What Is a Bank Levy? How It Works and How to Protect Your Money

When you get a notice about a bank levy, it’s understandable to feel a jolt of panic. A bank levy is a serious legal action where a tax authority, like the IRS or the Michigan Department of Treasury, takes funds directly from your bank account to satisfy an unpaid tax debt.

It’s one of the most aggressive collection tools in their arsenal, and it can freeze your access to your money almost instantly, causing immediate and significant financial hardship.

The Anatomy of a Bank Levy

So, what exactly happens behind the scenes? Understanding what is a bank levy is the first step to figuring out how to fight it.

Think of it this way: after sending multiple notices that go unanswered, the government essentially gets a court-ordered key to your bank account. But it’s not a continuous drain. A bank levy is a one-time snapshot—a freeze-frame of your account balance.

The levy captures only the funds available in your account at the very moment the bank processes the notice. Any deposits made the next day, or even a few hours later, are safe from that specific levy. The catch? If the seized amount doesn’t clear your entire tax bill, the agency can—and almost certainly will—issue another levy down the road.

How a Bank Levy Immediately Affects You

The impact is instant and disruptive. The moment your bank receives the levy notice, they are legally obligated to freeze your funds.

- No Withdrawals: You can't pull cash from an ATM or get money from a teller.

- Failed Transactions: Your debit card will be declined, and scheduled auto-payments for bills like your mortgage or car payment will fail.

- Bounced Checks: Any checks you’ve already written will bounce, which can trigger additional fees from the people you owe.

This freeze isn't permanent, but it is immediate. The bank is required to hold the funds for a 21-day period (for an IRS levy) before they send the money to the government. That 21-day window is your last, best chance to intervene.

A bank levy is a powerful collection tool used by the IRS to recover unpaid federal taxes. When the IRS serves a notice of levy, the bank must surrender funds up to the amount specified, but only after a legally mandated holding period. You can explore the IRS procedures to get more details on how this collection process works.

To give you a clearer picture, let's break down the essential details in a simple table.

Bank Levy Key Facts at a Glance

This table breaks down the most critical aspects of a bank levy for quick and easy understanding.

| Aspect | What It Means for You |

|---|---|

| What It Is | A one-time legal seizure of funds from your bank account. |

| Who Issues It | Federal (IRS) or state (Michigan Department of Treasury) tax agencies. |

| Trigger | Unpaid tax debt after multiple notices have been ignored. |

| Immediate Effect | Your bank account is frozen, blocking all access to your money. |

| Holding Period | The bank holds your funds for 21 days (for an IRS levy) before remitting them. |

| What's at Stake | All funds in the account at the time of the levy, up to the debt amount. |

| Key Takeaway | The 21-day window is your critical opportunity to stop the seizure. |

Understanding these key facts is crucial. A bank levy is a specific type of action, different from a lien (a claim against your property) or a wage garnishment (a continuous seizure of your paycheck). Knowing precisely what you're up against is the only way to choose the right strategy to resolve it.

The Legal Steps Leading to a Bank Levy

Let's get one thing straight: a bank levy doesn't just happen out of the blue. It’s the final play in a long, drawn-out collection game, and the government has to follow a strict set of rules to get there. Both the IRS and the Michigan Department of Treasury are legally required to send you a series of notices, giving you multiple chances to address the problem before they can touch your money.

Think of these official letters as legally required warning shots. Before any action is taken, the government must formally determine you owe tax, send you a bill (what’s known as a Notice and Demand for Payment), and give you an opportunity to settle up. If you don't respond, the collection efforts will escalate, leading to one final, critical warning.

When dealing with the IRS, this last-chance document is called the Final Notice of Intent to Levy and Notice of Your Right to a Hearing. Once you receive this, a clock starts ticking. You have exactly 30 days to either pay what you owe or officially appeal the levy before the IRS can legally order your bank to freeze your accounts.

The Critical Timeline from Notice to Seizure

Once the government has cleared all the legal hurdles and your 30-day window closes, they don't call you—they call your bank. The levy notice goes directly to your financial institution, and from that moment, things move very fast. Your bank is legally required to comply and freeze your funds immediately.

The process unfolds in three distinct stages once the levy hits your bank.

The moment the freeze happens, another countdown begins. With an IRS levy, there’s a federally mandated holding period: your bank must hold the frozen funds for exactly 21 days.

This 21-day period is your absolute last chance to act. The money is still in your account—it hasn't been sent to the government yet. This is the window where you or your tax attorney can frantically negotiate with the IRS to get the levy released. If you don't succeed in that timeframe, it's over. On the 22nd day, the bank wires the money to the Treasury, and it’s gone.

Understanding this sequence is vital. The notices you receive are not junk mail; they are legal prerequisites that start a countdown timer. Recognizing the Final Notice of Intent to Levy allows you to intervene before the process even reaches your bank.

To recap, the path to a bank levy looks like this:

- Tax Assessment and Billing: You get the first bill for taxes owed.

- Multiple Collection Notices: A series of follow-up letters arrive, demanding payment.

- Final Notice of Intent to Levy: This is the big one—the official, final warning that gives you a 30-day response window.

- Levy Issued to Bank: After the 30 days are up, the agency sends the order to your bank.

- 21-Day Holding Period: Your bank freezes the funds but must wait 21 days before sending them.

- Funds Seized: If you haven’t resolved the issue, the bank sends your money to the government.

Knowing exactly where you are in this timeline is the key to stopping the process and protecting what’s yours.

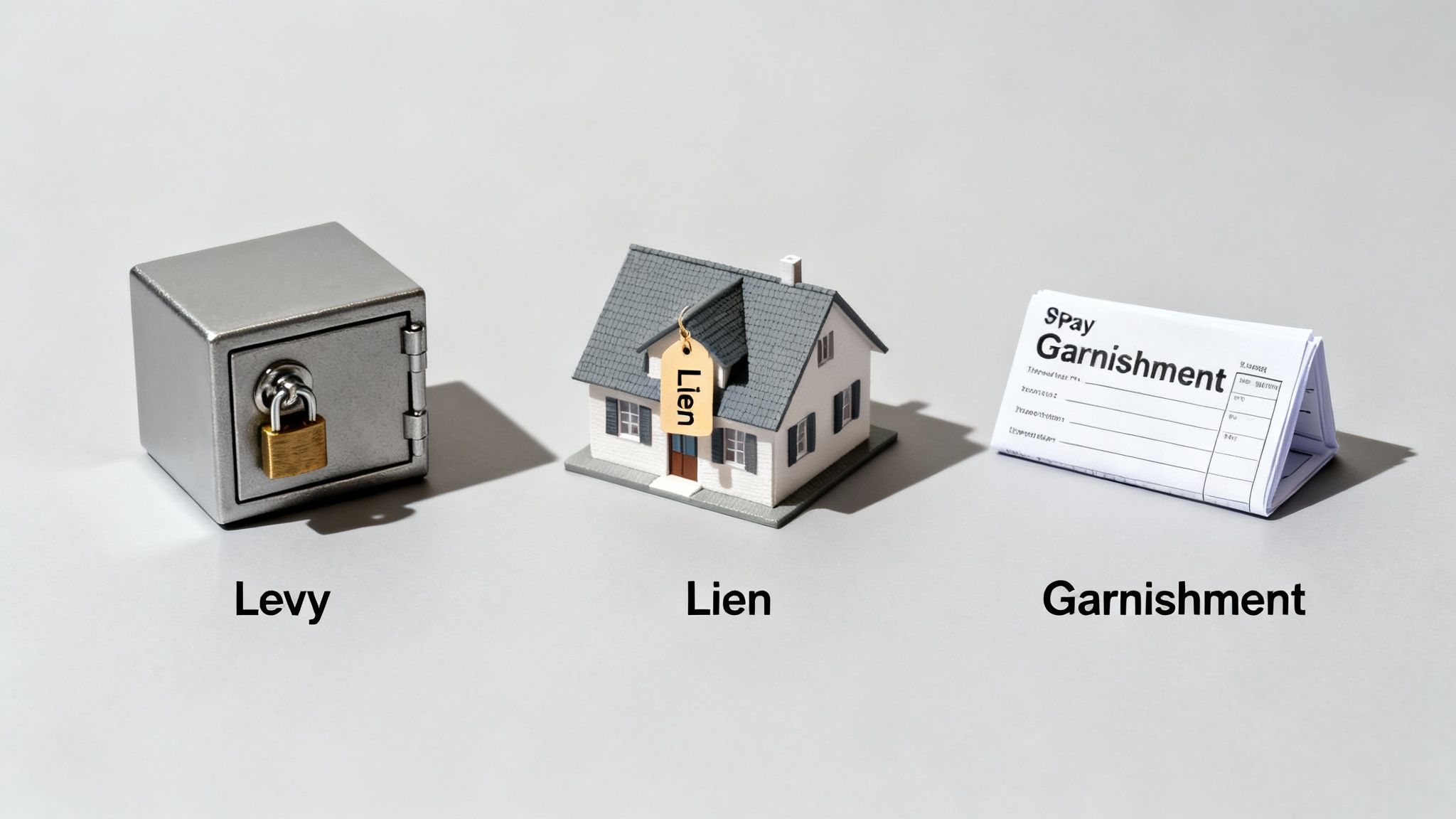

Understanding a Levy, Lien, and Garnishment

When you’re grappling with tax debt, you’ll likely hear the terms levy, lien, and garnishment thrown around. People often use them interchangeably, but that’s a big mistake. They are three very different collection tools, and knowing which one you’re facing is critical to fighting back effectively.

Think of a bank levy as the government’s most direct move. It’s an immediate, one-time seizure of whatever cash is in your bank account at that exact moment. They aren't just putting a hold on your money; they are actively taking it to cover your debt.

Differentiating Liens and Garnishments

So, how does that differ from the other two? A tax lien isn't a seizure at all. Instead, it’s a public legal claim against your property—your home, your car, your business assets. It’s the government’s way of saying, "We have first dibs on this property if you try to sell it." This cloud on your title can crush your credit score and make it impossible to sell or refinance until the tax bill is settled. To get a deeper dive into these claims, it helps to understand how tax liens work.

Then there’s a wage garnishment, which goes after your future income. This is a continuous legal order sent straight to your employer, forcing them to take a cut of your paycheck before it ever hits your bank account. Unlike a levy, which is a single snapshot in time, a garnishment keeps happening, paycheck after paycheck, until the debt is paid in full.

The core difference lies in what is being targeted. A levy takes what you have now. A lien secures a claim on your property. A garnishment intercepts what you will earn in the future.

Levy vs Lien vs Garnishment Key Distinctions

To make it crystal clear, let's break down how these three collection actions stack up against each other. This quick comparison should help you pinpoint exactly what you’re dealing with.

| Collection Action | What It Targets | Duration | Primary Purpose |

|---|---|---|---|

| Bank Levy | Current Assets (e.g., funds in a bank account) | One-Time Event | To seize existing money immediately. |

| Tax Lien | Property (e.g., house, car, business assets) | Long-Term | To secure the government's claim and priority as a creditor. |

| Wage Garnishment | Future Earnings (i.e., your paycheck) | Continuous | To intercept a portion of your ongoing income. |

Knowing which tool the government is using is the first step toward finding the right solution. If your bank account is suddenly frozen, you’re up against a levy and have a very short 21-day holding period to act. If you’re blocked from selling your home, a lien is the culprit. And if your take-home pay has mysteriously shrunk, a garnishment is almost certainly the reason. Each problem demands a completely different strategy.

Your Immediate Options to Stop or Release a Bank Levy

When your bank account is suddenly frozen by a levy, it’s easy to feel powerless. But here’s something most people don't realize: you have more control than you think. Because the IRS is legally required to hold the funds for 21 days, the money is still technically in your account. This is your critical window to act.

The clock is ticking, so you need to move fast. Your first call should be directly to the revenue officer assigned to your case, whether at the IRS or the Michigan Department of Treasury. How you handle this first conversation matters—staying calm and professional can set the stage for a successful negotiation.

Proving Financial Hardship for a Levy Release

One of the most powerful arguments you can make is for an administrative release based on significant economic hardship. This isn't just about being inconvenienced; you need to show that the levy is preventing you from covering your basic, essential living expenses. We’re talking about rent, groceries, or urgent medical care.

To make your case, you have to be ready with proof. Start gathering these documents immediately:

- Bank Statements: To show your current financial reality.

- Pay Stubs: To verify your income.

- Household Bills: Rent/mortgage statements, utility bills, and car payments.

- Medical Invoices: Proof of any critical medical needs.

Presenting this evidence clearly demonstrates that the levy is causing genuine distress. Tax agencies aren't in the business of making people homeless; their goal is to collect the debt. When you can prove hardship, they have procedures in place to release the funds.

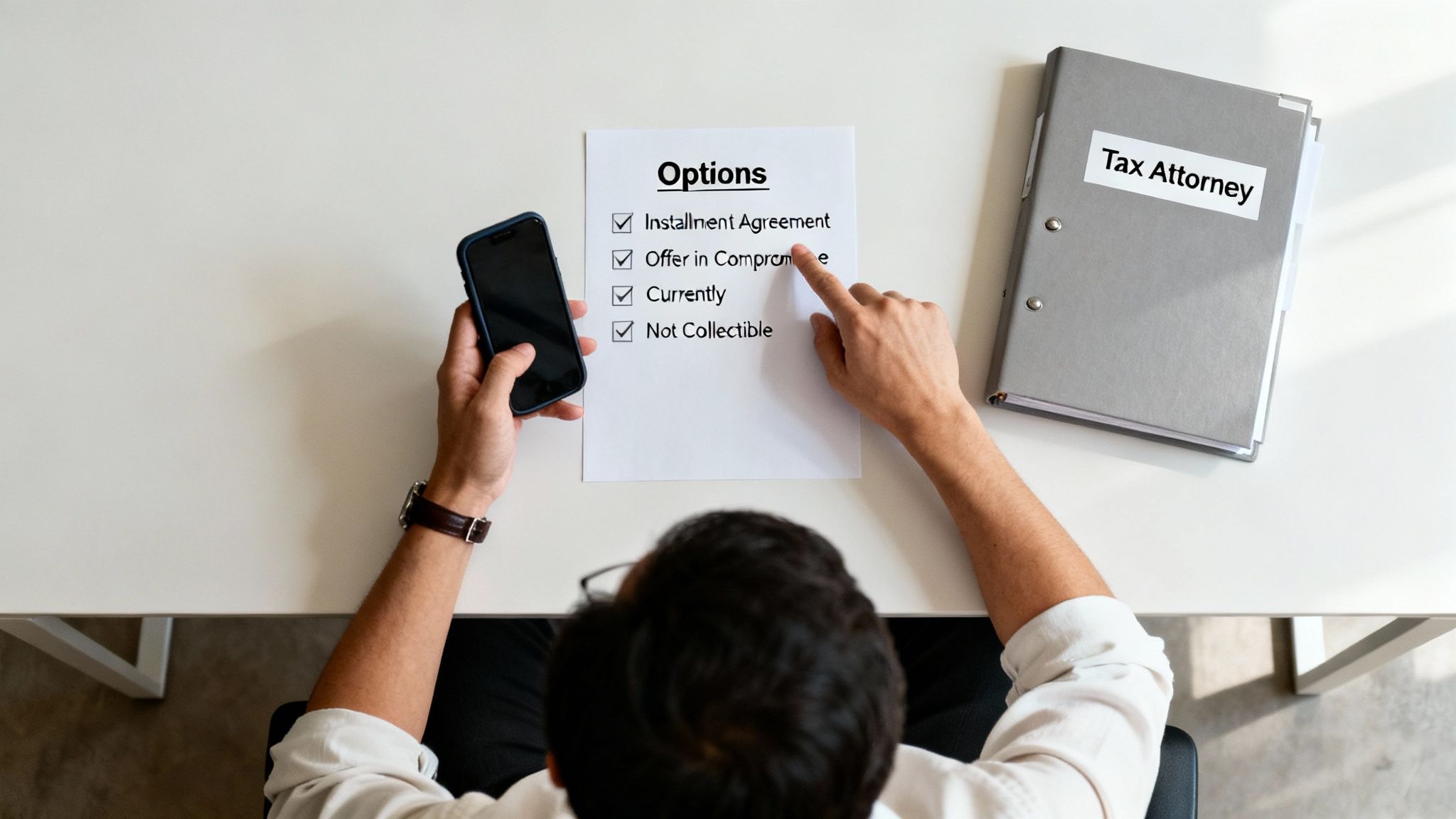

Entering a Collection Alternative to Stop the Levy

Getting a release due to hardship is a great first step, but it's a temporary fix. To stop another levy from hitting you down the road, you need a long-term plan. This is where agreeing to a formal collection alternative comes in—it’s often the quickest way to get the current levy released for good.

By proposing one of these solutions, you're showing the tax agency you’re serious about settling your debt. Your primary options include:

- Installment Agreement (IA): Think of this as a structured payment plan. You agree to pay a set amount each month, and in return, the government typically halts aggressive collection actions like levies.

- Offer in Compromise (OIC): If you truly can't afford to pay the full amount you owe, an OIC lets you settle the debt for less. We dive deeper into this in our guide on what an Offer in Compromise is.

- Currently Not Collectible (CNC) Status: For those in a dire financial spot, CNC status temporarily pauses all collection activity. It’s an acknowledgment that you can't afford to pay anything right now, though the debt doesn’t go away.

Remember, the goal is to communicate and cooperate. Ignoring the problem guarantees the worst outcome. By proactively engaging with the tax authority and presenting a viable resolution plan, you can often secure a levy release and establish a manageable path forward.

Sometimes a bank levy follows a court action, so it’s crucial to understand your rights and know how to fight a default judgment. Another powerful tool is filing for bankruptcy, which triggers an "automatic stay." This legal protection immediately halts all collection actions—including levies—giving you the breathing room needed to reorganize your finances under court supervision.

How a Tax Attorney Can Help Michigan Residents

When you get a notice that the IRS or the Michigan Department of Treasury is levying your bank account, it's easy to feel cornered. But you absolutely do not have to go through this alone. While the basic strategies for fighting a levy are similar everywhere, having a local Michigan tax attorney in your corner is a game-changer.

Why? Because tax law isn't just federal. It has specific state-level quirks, and a seasoned local professional knows the ins and outs of the Michigan Department of Treasury—the people, the processes, and the unwritten rules.

At Defense Tax Partners, we live and breathe Michigan tax law. We're dialed into the local enforcement trends and what the typical timelines look like. This means we know exactly who to call to cut through the bureaucracy and get things moving. That local know-how can be the one thing that gets your levy released within that critical 21-day holding period before the bank sends your money away for good.

Taking Immediate and Strategic Action

From the moment you call us, our sole focus is on taking practical, immediate steps to protect what's yours. We don't just talk; we act.

Here’s how we tackle a bank levy:

- Immediate Contact: The first thing we do is file a Power of Attorney. This tells the tax agency they have to talk to us, not you. We then get on the phone with the revenue officer on your case to put a stop to any further collection actions.

- Negotiating a Release: We immediately start building a strong case to get the levy released, often arguing for a financial hardship exemption to free up the cash you need to live.

- Building a Long-Term Solution: Once the immediate fire is out, we work with you to find a permanent solution. This could be an Installment Agreement you can actually afford or an Offer in Compromise to settle the debt for less, ensuring you don't face another levy down the road.

A tax attorney acts as your official representative and shield, handling all communications with the tax agency. This not only alleviates immense stress but also prevents you from accidentally saying something that could jeopardize your case.

Our team has a proven track record of helping people all over Michigan navigate these complex tax problems. We know your situation is unique, and we'll craft a strategy that fits your specific circumstances. If your account is frozen, every single second counts. You can't afford to wait for that 21-day window to slam shut.

Contact Defense Tax Partners today for a free, confidential consultation. Let us take a look at your case, lay out your options in plain English, and build a plan to protect your finances and put this tax debt behind you for good.

For more insights on securing your property, check out our guide on how to remove tax liens in Michigan.

Your Top Questions About Bank Levies Answered

When you get a notice about a bank levy, your mind starts racing with questions. It's a stressful situation, and you need clear, straightforward answers fast. Here’s a breakdown of what our clients most often ask when they’re facing a levy in Michigan.

Can they take money from my joint account?

Unfortunately, yes. If your name is on a joint bank account—even if the money was deposited by your spouse, partner, or parent—the tax authorities can usually seize the full amount to cover your tax debt.

From a legal standpoint, they see your name on the account and assume you have a right to all of it. The other account owner is left with the uphill battle of proving which funds were theirs, a process that is both complicated and rarely successful.

Is any of my money safe from a bank levy?

Some funds do have legal protection, but it’s very specific. The IRS, for instance, cannot touch federally-funded benefit payments that are directly deposited into your account.

This protection typically covers:

- Social Security benefits

- Supplemental Security Income (SSI)

- Veterans' benefits

- Certain disability payments

Your bank is actually required to look back at your account history and automatically shield a portion of these funds from seizure. The problem is, if you’ve mixed these protected funds with other money, things get messy fast. That's why it's so important to assert your rights immediately to protect what you're entitled to.

How long will the bank levy last?

Think of a bank levy as a snapshot, not a movie. It’s a one-time event that captures whatever funds are in your account at the exact moment the bank processes the order.

A levy freezes what's there on that day. It won't touch the paycheck you deposit tomorrow or the money you transfer in next week.

But don’t get a false sense of security. If that first levy doesn't clear your entire tax bill, the IRS or the Michigan Department of Treasury can, and often will, hit you with another one down the road. It's a cycle that will continue until the debt is fully resolved.