned advocate who knows the system inside and out. They speak the language of revenue officers and can step in immediately to protect you.

The very first thing we do is get in touch with the agent assigned to your case. This simple act often puts a temporary stop to the most aggressive collection efforts. By filing a Power of Attorney, we legally require the tax agency to communicate directly with our firm, effectively ending the stressful, demanding calls to you.

Building a Strategy That Fits Your Life

Once we've put a hold on collections, we dive deep into your specific financial situation. There’s no cookie-cutter solution for a tax levy. We carefully analyze your income, assets, and liabilities to figure out the best way to move forward. This isn't a shot in the dark; it's a precise strategy built on years of navigating the complexities of federal and Michigan tax law.

We’ll figure out which resolution programs you qualify for and walk you through the real-world pros and cons of each option:

- Installment Agreement: If you have the ability to pay the debt over time, we can negotiate a manageable payment plan that won't cripple your budget.

- Offer in Compromise (OIC): For those under serious financial duress, we can prepare a detailed OIC to persuade the agency to settle your tax debt for a lower amount.

- Currently Not Collectible (CNC): We can demonstrate that the levy is creating an immediate economic hardship, which can compel the agency to release it and pause collections.

Handling the Legal Heavy Lifting

Resolving a tax levy often involves more than just negotiation. The path to a solution might require formal appeals or other legal challenges. Knowing how to file court documents correctly and hitting every non-negotiable deadline is crucial, and that’s a burden we take off your shoulders.

Hiring a tax professional immediately levels the playing field. It signals to the IRS or state that you are taking the matter seriously and are prepared to assert your rights and explore all available legal remedies.

Our in-depth understanding of both IRS regulations and Michigan’s unique enforcement playbook gives our clients a clear advantage. We're always thinking one step ahead, building a proactive defense to shield your assets, get the levy released, and find a final resolution you can live with.

Common Questions We Hear About Tax Levies

Even after you grasp the basics, it's natural to have specific questions when a tax levy hits close to home. Here are some straightforward answers to the questions we hear most often from taxpayers in Michigan, shedding light on what these actions mean in the real world.

How Long Does a Bank Levy Last?

This is a big point of confusion, so let's clear it up: an IRS bank levy is a snapshot in time, not a continuous freeze.

The moment your bank gets the levy notice, they are legally required to hold the funds in your account at that specific time, up to the amount of your tax debt. They must hold that money for 21 days. Think of this as your final, critical window to negotiate with the IRS and get the levy released.

If you don't resolve the debt within that period, the bank sends the money to the IRS on the 22nd day. The levy is then over. To get any new money you deposit, the IRS would have to start the entire process over and issue a completely new levy. This is very different from a wage levy, which is continuous and takes a piece of every single paycheck until the debt is paid.

Can the IRS Take My Social Security?

Yes, they can. Through a program called the Federal Payment Levy Program (FPLP), the IRS has the power to take a portion of your Social Security benefits directly. They don't even need a court order to do it.

Under the FPLP, they can garnish up to 15% of your monthly payment to cover your back taxes.

It's critical to know, however, that some federal benefits are protected. For example, Supplemental Security Income (SSI) is generally off-limits and cannot be seized by the IRS.

Will a Tax Levy Show Up on My Credit Report?

A tax levy itself won't appear on your credit report. What used to show up was the Notice of Federal Tax Lien, which is the public notice that often precedes a levy. However, back in 2018, the three major credit bureaus stopped including federal tax liens on consumer credit reports.

While this change is good news for your credit score, don't get a false sense of security. Lenders can still easily find tax liens through public record searches, which could absolutely affect your ability to get a mortgage or a business loan. The real damage from a levy isn't to your credit score—it's the immediate, devastating blow to your cash flow and access to your own money.