How to Avoid Tax Penalties a Guide for Michigan Taxpayers

The easiest way to get hit with tax penalties is to miss a deadline or underpay what you owe. The IRS has a straightforward, if unforgiving, rule of thumb: you need to pay at least 90% of your current year's tax liability or 100% of the tax you owed last year. For most people, this comes down to making sure your employer is withholding the right amount from your paycheck or, if you're self-employed, sending in accurate quarterly estimated payments.

Falling short on these obligations is the fastest way to find yourself with costly fees that can quickly spiral.

The Real Cost of Ignoring Tax Penalties

Tax penalties aren’t just a slap on the wrist. They're significant financial setbacks designed to ensure everyone pays their fair share on time. The two most common penalties, for failing to file and failing to pay, are particularly nasty because they can stack up, turning a small tax bill into a major financial headache.

The IRS failure-to-file penalty alone is a brutal 5% of your unpaid taxes for each month your return is late. This penalty keeps growing until it hits a cap of 25% of your total tax bill. Compare that to the failure-to-pay penalty, which is much lower at 0.5% per month. This huge difference drives home the most important rule in tax compliance: always file on time, even if you don't have the money to pay the full amount.

A Real-World Scenario in Detroit

Let’s look at a real-life example. A self-employed contractor here in Detroit had a great year but got behind on his bookkeeping. He knew he owed about $20,000 in taxes but didn't file or make any estimated payments, thinking he'd just sort it out later. He blew past the April deadline.

Here's how quickly that decision came back to bite him:

- Five months later: The failure-to-file penalty maxed out at 25%, adding a whopping $5,000 to his bill.

- Ongoing penalties: At the same time, the failure-to-pay penalty was ticking up, adding another $500 over that same period.

- Interest charges: As if that weren't enough, interest started compounding daily on the original $20,000 and on the penalties that were just added.

In less than six months, his tax debt ballooned by more than 25%. What was once a manageable bill had become a genuine financial crisis. This is a classic example of the debt snowball that tax problems can create—it just gets bigger and harder to deal with the longer you wait.

Understanding and respecting your tax obligations is the single most effective way to protect your financial health. Proactive management isn't just about avoiding fees; it's about maintaining control over your financial future.

This guide is designed to give you the core strategies needed to stay on the right side of both federal and Michigan tax laws. From mastering deadlines to optimizing your payments, our goal is to show you how to handle your taxes with confidence and stop penalties before they ever become an issue. It all starts with recognizing the serious consequences of putting it off.

Mastering Deadlines to Prevent Penalties

Of all the ways to land in hot water with the tax authorities, simply missing a deadline is the most common—and the most avoidable. Both the IRS and the Michigan Department of Treasury run on a strict schedule, and being even a single day late can kick off a cascade of fees and interest charges.

For individuals and small business owners, getting these dates right isn't just good practice; it's the foundation of smart tax management.

Most people know the big one: April 15th, the due date for individual federal and state tax returns. But for countless business owners, freelancers, and investors, the tax calendar is a lot more crowded, dotted with quarterly estimated payments that can easily be missed.

An Extension to File Is Not an Extension to Pay

This is a critical point that trips up taxpayers every single year. Filing for an extension grants you an automatic six-month grace period to submit your tax forms, pushing the deadline to October 15th. What it absolutely does not do is give you more time to pay the taxes you owe.

Your tax payment is still due on the original April 15th deadline. If you file for an extension but haven't paid at least 90% of your total tax liability by that date, you'll start racking up failure-to-pay penalties and interest. This single misunderstanding leads to some nasty financial surprises for otherwise diligent people.

The cardinal rule is straightforward: Always file on time, even if you can't afford to pay the full amount. The failure-to-file penalty is significantly harsher than the failure-to-pay penalty, making it the one you must avoid at all costs.

Failing to file your return on time is one of the quickest ways to complicate your life. The IRS imposes a steep failure-to-file penalty that can make your tax debt balloon. For 2025, the minimum penalty under Code Sec. 6651(a) is projected to jump to $525, up from $510 in 2024. But that's just the floor—the penalty is 5% of your unpaid taxes for each month you're late, capped at a painful 25%.

Imagine you're a Detroit business owner who owes $10,000. Simply filing five months late could tack on $2,500 in penalties, and that's before any interest is calculated.

A Real-World Scenario: An Oakland County Entrepreneur

Let's look at a freelance consultant in Oakland County. She also brings in money from a rental property and has some stock investments. Her financial life is complex, with income arriving from multiple, irregular sources. This makes her tax calendar far more demanding than a typical W-2 employee's.

Here’s what her year looks like:

- Quarterly Estimated Taxes: She must calculate and pay estimated federal and Michigan taxes four times a year: April 15, June 15, September 15, and January 15 of the next year.

- Annual Filing: Her personal income tax return (Form 1040) is due April 15.

- Business Reporting: She also has to issue Form 1099-NEC to any subcontractors she paid over $600, and those are due by January 31.

Missing just one of these deadlines—especially an estimated payment—can trigger an underpayment penalty for that specific quarter. For a busy entrepreneur juggling clients and managing properties, it’s easy to see how a date could slip by. This is exactly why a proactive system is essential to avoid tax penalties. To grasp the full repercussions, it helps to understand what happens if you don't file taxes on time.

Actionable Steps to Stay on Schedule

Relying on memory alone is a recipe for disaster. The key is to build a reliable system that removes the guesswork and ensures you never miss a critical date.

Here are a few practical strategies you can put in place today:

- Use Digital Calendars: Don't just set one reminder. For every federal and state deadline, create alerts for one month out, one week out, and the day before it's due.

- Leverage Accounting Software: Modern accounting platforms can be set up to track tax deadlines for you. Many can even help you calculate estimated payments based on your real-time income.

- Create a Tax Binder: Go old-school with a physical binder (or a dedicated digital folder) that has a printed calendar of all your relevant tax dates for the year. Sometimes a simple visual is the most effective tool.

By turning deadline management into a process, you take back control of your tax obligations and dramatically reduce your risk of getting hit with unnecessary and expensive penalties.

Pay As You Go: Smart Withholding and Estimated Tax Strategies

Most people think of taxes as a once-a-year headache in April, but that’s a misconception that often leads to trouble. To stay clear of penalties, you need to think of tax compliance as a year-round activity. The goal is to pay your taxes as you earn the income, not all at once when you file.

For employees, this is handled through paycheck withholdings. For freelancers, gig workers, and small business owners, it means making quarterly estimated tax payments. Either way, the principle is the same: stay on top of your obligations throughout the year to avoid a nasty surprise.

Fine-Tuning Your W-4 Withholdings

Your Form W-4 is essentially the instruction manual you give your employer, telling them how much to set aside for taxes from each paycheck. If those instructions are wrong or outdated, you could easily end up owing a lot more than you expected come tax time, triggering underpayment penalties.

It’s crucial to revisit your W-4 whenever a major life event happens. Did you get married? Have a baby? Buy a house? Start a side gig? All of these things shift your tax situation and probably mean you need to adjust your withholding. A quick mid-year check-up using the IRS's free Tax Withholding Estimator tool can save you from a huge tax bill and penalties down the road.

Think of it this way: A quick W-4 review takes maybe 15 minutes. A tax penalty can cost you hundreds or thousands. It's one of the simplest, most effective ways to protect yourself.

The "Safe Harbor" Rule for Estimated Taxes

If you're self-employed or have other income not subject to withholding (like from investments or rental properties), estimated taxes are your best friend. The key to doing this right and avoiding penalties is to follow the IRS "safe harbor" rule. It gives you a clear, simple target for your payments.

To avoid an underpayment penalty, you generally need to pay at least:

- 90% of the tax you'll owe for the current year, OR

- 100% of the tax you owed for the previous year.

There's one important exception: if your prior year's Adjusted Gross Income (AGI) was over $150,000, that second target jumps to 110% of last year's tax. As long as your quarterly payments get you to one of these thresholds, you’re protected from penalties, even if you still have a balance due when you file.

A Real-World Example: A Lansing Freelancer's Strategy

Let's imagine a freelance graphic designer in Lansing with an income that goes up and down. Last year, her total tax bill was $12,000. To play it safe this year using the 100% rule, she knows her total estimated payments need to hit that same $12,000 mark, meaning she should aim for $3,000 each quarter.

But what if business is slow in the first quarter? She might only make enough to justify a $1,500 payment. Then, in the second quarter, a huge project comes in. If she just made a standard $3,000 payment, she'd be penalized for underpaying in Q1.

This is where the annualized income method comes in. It allows her to make a larger payment in Q2 to reflect when she actually earned the money, catching her up and preventing a penalty for the Q1 shortfall. For anyone with fluctuating cash flow, this kind of strategic adjustment is absolutely essential.

If you’re facing a tough financial spot and can’t keep up with payments, don’t just ignore it. Programs like the IRS Fresh Start Program for tax relief are designed to help you get back into compliance without making the problem worse.

Ensuring Accurate Reporting to Avoid Costly Errors

Meeting your filing deadlines is a huge part of staying on the right side of the IRS and the Michigan Department of Treasury, but it’s only half the battle. The accuracy of what you report is just as critical. A single mistake, whether it's an overlooked income stream or a deduction you can't back up, can trigger a nasty accuracy-related penalty—often as high as 20% of whatever you underpaid.

This isn't just a penalty for people trying to cheat the system. It can be applied for simple negligence or a disregard of the rules. Forgetting to report the income from that freelance project or side hustle is a classic example of a costly mistake the IRS can easily catch by cross-referencing the 1099 forms they receive.

Common Reporting Mistakes That Trigger Penalties

I've seen a few common reporting errors trip up taxpayers time and time again. One of the biggest is simply failing to report all sources of income. It's easy to focus on your main salary, but the government wants to know about everything, including:

- Freelance work or side gigs (often reported on Form 1099-NEC)

- Interest and dividends from your investments

- Capital gains from selling stocks or property

- Income from a rental property

Another major red flag for the IRS is playing fast and loose with deductions or credits. You should absolutely take every deduction you're entitled to, but claiming expenses you can't substantiate is a direct path to an audit and penalties. A great way to stay organized and ensure you're only claiming what's legitimate is to use a high-quality small business tax deductions list as a guide. It helps prevent both overpaying and raising unnecessary flags.

The High Stakes of Foreign Account Reporting

When it comes to accuracy, the stakes skyrocket for U.S. taxpayers with financial interests outside the country. Failing to properly disclose foreign bank accounts, investments, or other assets can lead to some of the most severe penalties in the entire tax code. The rules here, governed by the Foreign Account Tax Compliance Act (FATCA) and the Report of Foreign Bank and Financial Accounts (FBAR), are notoriously unforgiving.

For accounts with a balance over $10,000, a simple non-filing error can result in penalties starting at $10,000 per violation. If the IRS determines the failure was willful, the penalty can jump to the greater of $100,000 or 50% of the account balance. With global tax regulations constantly shifting, getting these details right is non-negotiable.

One taxpayer’s mistake can create a shared nightmare. Meticulous, independent review of a joint return is not just good practice—it's essential self-protection.

When One Spouse's Error Affects Both

The need for precision is amplified when you file a joint tax return. The term the IRS uses is "jointly and severally liable," which is a legal way of saying they can come after either one of you for the full amount of tax, interest, and penalties owed. It doesn’t matter who earned the income or who made the mistake.

Imagine a Michigan couple. One spouse runs a small business and the other is a W-2 employee. If the business owner underreports their income, leading to a huge tax bill and an accuracy penalty, the IRS can legally pursue the W-2 employee for the entire debt, even if they had no idea what was happening with the business's books.

Yes, there's a process called "innocent spouse relief," but qualifying is a tough, uphill battle. You have to prove you were completely unaware of the error and had no reason to even suspect it. This really drives home a critical point: always review and understand your joint tax return before you sign it, no matter how much you trust your partner. Your signature makes you 100% responsible.

Ultimately, preventing these accuracy-related penalties comes down to one fundamental practice: diligent record-keeping. Maintaining organized, detailed records for every dollar of income and every expense is your best defense against errors. It’s also the strongest evidence you can have if the IRS ever questions your return. This proactive approach is the bedrock of avoiding tax penalties and securing your financial peace of mind.

How to Request Penalty Abatement

Even with the most diligent planning, life happens. Sooner or later, a penalty notice from the IRS or the Michigan Department of Treasury might land in your mailbox. Seeing that official envelope is stressful, but it doesn't have to be the final word.

You can formally ask the tax authorities to remove a penalty through a process called penalty abatement. It’s a powerful tool, but your success depends entirely on building a clear, compelling case backed by solid evidence. This is where we move from prevention to resolution.

Understanding Reasonable Cause

The most common path to getting a penalty waived is by proving reasonable cause. This isn’t just a simple excuse; it's a specific legal standard. To meet it, you have to show that you acted with ordinary business sense and care but were still unable to file or pay on time because of circumstances completely out of your control.

Think of it from the IRS's perspective: they understand that true catastrophes occur. A sudden, severe illness that puts you in the hospital, a fire that destroys your home and records, or the death of a spouse who handled the finances are all classic examples that can establish reasonable cause.

Just claiming hardship won't cut it, though. You need to provide dated, specific documentation to back up your story. This could be:

- Hospital admission forms or a detailed doctor's letter.

- FEMA reports or insurance claims after a natural disaster.

- A death certificate for an immediate family member who was responsible for your taxes.

The goal is to draw a direct line from the event to your inability to meet your tax obligations.

The First-Time Abatement Lifeline

For taxpayers with an otherwise spotless record, the IRS offers a much simpler option: the First-Time Abatement (FTA). This is a huge relief for people who just made an honest mistake. It's essentially a one-time "get out of jail free" card, but you have to meet a few key requirements to use it.

To qualify for an FTA, you must show:

- A Clean Filing History: You’ve filed all required returns for the past three years.

- A Clean Payment History: You’ve paid or have a plan in place to pay any tax you owed for the past three years.

If you check these boxes, you can often get penalties for failure-to-file, failure-to-pay, and failure-to-deposit waived without having to go through the whole reasonable cause argument. It’s a great program that rewards taxpayers for their history of doing the right thing.

The First-Time Abatement is your reward for past diligence. If you've maintained a clean record, don't hesitate to ask for this relief. It acknowledges that even the most careful taxpayers can make a mistake.

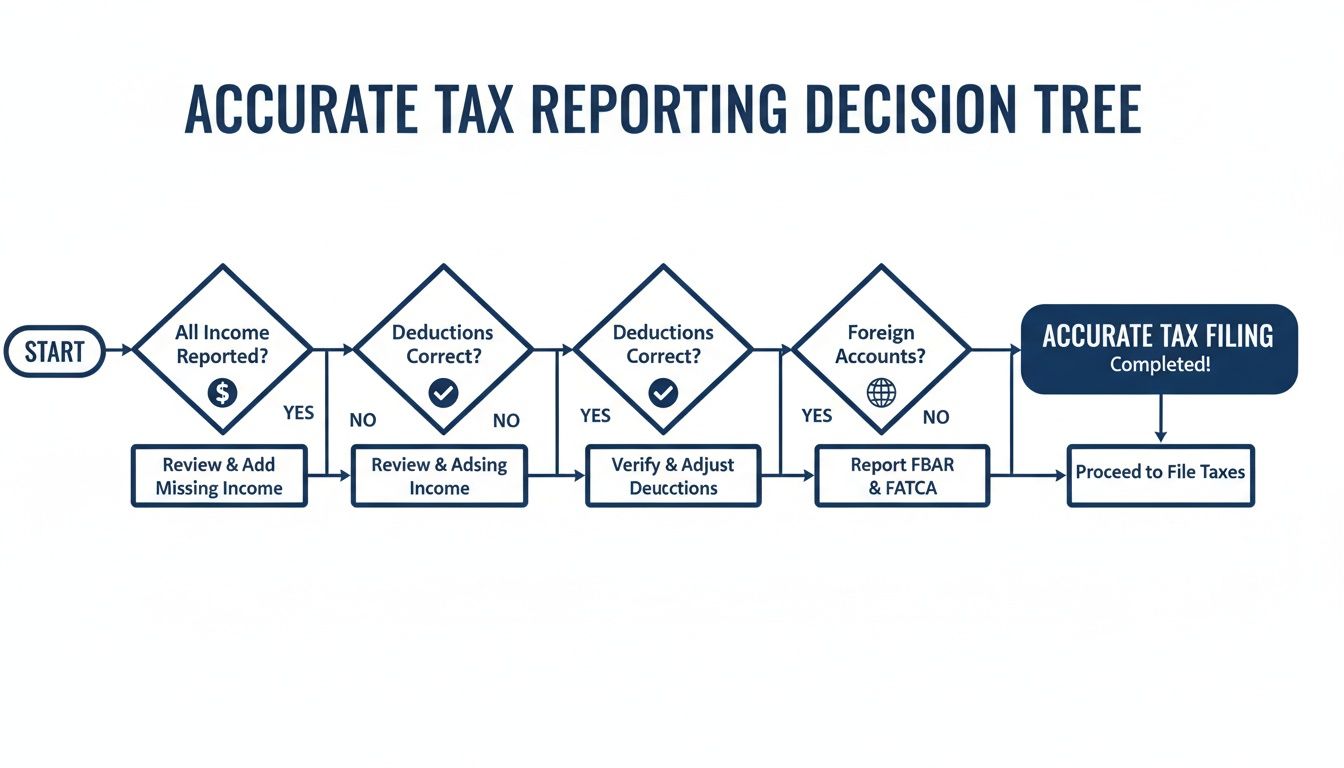

This decision tree shows the kind of careful thinking that helps prevent penalties in the first place—by getting your reporting right from the start.

As the graphic illustrates, compliance is a process. It takes careful attention to all your income, deductions, and any special reporting requirements to stay out of trouble.

When to Bring in a Professional

So, can you handle a penalty abatement request yourself? For a simple First-Time Abatement on a small penalty, you can often do it yourself with a phone call or a letter. If you want to dive deeper into the paperwork, you can learn more about how to use Form 843 for abatement in our dedicated article.

However, the game changes when the stakes get higher. It's time to call a tax professional immediately if:

- The penalties are substantial. When thousands of dollars are on the line, you don't want to risk a DIY request.

- Your situation is complex. Proving reasonable cause because you relied on bad advice from a tax preparer, for example, requires a sophisticated legal argument.

- You're under audit. Never, ever try to negotiate penalties while you're being audited without professional representation.

- You have several years of unfiled returns. A pro can help you get back into compliance first—a crucial step before you even think about asking for abatement.

An experienced tax attorney knows how to frame your story in the best possible light, which documents will make a difference, and how to speak the IRS's language. We understand the internal rulebook and are skilled negotiators, which can dramatically increase your chances of getting those penalties wiped away.

Answering Your Top Questions About Tax Penalties

When you're dealing with taxes, a lot of questions can pop up. Let's tackle some of the most common ones we hear from our Michigan clients. Getting these answers straight can help you sidestep some serious financial headaches down the road.

What’s the Difference Between a Failure-to-File and a Failure-to-Pay Penalty?

This is a crucial distinction, and the financial consequences are worlds apart.

The failure-to-file penalty hits you when your tax return isn't in by the deadline. The IRS charges a steep 5% of your unpaid tax bill for every month you're late. This penalty can climb all the way up to 25% of what you owe.

On the other hand, the failure-to-pay penalty is for when you've filed on time but haven't paid the full tax amount due. This one is much less severe, usually just 0.5% of your unpaid taxes per month.

The takeaway here is simple but powerful: always, always file your return on time, even if you know you can't pay the bill right away. The filing penalty is ten times higher, so you can save yourself a massive amount of money by just getting the paperwork in. You can always work out a payment plan later, but that late-filing penalty is a beast you want to avoid.

Can I Get Penalties Waived if My Tax Preparer Messed Up?

Yes, this is definitely possible. If your tax professional made a mistake, you can often request penalty abatement under the "reasonable cause" argument. But—and this is a big but—the burden of proof is entirely on you.

You'll need to demonstrate two things to the IRS or the Michigan Department of Treasury:

- You gave your preparer all the correct information in a timely manner.

- The error was truly their fault and not due to incomplete or inaccurate data you provided.

This is where your record-keeping becomes your greatest asset. Save your emails, keep copies of receipts, and maintain a clear paper trail. This documentation is essential for proving you did your part. A tax resolution expert can be a huge help in organizing this evidence and presenting a compelling case on your behalf.

I’m Self-Employed in Michigan. How Do I Avoid an Underpayment Penalty?

If you're self-employed, the name of the game is making consistent quarterly estimated tax payments. This is how you stay ahead of the curve and avoid a nasty surprise at tax time. Your guiding principle here is the "safe harbor" rule.

The safe harbor rule is your shield against penalties. It protects you as long as you pay at least 90% of what you owe for the current year, or 100% of what you owed for the previous year. (Note: that 100% figure jumps to 110% if your Adjusted Gross Income last year was over $150,000).

Since your income as a freelancer or business owner can go up and down, it's a good practice to revisit your estimated payments each quarter. A little proactive management can prevent a huge, unexpected tax bill and the penalties that come with it.

I Just Got a Penalty Notice. What Should I Do?

First things first: don't ignore it. A tax notice is not something that gets better with time; it only gets more serious. Open that letter immediately. Read it carefully to understand which tax period it's for, the specific reason for the penalty, and the total amount they say you owe.

If you think the penalty is wrong or if you have a legitimate reason for the delay—like a serious illness, a family emergency, or a natural disaster—you have the right to contest it. Your next step is to gather every piece of supporting documentation you can find and make sure you respond before the deadline listed on the notice.

If the situation feels complex, the dollar amount is significant, or you're simply feeling overwhelmed, your best bet is to call a professional. A firm like Defense Tax Partners can step in immediately, handle all communications with the tax agencies for you, and work to secure the best possible outcome.