Notice of Levy IRS: How to Respond in Michigan (notice of levy irs)

Getting a letter from the IRS is always a bit nerve-wracking. But when you open the envelope and see a Notice of Levy, that feeling turns into a full-blown emergency. This isn't just another bill or a warning shot. It's a legal order that gives the IRS the power to seize your assets—your bank accounts, your paycheck, even your property—to cover an unpaid tax debt.

What an IRS Notice of Levy Really Means

Let's be clear: a Notice of Levy is one of the most serious documents the IRS can send. It means they've tried to contact you multiple times without success and are now using their most powerful collection tool. The IRS is legally authorized to take what you own to settle your account.

To really understand the gravity of the situation, it’s crucial to know the difference between a levy and its cousin, the tax lien. They sound similar, but their impact is vastly different.

Think of it this way: a tax lien is a public claim against your property. It's like the government putting a "boot" on your car. It secures their interest but doesn't take the car away. A Notice of Levy is the tow truck showing up to haul your car away. It's the active, physical seizure of your assets.

Lien vs. Levy: What You Need to Know

Many people use "lien" and "levy" interchangeably, but they are two distinct IRS actions. This table breaks down the fundamental differences.

| Action Type | What It Does | Impact on Your Assets |

|---|---|---|

| IRS Tax Lien | Secures the government's interest in your property as collateral for your tax debt. | Puts a public claim on your assets, harming your credit and making it hard to sell or borrow against property. The assets are still yours. |

| IRS Tax Levy | Is the actual act of seizing your property to satisfy the tax debt. | Actively takes your property. This can mean freezing and emptying bank accounts, garnishing wages, or seizing physical property. |

Understanding this distinction is the first step. A lien is a warning sign; a levy is the consequence in action.

What Is at Risk

The IRS's reach with a levy is incredibly broad. This isn't a theoretical threat—it’s a very real action that can turn your financial life upside down in an instant. Once a levy is issued, the IRS can go after almost anything you own.

Here are the assets most commonly targeted:

- Bank Accounts: The IRS can order your bank to freeze your account. The bank must hold your funds for 21 days before sending the money directly to the IRS. This can happen without any further warning.

- Wages and Salary: A wage garnishment is a particularly tough form of levy because it's continuous. Your employer is legally required to send a large chunk of your paycheck to the IRS, every single payday, until your debt is gone.

- Federal Payments: Any money coming to you from the federal government is fair game. This includes Social Security benefits, federal retirement payments, and payments for federal contracts.

- State Tax Refunds: If you're expecting a tax refund from the state of Michigan, the IRS can intercept it before it ever gets to you.

- Property: In more extreme cases, the IRS has the authority to seize and sell physical property. This can include your car, boat, or even your home.

It's critical to see the difference between a claim and an actual seizure. You can learn more about what a tax levy is and how it works to get a deeper understanding. A Notice of Levy is a clear signal that the time for waiting has run out. You need to take immediate, strategic action to protect what’s yours.

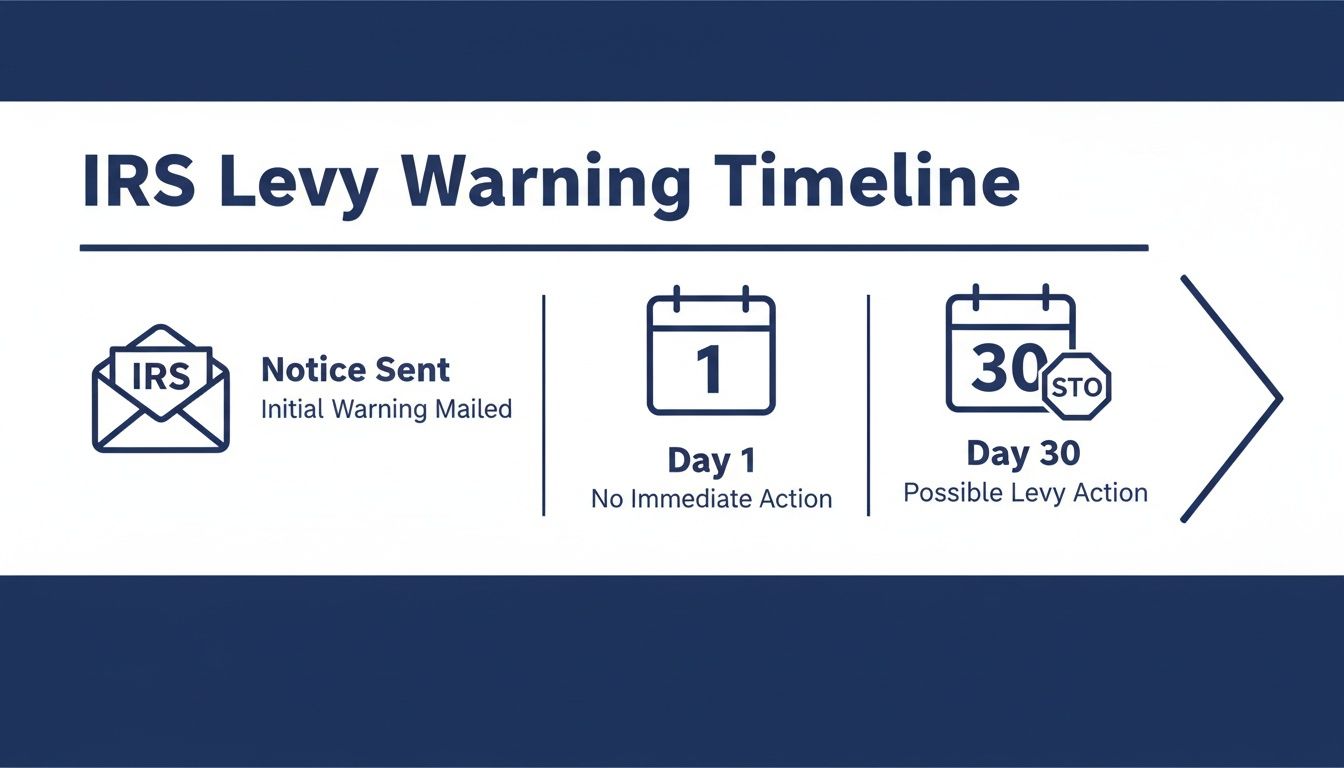

Your 30-Day Window to Stop a Seizure

The IRS can't just show up and take your property out of the blue. By law, they have to send you one final warning before they move to seize your assets. This isn't just another piece of mail; it's the most critical communication you'll receive and your best chance to stop a levy in its tracks.

This formal warning is a letter, usually titled a “Final Notice of Intent to Levy and Your Right to a Hearing.” The moment that letter arrives, a 30-day clock starts ticking. Think of it less as a suggestion and more as a hard legal deadline. What you do—or don't do—in those 30 days will determine what happens next.

This window is your opportunity to get ahead of the problem. It’s a legally required pause in their collection process, giving you one last chance to either pay the debt or formally challenge their plan to seize your assets. Letting this chance slip by is one of the worst mistakes you can make.

How to Spot the Final Notice

You've probably gotten other letters from the IRS, but this one is different. The "Final Notice" is the one that carries the immediate threat of seizure. It will clearly state the amount you owe, break down any penalties and interest, and explicitly warn you of the IRS's intent to levy your property.

Most importantly, this notice contains your ticket to a powerful protection: your Collection Due Process (CDP) hearing rights. By requesting a CDP hearing within that 30-day period, you can legally freeze most levy actions. The IRS has to hit pause while your case goes to their independent Office of Appeals, giving you vital breathing room to negotiate without the threat of a frozen bank account hanging over your head.

Think of this 30-day period as a strategic timeout. It's a legally mandated pause button that allows you to shift from being reactive to proactive, putting you back in a position of control.

Under Internal Revenue Code (IRC) Section 6331(d), the IRS must send this Final Notice at least 30 days before they act, usually via certified mail. The letter is a direct warning that your wages, bank accounts, and other assets are on the line. You can read more about the full scope of the IRS levy process on their official site.

What Happens When the 30 Days Are Up

If you ignore the notice and let the deadline pass, the gloves come off. The legal shield protecting you vanishes, and the IRS is free to start its collection machine without any further warning. The results can be financially devastating and happen almost overnight.

Here’s a snapshot of what to expect once that 30-day window slams shut:

- Bank Levies: The IRS will contact your bank directly and order them to freeze your accounts. After a 21-day holding period, the bank must send the funds—up to the amount you owe—straight to the IRS.

- Wage Garnishments: Your employer will get a notice to start withholding a large chunk of your paycheck. This isn't a one-time thing; it happens every single pay period until your tax debt is paid in full.

- Seizure of Other Assets: While it's not their first move, the IRS can also go after other assets. This includes intercepting state tax refunds, taking a portion of federal payments like Social Security, and in rare cases, seizing physical property.

This is a serious situation. The end of that 30-day period is when the IRS moves from sending letters to taking aggressive action. Your financial life can be turned upside down. The key is to see this notice not as a final threat, but as an urgent call to action. Use this window wisely, and you can prevent a seizure and find a path to resolving your tax problem for good.

How an IRS Levy Affects Your Income and Bank Accounts

Receiving an IRS notice is one thing, but the real punch comes when the levy actually starts. This isn't some abstract threat—it's a direct, forceful action against your financial lifeline. A levy means real money is about to be taken from your bank accounts and paychecks, often leaving you scrambling to cover basic living expenses.

The impact is immediate and can be absolutely devastating. Let's walk through exactly how this powerful collection tool targets your most critical assets, from the wages you earn to the cash sitting in your bank.

How a Wage Garnishment Works

One of the most common and disruptive levy types is a wage garnishment. When the IRS decides to go this route, they don't ask you for the money. Instead, they send a legal order, Form 668-W (Notice of Levy on Wages, Salary, and Other Income), directly to your employer. This isn't a suggestion; it's a command.

Your employer is then legally obligated to calculate a small, legally protected amount and send the rest of your pay directly to the IRS. This continues with every single paycheck until the entire tax debt is paid in full or you negotiate another solution. The amount the IRS leaves you is determined by your filing status and number of exemptions, and frankly, it's often not enough to live on.

The Shock of a Bank Account Levy

While a wage garnishment is a slow drain, a bank levy is a sudden, one-time blow. The IRS sends a notice to your financial institution, which must immediately freeze the funds in your account up to the total amount of your tax debt.

A bank levy is like a financial lightning strike. It captures whatever is in your account at that specific moment. If you owe $7,000 and have $5,000 in the bank, the entire $5,000 is frozen.

Your bank is required to hold these frozen funds for 21 days. This 21-day holding period is your last, critical window to contact the IRS and fight to get the levy released. If you don't resolve the matter in time, the bank sends the money straight to the IRS, and getting it back becomes incredibly difficult. You can learn more about the specifics of what a bank levy entails to better understand the process.

This timeline below shows the crucial 30-day window you have before a levy can even happen, highlighting your last chance to act.

This visual really drives home the urgency. Once that "Final Notice of Intent to Levy" arrives, the clock is ticking on that 30-day deadline before the IRS can start seizing your assets.

Levies on Federal Payments and Benefits

The IRS’s reach doesn’t stop with your employer and your bank. They can also intercept money the federal government owes you through a powerful system known as the Treasury Offset Program (TOP).

This program can target various federal payments, but a common one is Social Security benefits. Through what's often called a "continuous levy," the IRS can take up to 15% of your monthly benefit payment. This authority was granted under the 1997 Taxpayer Relief Act, allowing the IRS to siphon off a portion of federal payments until the debt is cleared.

This offset can also apply to other federal funds you might be expecting, including:

- Federal employee retirement annuities

- Payments to federal contractors

- Certain federal salaries

Understanding how a notice of levy from the IRS impacts each of these areas is the first step toward protecting yourself. The consequences are tangible and severe, making a swift and strategic response absolutely essential.

Your First Steps to Stop an IRS Levy

When an IRS levy notice lands in your mailbox, it's easy to feel a surge of panic. But right now, you need to take a deep breath and act decisively. The good news is that the path to stopping a levy isn't some hidden secret; it starts with immediate, strategic action, and the most powerful tool you have is right there in the "Final Notice of Intent to Levy" letter.

That letter details your right to request a Collection Due Process (CDP) hearing. Think of this as the emergency brake on the IRS collection machine. By formally requesting this hearing within the crucial 30-day window, you can automatically halt most new levy actions while your case gets a fresh look from the IRS Office of Appeals. This buys you invaluable time to find a real solution.

Requesting Your Collection Due Process Hearing

Filing a CDP hearing request is your absolute first line of defense. The official way to do this is by submitting IRS Form 12153, "Request for a Collection Due Process or Equivalent Hearing." I can't stress this enough: meeting that 30-day deadline is non-negotiable. If you miss it, you forfeit the automatic stay on collections, which puts you in a much weaker position.

Once your request is properly filed, the IRS has to stand down. This pause gives you the breathing room to figure out a long-term fix without the immediate fear of your bank account being seized or your wages garnished. It effectively shifts the power dynamic, letting you move from a purely defensive stance to a proactive one where you can negotiate from a place of relative stability.

With the immediate threat on hold, you can turn your attention to the three primary routes for resolving the underlying tax debt and getting the levy released for good.

Path 1: Set Up an Installment Agreement

For many people, the most direct path forward is an Installment Agreement (IA). This is simply a formal payment plan with the IRS. It allows you to pay off your tax debt in manageable monthly chunks over a period of up to 72 months. By setting up an IA, you're showing the IRS you're committed to making things right.

As long as you make your monthly payments on time and stay current on all future tax filings and payments, the IRS will not proceed with a levy. This is a great option if you can afford to pay the full debt eventually but just need more time to do it without upending your finances.

Path 2: Pursue an Offer in Compromise

But what if you look at the total amount you owe and know you can never realistically pay it all back? This is where an Offer in Compromise (OIC) comes into play. An OIC is a formal program that allows eligible taxpayers to settle their tax liability with the IRS for less than the full amount owed.

An Offer in Compromise isn't about haggling over the tax bill. It's a complex, data-driven process. You have to prove to the IRS, based on a deep dive into your income, assets, and reasonable living expenses, that they are unlikely to ever collect the full amount from you.

The IRS is notoriously selective and accepts only a fraction of the OIC applications it receives. It's a high bar to clear. But for those who do qualify, it can be a life-changing fresh start, wiping away an otherwise insurmountable debt.

Path 3: Qualify for Currently Not Collectible Status

For taxpayers in the toughest financial situations, there's another safety valve: being placed in Currently Not Collectible (CNC) status. This doesn't make the debt disappear, but it does put a temporary stop to all collection activities, including levies. The IRS essentially agrees to back off because taking your money would prevent you from covering basic living expenses.

To qualify for CNC, you'll need to open up your books and provide detailed financial information that proves your hardship. The IRS will periodically review your situation, and if your finances improve down the road, they can and will resume collection efforts. While CNC is a temporary solution, it provides immediate and critical relief when you simply have no other way out.

Getting the Levy Released and Finding a Permanent Fix

Stopping a levy is really just the first-aid part of the process. It gets the immediate bleeding to stop, but it doesn't solve the underlying problem. Your real goal is to get a formal levy release, which is the IRS’s official document terminating its legal claim on your property. This is the difference between hitting pause and actually stopping the collection action for good.

But the IRS won't just hand over a release. They need to see a clear plan in place for how you're going to handle the tax debt. They’re legally required to release a levy once the debt is paid, the time limit for collection runs out, or—most commonly—you've successfully set up an alternative payment solution.

What It Takes to Get a Formal Levy Release

The IRS operates on a strict set of rules, not on goodwill. The key to getting a levy released is to show them that, according to their own procedures, the collection action is either no longer necessary or is causing you an unacceptable level of harm.

Here are the most common situations that will trigger a levy release:

- Full Payment: The simplest way—you pay off the entire debt, including all the penalties and interest.

- Installment Agreement: You get a formal payment plan approved by the IRS and make your first required payment.

- Offer in Compromise Acceptance: The IRS agrees to your Offer in Compromise, and you start following its terms.

- Economic Hardship: You successfully prove the levy is preventing you from affording basic, necessary living expenses.

- An Error: The levy was a mistake. Maybe you already paid the tax, or they have the wrong person entirely.

How to Make the Formal Request

To make your case, especially for a hardship claim, you can't just tell the IRS you're struggling—you have to show them. This is done with a Collection Information Statement, usually Form 433-F. This form is a detailed breakdown of your finances: what you earn, what you own, and what it costs you to live.

A thoroughly prepared Collection Information Statement is your best leverage. It turns your claim of "I can't afford this" into a documented, verifiable fact. This gives the IRS revenue officer the proof they need to justify releasing the levy on their end.

You'll submit this form directly to the IRS agent or department handling your case. Be ready to back it up with documents like recent pay stubs, bank statements, and copies of essential bills. You’re painting a picture of your financial reality, and the details matter.

Beyond Payment Plans: Strategies to Reduce Your Debt

Sometimes, the sheer size of the tax bill is the real roadblock. In those cases, just getting into a payment plan isn't enough. You need to look at strategies that can actually reduce the total amount you owe. Two of the most powerful options are penalty abatement and Innocent Spouse Relief.

Penalty Abatement is a request to have certain tax penalties wiped from your account. You might qualify if you have a clean tax history (known as First-Time Abate) or if you can prove you had reasonable cause for not paying on time—think a sudden, severe illness or a natural disaster that completely upended your life.

Innocent Spouse Relief is designed to protect people from the tax debts created by their spouse (or ex-spouse) on a joint return. If you can show you had no knowledge of the errors and it would be fundamentally unfair to hold you responsible, the IRS may relieve you of the entire tax liability, along with the interest and penalties.

A crucial part of any long-term solution is ensuring you don't fall behind again. This means getting a handle on your ongoing tax obligations, like making quarterly estimated taxes if you're self-employed. Good tax planning is truly the best defense.

Ultimately, the strongest solutions often combine several of these strategies. For instance, you might get a penalty abatement that shrinks your debt to a manageable size, making an Installment Agreement affordable. For those with a truly overwhelming tax bill, an Offer in Compromise might be the only viable path forward. You can learn more about how an Offer in Compromise works to see if it’s a potential fit. By looking at all the tools available, you can build a strategy that doesn’t just release the levy, but finally puts your tax problems behind you.

Costly Mistakes to Avoid When Facing a Levy

Receiving a notice of levy from the IRS can feel like walking through a minefield. One wrong step can have some truly damaging financial consequences, turning an already stressful situation into a full-blown crisis. The single biggest mistake you can make? Doing nothing at all.

Ignoring the problem is a guaranteed way to make it worse. The IRS collection process is automated and persistent—it won't just go away. Failing to respond only escalates their actions and closes the door on your best opportunities to negotiate a manageable solution.

Another massive misstep is missing the 30-day deadline to request a Collection Due Process (CDP) hearing. This is, without a doubt, your most powerful right. Filing a timely CDP request legally stops most levy actions in their tracks, buying you invaluable time to negotiate without the immediate threat of your assets being seized. Letting that deadline slip is like handing over your best shield.

Providing Inaccurate or Incomplete Information

When you finally do communicate with the IRS, honesty is everything. If you submit a Collection Information Statement (Form 433-F) with information that's incomplete or, worse, outright false, you've just destroyed your credibility. The IRS will cross-reference your details, and if they find inconsistencies, they’ll likely deny your request for a resolution and ramp up their collection efforts.

Along those same lines, don't agree to a payment plan you know you can't afford. It might feel like a quick fix, but defaulting on an Installment Agreement lands you right back at square one, only now you have fewer options and have lost the IRS's trust. It's far better to be realistic and negotiate a sustainable plan based on what you can actually pay.

Be warned: an IRS wage levy can drastically reduce your take-home pay. However, federal law provides crucial exemptions to protect funds for basic living expenses, including an inflation-adjusted amount per dependent. You must proactively file the correct forms to claim these exemptions.

Misunderstanding Your Rights and Exemptions

It's also a huge mistake to not understand what the IRS can and cannot legally take. For instance, a wage levy can take a huge bite out of your paycheck, but federal law sets aside certain amounts to cover basic living expenses. The Tax Cuts and Jobs Act (TCJA) updated these figures, including a $4,300 exemption per dependent.

It’s on you to submit an updated exemption statement to your employer to make sure they withhold the right amount. If you don't, they might use an outdated formula, and the IRS could take far more than they're entitled to. You can learn more by reviewing the IRS levy exemption guidelines on IRS.gov.

Overlooking these protections can lead to severe financial hardship. The complexity of these rules highlights one final, critical point: trying to navigate an IRS levy on your own is often the most expensive mistake of all. Getting professional help can keep you from stepping on these landmines and protect your financial future.

Frequently Asked Questions About IRS Levies

When you're staring down something as serious as an IRS levy, the questions can start piling up fast. It’s a stressful, often confusing process, but getting clear answers is the first real step toward getting your financial life back on track. Let's tackle some of the most common questions people have when they receive that dreaded notice.

How Long Does an IRS Levy Last?

The answer really depends on what the IRS is targeting. Think of it as the difference between a one-time withdrawal and a continuous drain on your finances.

A bank levy is a one-shot deal. The IRS instructs your bank to freeze whatever is in your account on that specific day and send it over. Once those funds are gone, that particular levy is finished. Of course, if you still owe money, the IRS can absolutely issue another levy down the road.

A wage garnishment, on the other hand, is a completely different beast. It's continuous. Your employer is required to take a chunk out of every single paycheck and send it directly to the IRS. This keeps happening, paycheck after paycheck, until the debt is paid off, the levy is officially released, or you get into a formal payment plan.

The most important thing to remember is that a wage levy doesn't just go away on its own. It's designed to be a relentless collection tool that stays in place until you actively resolve the underlying tax problem.

Can the IRS Really Seize My Home or Car?

Yes, they can. The IRS has the legal power to seize and sell personal property—including your house and your car—to cover a tax debt. But, and this is a big "but," it's an extreme measure and usually the IRS's last resort.

Taking someone's home is a complicated legal maneuver that requires approval from high up the chain at the IRS. It's typically reserved for situations with very large tax debts where the taxpayer has ignored every other attempt at communication. While it's a real possibility, it's not common. The goal is always to address the notice of levy from the IRS long before things ever get to that point.

Will Filing for Bankruptcy Stop an IRS Levy?

Filing for bankruptcy often provides immediate and powerful protection. The moment you file, a legal protection called an "automatic stay" usually kicks in. This forces most creditors, including the IRS, to immediately stop all collection efforts. That means any active levies or wage garnishments have to be paused, at least for a while.

But there's a crucial distinction here: stopping a levy isn't the same as wiping out the tax debt. Whether the taxes you owe can actually be discharged in bankruptcy is a whole other, very complex question. It depends on the type of tax, how old the debt is, and if you filed your returns on time. This is where you absolutely need to talk to an attorney who understands both tax and bankruptcy law.

Is an IRS Levy the Same as a Michigan State Levy?

No, they are completely separate actions from two different government agencies. The basic idea is the same—seizing assets for unpaid taxes—but the rules, legal authority, and what you're allowed to keep (your exemptions) are totally different.

- An IRS levy comes from the federal government for federal taxes and follows federal law.

- A Michigan state levy comes from the Michigan Department of Treasury for state taxes and is governed by Michigan's own set of laws.

It's entirely possible to be hit with levies from both the IRS and the State of Michigan at the same time if you owe both federal and state taxes. Each needs to be dealt with separately.