What happens if you get audited: A concise guide to audit notices and outcomes

So, that official-looking envelope from the IRS or the Michigan Department of Treasury has landed in your mailbox. Your stomach might drop, but an audit notice isn't an automatic accusation of guilt. It’s simply a formal request to double-check the numbers you reported.

Think of it this way: what happens if you get audited? It kicks off with that notice, moves into a phase where they ask for specific information, and ends with a resolution. That resolution could be a simple no change, an agreed-upon adjustment to what you owe, or a disputed finding that you'll need to address further.

The Audit Notice Arrived: What Happens Now?

The second you see that letter, it's natural to feel a jolt of panic. But the absolute first thing you must do is take a breath and approach this calmly and methodically. An audit notice just means your tax return was flagged for a closer look. It's a process, not a verdict.

I often tell my clients to think of it like a routine traffic stop. The notice is the flashing lights in your rearview mirror—it definitely gets your attention, but it doesn't automatically mean you’ve done anything seriously wrong. When the auditor asks for documents, it’s like the officer asking for your license and registration. How organized, calm, and timely you are from this point forward can make all the difference.

Your Immediate Action Plan

How you handle these first few moments can set the tone for the entire audit. A proactive, well-thought-out response is absolutely critical to steering this toward a positive outcome. It’s tempting to either shove the letter in a drawer or immediately call the number on the notice, but both are mistakes.

Instead, this initial phase is all about understanding exactly what the government is asking for and getting your ducks in a row. The notice itself is your roadmap—it will tell you the specific tax year and the exact items they want to verify.

Key takeaway: An audit is a verification process, not an accusation. The IRS and state agencies select returns for all sorts of reasons, including random computer-generated flags. Your only job is to provide clear, organized proof for the numbers on your return.

Key First Steps: Do This, Not That

Before you make a single move, it's crucial to know which actions will help you and which could dig you into a deeper hole. Firing from the hip is a recipe for disaster. For instance, calling an auditor unprepared might lead you to say something that accidentally opens up other tax years or new areas for them to scrutinize.

To help you navigate these first critical hours, here is a simple checklist of what to do—and what to avoid.

Your Initial Audit Response Checklist

| Action Item | Do | Don't |

|---|---|---|

| Review the Notice | Read every word carefully. Identify the tax year, specific items being audited, and the response deadline. | Skim it and assume you know what they want. The details are critical. |

| Respond to Deadlines | Acknowledge and respect every deadline. If you need more time, have your representative request an extension. | Ignore the letter or miss a deadline. This can lead to an automatic decision against you. |

| Gather Your Records | Methodically collect all receipts, bank statements, and records related to the items under review. Organization is key. | Send a messy shoebox of receipts or disorganized files. Present your information clearly. |

| Communicate with the IRS | Let a qualified tax professional, like an attorney, handle all communications. They know what to say and what not to say. | Call the auditor yourself without a plan. An innocent comment can be misinterpreted. |

| Seek Professional Help | Contact a tax defense attorney immediately. They act as a shield between you and the auditor. | Try to handle it alone to save money. This can be a very costly mistake in the long run. |

Following these simple rules from the outset helps ensure you stay in control of the process. Your initial actions lay the foundation for a successful defense.

Decoding the Different Types of Tax Audits

When you hear the word "audit," it’s easy to picture an IRS agent in a suit knocking on your door. But that’s actually the rarest and most intense scenario. In reality, a tax audit can be anything from a simple letter in the mail to a full-blown examination of your finances.

Think of it like a medical check-up. A minor issue might just need a quick phone call with a nurse. A more complex concern could require a visit to the doctor's office for a few tests. For serious conditions, you might see a specialist for a comprehensive investigation. Tax audits follow a similar spectrum, and knowing which kind you’re dealing with is the first step toward a successful outcome.

The Correspondence Audit: A Letter in the Mail

This is by far the most common and least threatening type of audit. A correspondence audit happens entirely through the mail. You’ll get a formal notice from the IRS or the Michigan Department of Treasury flagging one or two specific items on your tax return and asking for more information.

For example, the letter might ask you to send proof of the charitable donations you claimed or receipts for childcare expenses tied to a tax credit. It’s a targeted request for verification. In most cases, you mail back the documents they asked for, and if everything checks out, they close the file. It might seem simple, but don't take it lightly—ignoring the notice or sending the wrong information can turn a small problem into a big one.

The Office Audit: A Visit to an IRS Location

One step up the ladder is the office audit. This one is more involved because, as the name implies, you have to show up in person at a local IRS office. An auditor will sit down with you to review several related parts of your tax return.

An office audit is common for self-employed individuals, where the IRS might want to look at your reported income, business expenses, and equipment depreciation all at once. You’ll be asked to bring a whole file of records with you—bank statements, receipts, mileage logs, you name it. They want to see the proof right then and there.

This is where professional representation really starts to pay off. A tax attorney can go to this meeting for you, handle the auditor's questions, and make sure you don't inadvertently say something that opens up a whole new can of worms.

The Field Audit: They Come to You

The field audit is the most comprehensive and serious type of examination. This is the scenario everyone dreads, where an IRS revenue agent schedules a visit to your business, home, or your representative's office to conduct a deep dive into your books.

Field audits are generally reserved for more complex situations, like a business with multiple employees, a high-income individual with sophisticated investments, or a return with major red flags. The agent will pour over everything from your daily sales receipts to your inventory control systems. The scope is wide, the questions are tough, and the stakes are incredibly high. Trying to handle a field audit on your own is a major gamble.

The financial fallout from any audit can be life-altering. In a recent fiscal year, the IRS wrapped up over 500,000 tax audits and recommended an additional $29 billion in taxes. That breaks down to an average of $57,400 in extra tax per audit—a potentially crippling amount for any family or small business. You can dive deeper into these figures by reviewing the latest IRS enforcement statistics.

Knowing which audit you’re up against is critical. It sets the tone for your response and helps you prepare for what’s ahead. A simple letter requires a different strategy than a full field examination, but every single notice from the IRS demands your immediate and careful attention.

Navigating the Audit Process from Start to Finish

Getting a notice that you’re being audited can feel overwhelming, like you’re being asked to navigate a maze blindfolded. But the process isn’t as chaotic as it seems. It’s actually a very structured, step-by-step procedure. Think of it less as a sudden attack and more like a formal review—every stage gives you a chance to present clear, organized evidence that validates your tax return.

The whole journey, from that first letter in the mail to the final determination, is a methodical conversation between you and the tax agency. Your job is to provide exactly what they need, organized and on time. Knowing the sequence of events is the first step to taking back control.

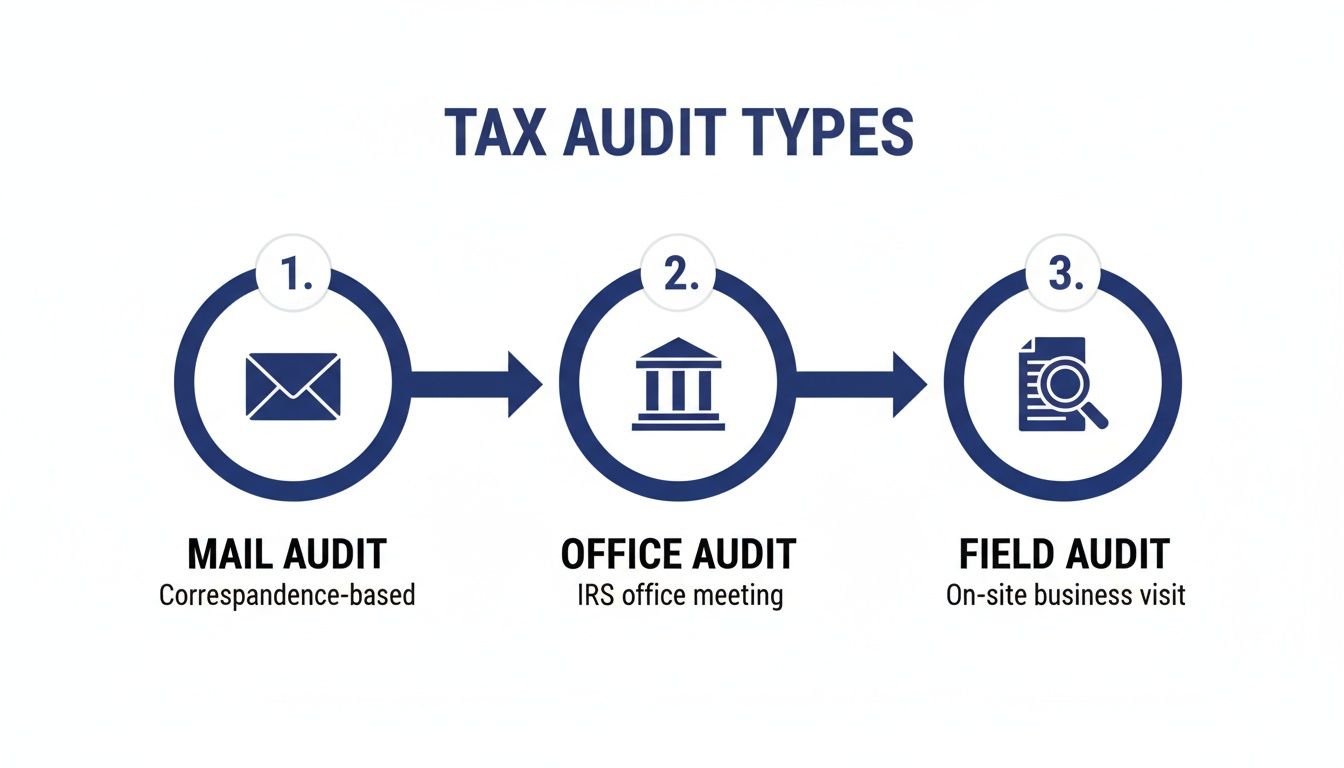

This visual gives you a quick breakdown of the different audit types, from simple mail inquiries to in-depth, in-person examinations.

As you can see, the deeper they dig, the more involved the process becomes.

Stage 1: The Initial Notification and Response

It all starts with a letter. You'll receive an official notice from the IRS or the Michigan Department of Treasury informing you that one of your tax returns has been selected for examination. This notice will clearly state the tax year in question and which parts of the return they want to look at.

Your first move shouldn't be to pick up the phone and call the auditor. It’s to call a tax professional. Review the notice together and map out a strategy. This makes sure your first response is calm, calculated, and doesn't accidentally hand over information you aren't required to provide.

Stage 2: The Information Document Request

Soon after, you’ll receive an Information Document Request (IDR). This is basically the auditor's shopping list—a formal, itemized list of the specific records they need. It could be anything from bank statements and expense receipts to mileage logs or proof of charitable giving.

This is where you gather your evidence. Organization is everything. You should only provide the exact documents requested for the specific period under audit. Anything more is a mistake. Dumping a shoebox full of disorganized receipts on their desk is one of the worst things you can do.

Your response to the IDR sets the tone for the entire audit. A clean, well-organized package shows you're professional and transparent. A messy or incomplete submission just raises red flags and invites the auditor to dig deeper.

Stage 3: The Auditor's Review

Once your documents are submitted, the auditor begins their work. They will go through every piece of paper, line by line, comparing your records to the numbers you reported on your tax return. It's not uncommon for them to have follow-up questions or ask for clarification on certain items during this stage.

Ideally, all communication should go through your tax representative. This creates a professional buffer and prevents you from making an off-the-cuff comment that could be misinterpreted or unintentionally expand the scope of the audit.

Stage 4: Preliminary Findings and Your Rebuttal

When the review is done, the auditor will issue their preliminary findings. If they’ve found discrepancies, they will propose changes to your tax liability. This is not the final word—it's an opening bid.

This is your opportunity to respond. You can either agree with the findings or present counter-arguments backed by additional evidence to dispute them. For anyone facing a proposed adjustment, knowing how to dispute a tax assessment is the crucial next step.

Stage 5: The Final Determination Letter

The last step is the issuance of a determination letter, which officially closes the audit. This letter will lay out one of three possible outcomes:

- No Change: Your return is accepted as you filed it. This is the best-case scenario.

- Agreed: You accept the proposed changes. You'll soon receive a bill for the additional tax, penalties, and interest owed.

- Disagreed: You don’t accept the findings. This moves you out of the audit and into the appeals process.

The entire timeline can vary wildly. A simple correspondence audit might be wrapped up in a few months, while a complex field audit can easily stretch out for more than a year. Throughout it all, patience and strategic preparation are your two most powerful tools.

Understanding Potential Outcomes and Penalties

After months of gathering documents, answering questions, and waiting, the audit finally wraps up. This is the moment of truth—the point where you find out exactly what this whole process means for your finances. Understanding what happens if you get audited isn't just about the back-and-forth; it’s about knowing the possible endgames and preparing for the financial impact.

When the dust settles, an audit typically lands in one of three places. Each outcome sends you down a different path, from a sigh of relief to a new set of challenges.

The Three Main Audit Outcomes

That final determination letter from the IRS or the Michigan Department of Treasury will spell out their conclusion in black and white.

- No Change: This is the best-case scenario. The auditor has gone through your records and agrees that your tax return was accurate as filed. The case is closed, and you don’t owe any additional tax, penalties, or interest. You can breathe easy.

- Agreed: Here, the auditor has found issues and proposed changes to your tax return, and you agree with their findings. This almost always means you owe more tax. You’ll sign an agreement form, and the agency will follow up with a bill for the new tax amount, plus any penalties and interest that apply.

- Disagreed: If you don't accept the auditor's conclusions, the fight isn't over. This outcome moves your case into a new phase where you have the right to formally contest the decision, usually by taking your case to an independent appeals office within the tax agency.

For most people facing an "Agreed" or "Disagreed" outcome, the biggest worry isn't just the extra tax. It's the penalties and interest that can make a manageable tax bill feel completely overwhelming.

How Penalties Can Magnify Your Tax Bill

When an audit uncovers an understatement of tax, the government doesn't just ask for the difference—they tack on penalties as a punishment. These aren't just random fees; they're calculated based on the nature and severity of the mistake.

- Accuracy-Related Penalty: This is the most common one we see. If the IRS decides you were negligent or simply disregarded the rules (even if it was an honest mistake), they can add a penalty of 20% of the understated tax.

- Civil Fraud Penalty: This is the big one, reserved for cases where the IRS believes you intentionally tried to deceive them. The civil fraud penalty is a staggering 75% of the understated tax.

And on top of all that, interest starts piling up on the unpaid tax from the day your return was originally due. Because it compounds, interest can dramatically inflate your total debt over time.

Example: Let's say an audit finds you underreported your income, creating a $10,000 tax deficiency. A 20% accuracy-related penalty immediately adds $2,000. Then, after a year of accrued interest (at a rate of, say, 8%), another $800 gets tacked on. Your initial $10,000 problem has quickly snowballed into a $12,800 bill.

Penalties Are Often Negotiable

Here’s some good news: penalties are not always set in stone. A critical part of any good tax defense strategy is negotiating for penalty abatement. If you can show you had "reasonable cause"—basically, that you made a good-faith effort to follow the law but were prevented by circumstances beyond your control—the IRS may agree to reduce or even completely waive the penalties.

You can learn more about how our firm handles these requests by reading our guide on filing a Form 843 for penalty abatement.

While human-led audit rates have changed over the years, the IRS's automated systems are incredibly good at flagging discrepancies. These programs assessed a whopping $7.7 billion in a recent year from 1.2 million underreporter cases alone. Ignoring one of those automated notices is a fast track to a formal deficiency notice with accuracy penalties tacked on, which often triggers a similar inquiry from Michigan tax authorities.

Successfully arguing for reasonable cause requires a compelling, legally sound explanation. When the stakes are this high, having professional representation is absolutely vital.

What Are Your Defense and Relief Options?

When an audit ends and you’re handed a report you disagree with, it’s easy to feel like you’ve hit a dead end. But this isn’t the end of the road. In fact, it’s the beginning of your real defense. An unfavorable audit report is simply the first move in a longer conversation, opening the door for you to formally challenge the findings and look into programs designed to give you a lifeline.

It’s so important to understand what happens if you get audited and the results aren't in your favor. You have legal rights to contest the decision and fight for a fair resolution. This is where the dynamic shifts—you move from simply reacting to an auditor's conclusions to proactively building your case.

Taking Your Case to the Appeals Office

If you flat-out disagree with the auditor's findings, your first and most powerful move is to request a conference with the IRS Independent Office of Appeals. Don't think of this as just a re-do of the audit. It's a chance to present your side of the story to a completely separate and impartial division within the IRS.

An Appeals Officer has a different job than an auditor. While an auditor’s role is to stick strictly to the letter of the law, an Appeals Officer has a bit more wiggle room. Their main goal is to settle tax disputes without dragging everyone into court. This means they can weigh the "hazards of litigation"—the very real possibility that the IRS could lose if the case went to trial.

Because of this, they have the authority to negotiate and land on a settlement that might be much better than what the auditor initially proposed.

Why Appeals Matters: Think of the appeals process as a form of mediation. It brings a fresh pair of eyes to your case and opens up opportunities for compromise that just aren't on the table during the audit itself. A strong, well-argued appeal can often lead to a lower tax bill and even waived penalties.

Getting Penalties Wiped Out With an Abatement Request

Sometimes you agree you owe more tax, but the penalties tacked on are what's truly crushing you financially. The good news is, you can formally ask to have those penalties removed through a process known as penalty abatement.

The entire strategy hinges on proving you had "reasonable cause" for the error. This isn't a vague excuse; it's a solid, evidence-backed argument showing that you genuinely tried to follow the tax laws but were tripped up by circumstances you couldn't control.

Some of the more common arguments for reasonable cause include:

- Bad Advice from a Pro: You gave all your information to a tax professional who then made a mistake.

- Serious Illness: A major health issue, for you or a close family member, made it impossible to handle your tax obligations correctly.

- Records Destroyed: Your tax records were lost in a disaster like a fire or flood.

- Ignorance of the Law: This is a tough one to prove, but in very specific cases, you might argue that a particularly confusing or obscure tax rule was genuinely beyond your understanding.

Simply saying you were busy or just forgot won't cut it. You have to build a convincing case that your failure to comply was understandable given what you were up against.

Finding Shelter With Innocent Spouse Relief

When married couples file a joint tax return, the IRS sees them as a single unit. That means both spouses are on the hook for the entire tax bill, even if they get divorced later on. This is called "joint and several liability." But what if the tax debt was 100% your ex-spouse's fault?

This is exactly why Innocent Spouse Relief exists. This critical program can legally separate you from a joint tax liability that came from your spouse's (or former spouse's) mistakes. To qualify, you generally have to prove three key things:

- The tax was underreported because of your spouse's erroneous items.

- When you signed the return, you genuinely did not know—and had no reason to know—about the error.

- Given all the facts, it would be fundamentally unfair to hold you responsible for the tax.

The IRS is currently sharpening its focus on high-income taxpayers, with plans to increase audit rates for those earning over $10 million by more than 50% by tax year 2026. This heightened scrutiny makes relief programs like innocent spouse protection more vital than ever, especially when one partner's complex finances create a surprise tax liability for the other.

Navigating these defense and relief options is not a DIY project. Whether you're appealing a finding, fighting penalties, or seeking innocent spouse relief, professional help is key to building the strongest case possible. And if paying any remaining tax is simply out of the question, you might want to learn more about another powerful tool. You might be interested in our guide on what an Offer in Compromise is and how it can help you settle tax debt.

Your Top Tax Audit Questions, Answered

Even after getting a handle on the audit process, it's completely normal to have lingering questions and a bit of anxiety. Let's be honest, an audit isn't something most people go through, so it’s natural to worry about what set it off, how long it will take, and what the fallout might be.

This section tackles the most common questions we hear from clients every day. We'll give you straight, practical answers to cut through the noise and help you feel more prepared for what's ahead.

What Triggers an IRS Audit in the First Place?

While it’s true that a tiny fraction of audits are completely random, the vast majority are flagged by a powerful IRS computer system known as the Discriminant Information Function (DIF). This system is the gatekeeper. It scores every single tax return by comparing it against statistical norms for people in similar financial situations. If your return strays too far from the average, it gets a high DIF score, which is like raising a hand for a closer look from an IRS agent.

Think of it like a home security system. A single moth flying by a sensor might not do anything, but a combination of a window opening and a motion sensor tripping will definitely trigger an alarm.

Here are some common red flags that tend to grab the IRS's attention:

- Unusually high deductions: Claiming charitable gifts or business expenses that seem way out of proportion to your income is a big one. For instance, if you report $60,000 in income but claim $30,000 in business meals, you can bet the system is going to flag that.

- Recurring business losses: If a business reports significant losses year after year, the IRS might start to wonder if it’s a legitimate commercial operation or more of a hobby. This often triggers a review to verify its business intent.

- Income discrepancies: This is one of the easiest catches for the IRS. They get copies of all the W-2s and 1099s filed under your Social Security number. If the income you report doesn't match what employers and clients have reported paying you, an automated notice is almost guaranteed.

- Complex investments and foreign accounts: The more complex your financial life, the higher the odds of scrutiny. High-income taxpayers with pass-through income from partnerships, S-corporations, or foreign bank accounts are simply under a bigger microscope.

At the end of the day, if your financial story looks dramatically different from others in your income bracket, the IRS is more likely to ask you to explain why.

How Long Does a Tax Audit Usually Take?

This is one of the most unpredictable parts of the whole experience. The timeline for an audit really depends on its type and how complicated the issues are. There's no one-size-fits-all answer, but we can break it down into general estimates.

A straightforward correspondence audit, handled entirely through the mail, can sometimes be wrapped up in just a few months. This is especially true if the issue is simple and you respond right away with clear documentation. On the other hand, an office audit, which means a face-to-face meeting, usually takes longer—often somewhere between six months and a year.

The most involved type, a field audit, can easily stretch out for more than a year. These are deep dives into your finances, and things like the auditor's own caseload, the sheer volume of your records, and whether you decide to appeal the findings can all add significant time to the process.

It's a huge mistake to try and rush through an audit. A fast but bad outcome is far worse than a longer, more methodical process. Your number one priority should always be taking the time you need to gather every document and build the strongest possible case.

Can I Handle an IRS Audit Myself?

You absolutely have the legal right to represent yourself, but it's rarely a good idea for anything more than the simplest mail-based inquiry. IRS auditors are highly trained specialists who live and breathe the tax code. A taxpayer walking in without that same depth of knowledge is at an immediate, and serious, disadvantage.

Trying to go it alone can lead to some critical mistakes:

- Saying too much: You might accidentally answer a question in a way that opens up a whole new line of questioning or, even worse, expands the audit into other tax years.

- Making harmful statements: An innocent comment you think is helpful could easily be misinterpreted by an auditor as an admission of negligence.

- Not knowing your rights: Most people aren't aware of their right to appeal, ask for penalty abatement, or explore programs like Innocent Spouse Relief.

Hiring a qualified tax professional is like bringing in a shield. They handle all the communication, know exactly what to provide (and what not to), and negotiate from a position of strength and experience. That buffer is essential for protecting your rights and minimizing the financial damage.

Will I Go to Jail If I Get Audited?

This is probably the biggest fear people have when they hear the word "audit," but let me put your mind at ease: going to jail is an incredibly rare outcome. The vast majority of IRS audits are civil matters, not criminal ones. The entire point of a civil audit is to figure out the correct amount of tax owed. That's it.

Criminal investigations, the kind that can actually lead to prosecution and prison, are handled by a completely separate division of the IRS called Criminal Investigation (CI). They only get involved in cases of willful tax evasion or outright fraud. For an audit to cross that line from civil to criminal, the IRS has to find clear, compelling evidence that you deliberately tried to deceive them.

What does tax fraud look like?

- Keeping two separate sets of financial books.

- Intentionally hiding offshore bank accounts or sources of income.

- Creating fake invoices or documents to claim deductions you're not entitled to.

If you made an honest mistake, miscalculated a deduction, or just got tripped up by a confusing tax rule, the consequences will be financial. You might owe back taxes, interest, and penalties, but you won't be facing criminal charges. The key difference between a mistake and fraud is intent, and the bar for proving criminal intent is extremely high.