Does the IRS Garnish Wages and How Can You Stop It

Yes, the IRS can and absolutely will garnish your wages if you have unpaid tax debt. It’s one of the most powerful tools in their collection arsenal.

This process is officially called a wage levy, and it allows the IRS to legally take money right out of your paycheck to satisfy your tax liability. It’s a shock for many people to learn that, unlike private creditors, the IRS doesn't need a court's permission to do this.

Understanding the IRS Wage Garnishment Process

When you hear "garnishment," you probably picture a lawsuit. For most debts, like credit cards or medical bills, a creditor has to sue you, win in court, and get a judge's order before they can touch your paycheck.

The IRS, however, plays by a different set of rules. Its authority to collect taxes comes directly from the U.S. tax code itself, which gives it a powerful shortcut.

This means the IRS can skip the court system entirely. Once they've sent you the required series of legal notices, they can directly order your employer to start withholding a significant chunk of your pay. This is an administrative process, not a judicial one, making it much faster and more aggressive.

An IRS wage levy is not a negotiation; it is a legal demand placed upon your employer. The moment your employer receives the levy notice, they are legally obligated to comply and send the specified funds to the IRS, or they could become liable for your tax debt themselves.

This is a critical distinction to understand. While a private creditor has to prove their case, the IRS already has the legal authority on its side.

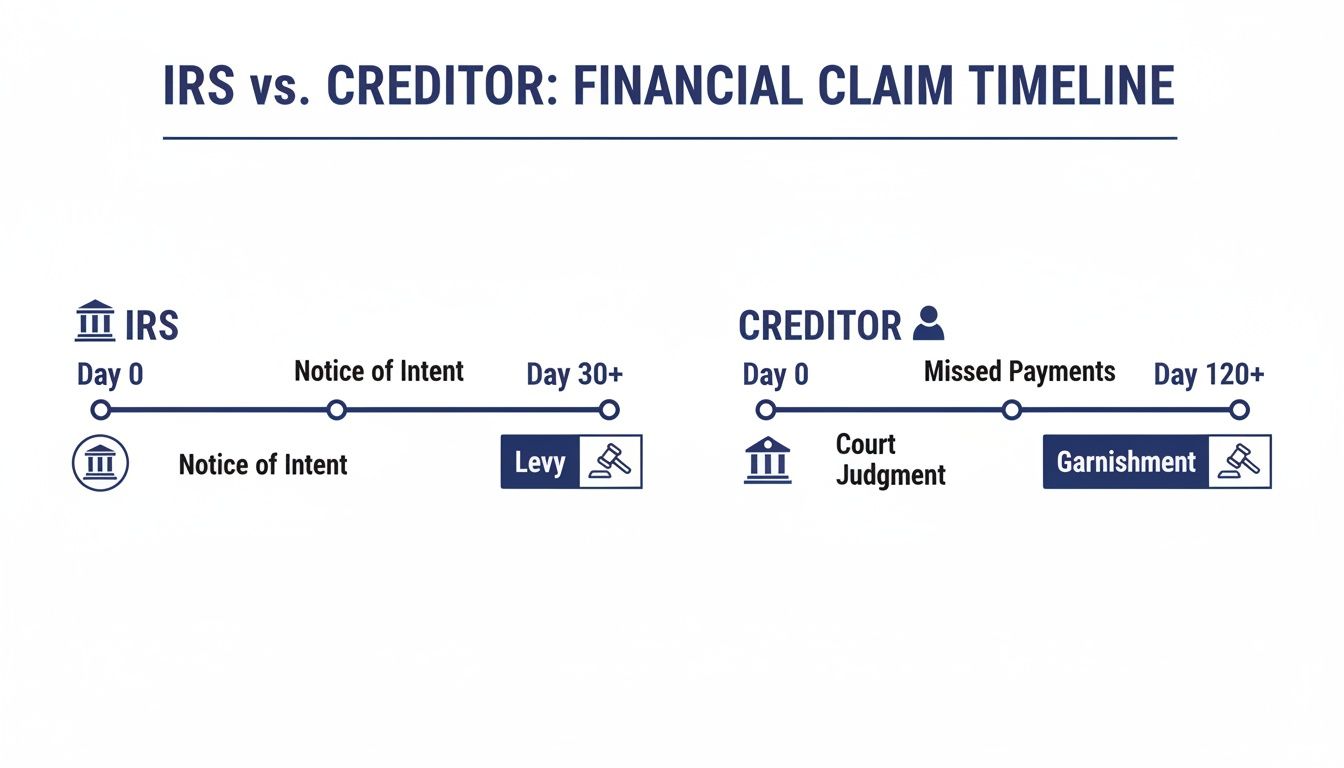

IRS Wage Levy vs Private Creditor Garnishment

To see just how different the IRS's power is, let's compare it directly to what a typical private creditor must do to garnish your wages.

| Feature | IRS Wage Levy | Private Creditor Garnishment |

|---|---|---|

| Court Order Required? | No | Yes |

| Legal Basis | U.S. Tax Code (Administrative) | Court Judgment (Judicial) |

| Process Speed | Fast, once notices are sent | Slow, requires a full lawsuit |

| Amount Taken | Significant portion, based on dependents | Limited by federal/state law (usually up to 25% of disposable income) |

| Employer Obligation | Legally binding; employer can be held liable | Legally binding upon receiving a court order |

As you can see, the IRS has a direct and potent path to your income.

This non-judicial power is precisely why an IRS notice should never be ignored. The agency's ability to act swiftly makes it one of the most effective creditors out there.

The good news? The process isn't instant and the IRS must send several warnings first. Understanding the difference between an IRS levy and a standard garnishment is the first step in knowing how to protect yourself. To dig deeper, you can learn more about what a tax levy is and how it functions in our detailed guide. Mastering these basics is the foundation for building a strong defense.

The Warning Signs Before a Wage Levy Begins

An IRS wage levy is a serious financial gut punch, but it never comes out of the blue. The IRS is legally required to follow a very specific notification process before they can touch your paycheck. Think of these letters not as simple bills, but as a series of increasingly loud alarm bells demanding your immediate attention.

It all starts with a letter like the CP14, Notice and Demand for Unpaid Tax. This is the first official bill outlining what you owe and when it’s due. If that letter goes unanswered, you'll start receiving a string of follow-up notices, each one a bit more insistent than the last.

The Critical Countdown Clock

The one letter you absolutely cannot ignore is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This is usually a Letter 1058 or LT11, and it's the final warning shot before the IRS takes action.

Once that Final Notice lands in your mailbox, a 30-day countdown officially begins. This is your last chance to pay the debt, set up a payment plan, or formally appeal. If you don't act within this window, the IRS gets the green light to contact your employer and start taking money directly from your wages.

Ignoring these notices is a recipe for disaster. We had a client from Lansing, Michigan, who had been setting a stack of IRS letters aside, assuming they were just duplicates of the same bill. He was completely blindsided when his paycheck was suddenly 40% lighter. He never realized that final notice had started a ticking clock on his income. This kind of real-world shock is exactly why you have to be proactive.

Understanding the Process

The IRS issues hundreds of thousands of levies every year; it’s one of their most powerful tools for collecting from taxpayers who aren't communicating. And unlike a credit card company that needs a judge's permission, the IRS can go straight to your employer once they've sent the required warnings. All they need is that 30-day waiting period after the final notice to expire.

This chart really drives home how much more direct the IRS's power is compared to a private creditor.

As you can see, the IRS has administrative authority, meaning they don't have to navigate the court system like other creditors. To protect yourself, it’s critical to understand the Wage Garnishment: 4 Things To Know Before It Happens, especially the early warning signs. Knowing what to look for is your best defense. For a deeper dive into what these official documents look like, check out our guide on the IRS notice of levy.

How Much Can the IRS Actually Take From Your Paycheck?

It’s a common misconception that an IRS levy just snatches a simple percentage of your income. The reality is a bit more calculated—and often much more aggressive. The IRS is legally required to leave you with a small slice of your paycheck for basic living expenses, but everything else is fair game.

This protected slice is known as your exempt amount. Think of it as the bare minimum the government figures you need to get by. Anything you earn above this specific, government-defined threshold is what the IRS will seize from every single paycheck until your debt is paid in full.

While there’s a formula, it's a cold one. It leaves most people with far less money than they need to cover their actual monthly bills, which is why a wage levy can feel so financially crippling.

How the IRS Figures Out Your Exempt Amount

The IRS doesn't care about your real budget—your mortgage, car payment, or utility bills don't factor in. Instead, they use a rigid, standardized formula found in IRS Publication 1494. This calculation hinges on just three things:

- Your Tax Filing Status (Single, Married Filing Jointly, etc.)

- The Number of Dependents you claim.

- Your Pay Period (weekly, bi-weekly, monthly).

When your employer receives the levy notice, they use these details to look up a specific number on a table. That number is your exempt amount. Every dollar you earn above it is sent straight to the IRS.

The most important thing to understand is that this "exempt" amount is not generous. It's a survival-level figure designed to cover only the most basic necessities, not the financial realities of your life. This is precisely what makes a wage levy so devastating.

Here’s a look at what some of those exempt amounts might be. These figures, based on the formula, show the approximate take-home pay that is protected each week.

Estimated Weekly Income Exempt from IRS Levy

This table shows the approximate weekly take-home pay that is protected from an IRS levy, based on filing status and number of claimed exemptions. (Note: Values are illustrative examples based on IRS formulas).

| Filing Status | Personal Exemptions Claimed | Approximate Weekly Exempt Amount |

|---|---|---|

| Single | 1 | $263 |

| Single | 3 | $452 |

| Married Filing Jointly | 2 | $527 |

| Married Filing Jointly | 4 | $715 |

As the table shows, the more exemptions you claim, the more income is protected. However, the amount the IRS can still take remains substantial.

Real-World Examples in Michigan

Let's put this into perspective with a couple of real-world Michigan scenarios. The exact dollar amounts are updated by the IRS periodically, but the math and its impact are always the same.

Example 1: A Single Individual in Detroit

Imagine a single person paid bi-weekly who claims one exemption. Their protected amount is around $527 every two weeks. If their bi-weekly take-home pay is $1,500, the IRS can legally take the remaining $973 right out of that single paycheck.

Example 2: A Family in Grand Rapids

Now, consider a head of household with three children who gets paid every week. Their protected amount would be much higher, around $682 per week. But if their weekly take-home pay is $1,200, the levy would still capture $518 every single week.

These examples transform the vague fear of a wage levy into a hard number. They show exactly what’s at stake and underscore why you have to act fast to get a resolution in place before your finances are completely derailed.

How to Stop an IRS Wage Garnishment

Getting that final notice of intent to levy can feel like the walls are closing in, but it’s not game over. Think of it as the IRS putting the ball in your court. You have several powerful moves you can make to protect your paycheck, but you have to act.

The absolute worst thing you can do is ignore the situation; that’s a surefire way to have the levy go through. The single most important step is to open a line of communication with the IRS. By getting back in touch and showing you’re serious about resolving the debt, you can almost always find a better solution than having your wages seized.

Set Up an Installment Agreement

One of the most straightforward and common solutions is an IRS Installment Agreement (IA). It's simply a formal payment plan, letting you chip away at your tax debt with a manageable monthly payment you can actually afford. As soon as the IA is approved and you make that first payment, the IRS stops all collection activities, including any pending wage levy.

- Who it’s for: People who can’t pay the full balance today but can afford to make consistent monthly payments over time.

- What you need to know: You have to be up-to-date on filing all your tax returns. Stick to the monthly payments and stay current on your future taxes, or the agreement could default.

If your total debt is under $50,000, you can often set up a streamlined agreement right on the IRS website without having to turn over tons of financial paperwork. For larger debts, the process gets more detailed, but it’s still one of the most reliable ways to keep your paycheck intact.

Qualify for Currently Not Collectible Status

What if you're facing a true financial crisis? If you can't even cover basic living expenses, let alone a tax bill, you might qualify for Currently Not Collectible (CNC) status. This isn’t debt forgiveness—it's a temporary pause button on all collections. The IRS essentially agrees that forcing you to pay right now would cause significant hardship.

To get this status, you'll need to open your books and provide a complete financial picture to prove you can't pay. The IRS will look closely at your income, essential expenses, and any assets you have.

Once you're placed in CNC status, the IRS will halt wage garnishments, bank levies, and other collection actions. They will typically review your financial situation every year or two to see if things have improved enough for you to start paying again.

Keep in mind that interest and penalties will keep adding up while you're in CNC status. However, it provides crucial breathing room to get your finances stabilized without the immediate threat of a levy.

Negotiate an Offer in Compromise

The Offer in Compromise (OIC) is a powerful tool that allows some taxpayers to settle their debt with the IRS for less—sometimes much less—than the full amount owed. It's an option when the IRS is convinced it's unlikely to ever collect the full balance before the collection statute expires.

This is what’s known as "doubt as to collectibility."

- Who it’s for: Taxpayers buried under a mountain of tax debt with limited income and few assets to their name.

- What you need to know: The OIC application is notoriously complex and requires a deep dive into your finances. You have to prove that paying the full amount would create a legitimate economic hardship.

Getting an OIC approved is tough, no question. But for those who qualify, it can be a truly life-changing resolution. A successful offer doesn't just stop a wage garnishment—it settles the underlying tax debt for good, giving you a fresh start.

Finding Relief Through Special Tax Programs

Beyond standard payment plans, the tax code has some powerful built-in relief programs for people in truly difficult situations. Think of these as a lifeline when you're facing a wage levy. They get to the root of the problem in a way that a simple payment plan just can't.

Two of the most important options are Innocent Spouse Relief and Penalty Abatement. These programs exist because the IRS understands that not all tax debt is created equal. Sometimes, the liability isn't really your fault, or the penalties are just unfairly punishing given what you've been through. Exploring these avenues is often a crucial step in stopping the IRS from taking your wages.

Innocent Spouse Relief

Can you imagine finding out you owe the IRS thousands of dollars because of a tax return your ex-spouse filed years ago—a return you signed without knowing the full picture? It happens more often than you'd think. This is exactly why Innocent Spouse Relief was created. It’s designed to legally separate you from tax debt created by your current or former spouse, freeing you from a financial burden you had no hand in creating.

To have a shot at qualifying, you generally need to prove a few key things:

- You filed a joint return that has an understated tax liability.

- That understatement came from erroneous items—like unreported income or false deductions—attributable to your spouse.

- You can show that when you signed the return, you genuinely did not know, and had no reason to know, about the tax understatement.

- Looking at all the facts and circumstances, it would be unfair to hold you responsible for the debt.

If the IRS grants this relief, it can completely wipe out your responsibility for the tax, interest, and penalties. Once that happens, the threat of wage garnishment vanishes along with it.

This isn't about blaming a former partner. It's about building a factual case for the IRS that proves you were kept in the dark about financial missteps. When you successfully prove your case, you can sever your connection to that debt for good.

Penalty Abatement

IRS penalties can be brutal. They can quickly snowball, sometimes doubling or even tripling the original tax bill. The good news is the IRS has the authority to remove—or "abate"—these penalties if you can show you had reasonable cause for not filing or paying on time.

"Reasonable cause" isn't just a flimsy excuse. It’s a legitimate, often unavoidable, situation that prevented you from meeting your tax obligations. We're talking about things like a sudden serious illness, a death in the immediate family, destruction of your records in a fire or flood, or even relying on bad advice from a tax professional.

If you're successful, you'll still owe the original tax and the interest that has accrued. But getting thousands of dollars in penalties waived can make the remaining balance far more manageable. Removing that chunk of debt often makes it possible to qualify for a better solution, like a smaller installment agreement or even an Offer in Compromise.

An Offer in Compromise is a formal agreement with the IRS to settle your tax debt for less than the full amount you owe. Learn more by reading our guide explaining what an Offer in Compromise is and how it can provide a fresh start.

Why a Tax Attorney Is Your Strongest Ally

Trying to handle an IRS wage levy on your own is a tough, often losing, battle. Think of it like walking into a courtroom without a lawyer—the rules are confusing, the deadlines are unforgiving, and the stakes couldn't be higher. When you bring in an experienced tax attorney from Defense Tax Partners, you're not just getting help; you're changing the entire dynamic. You go from being a target to someone with a powerful advocate in their corner.

An attorney is both your shield and your sword. In many cases, a single, well-placed phone call from our firm to the IRS can halt a levy right in its tracks. This gives us the breathing room needed to work out a lasting solution. It’s not about stalling; it’s about taking back control.

The Strategic Edge of Professional Representation

Having a tax attorney on your side gives you some immediate, critical advantages. We take over all the stressful calls and correspondence with IRS Revenue Officers, so you don’t have to. We’ve been doing this for years, so we know exactly what financial information to provide—and, just as importantly, how to frame it—to build a compelling case for financial hardship or to get you into a favorable settlement program.

This kind of expertise is more critical now than ever. The IRS is ramping up its collection machine with AI, which means everything happens faster. Accounts get flagged and escalated for levy much quicker than in the past, making that 30-day notice period feel incredibly short. You can get more details on how the IRS is leveraging technology for wage garnishments on TaxFortress.com.

An experienced attorney knows how to get past the IRS's automated gatekeepers and speak to the right human decision-maker. We can escalate your case and negotiate a resolution that protects your paycheck and your financial stability.

There's another crucial layer of protection: confidentiality. When you're sharing sensitive financial details, it's vital that you can speak freely. By understanding attorney-client privilege rules, you’ll see how this legal shield keeps our conversations completely private. A tax attorney isn't just a negotiator; we are your confidential advisor, completely focused on securing the best possible outcome for you.

Here are some of the most pressing questions we hear from clients facing an IRS wage levy, along with straight-talk answers.

Can the IRS Really Take My Social Security?

Yes, they absolutely can. The IRS has the power to levy federal payments, which includes both Social Security retirement and disability benefits.

There is a limit, though. They can't take everything. The IRS is generally restricted to taking up to 15% of your monthly benefit payment. It's also crucial to know that Supplemental Security Income (SSI) is completely off-limits and cannot be touched by an IRS levy.

How Long Will This Wage Garnishment Go On?

An IRS wage levy isn't a one-and-done deal. It's continuous and will keep taking a portion of your money from every single paycheck you get.

This will continue indefinitely until one of three things happens: the tax debt is finally paid off, you negotiate a formal resolution with the IRS (like an installment agreement), or the legal time limit for collections—typically ten years—runs out.

A wage levy is relentless by design. It's meant to get your attention and will not stop on its own. You have to take action to get it released.

Does My Boss Have to Know About This?

Unfortunately, yes. Your employer will be directly involved. The process starts when the IRS sends a legal notice, Form 668-W, right to your company's payroll department.

This form legally requires your employer to calculate the levy amount from your pay and send it directly to the IRS. There's no way to keep it private; they become a key part of the collection process.