How to Remove a Tax Lien: A Michigan Homeowner’s Guide

Receiving a notice about a tax lien is an undeniably stressful experience, but navigating your way out of it is more straightforward than you might imagine. The core of the issue is the underlying tax debt. To get the lien removed, you'll either need to pay that debt in full or work out a formal resolution with the IRS or the Michigan Department of Treasury, like an Offer in Compromise or an Installment Agreement. The most important thing is to act quickly and decisively—it’s the best way to protect your property and get your financial life back on track.

Your First Steps After Discovering a Michigan Tax Lien

When a Notice of Federal Tax Lien (NFTL) or a Michigan State Tax Lien shows up in your mailbox, it's natural to feel a wave of panic. It’s critical to first understand what a lien actually is—and what it isn't. A tax lien isn't a seizure of your property. Rather, it's a legal claim the government places against your assets to secure its interest in the debt you owe. Think of it as a public "hold" on your property, whether it's your house, your car, or your business equipment.

This public filing is where the real trouble begins. It can stop you dead in your tracks if you're trying to sell property, refinance a mortgage, or get a loan for your business. And while the lien itself doesn't take your assets, it’s often the first shot across the bow before more aggressive collection actions start. To see what could come next, you can explore our guide on the differences between a tax lien and a tax levy.

Verify the Lien’s Legitimacy

Before you do anything else, make sure the notice is real. The first thing I tell my clients is to look for official letterhead from the IRS or the Michigan Department of Treasury. Carefully review the notice for your name, the specific tax periods involved, and the exact amount they claim you owe. Pay close attention to any deadlines mentioned, as they are non-negotiable.

If anything feels off or looks suspicious, don't use the phone number on the letter. Go directly to the agency's official website and call them using a number you find there. This simple step can protect you from sophisticated scams.

Understand the Impact on Your Credit

Here’s some good news that surprises many people: a tax lien no longer directly tanks your credit score. Back in 2018, all three major credit bureaus—Experian, Equifax, and TransUnion—made a huge policy change and stopped including tax liens on consumer credit reports. This was a massive relief for taxpayers, as it meant the lien itself wouldn't automatically drag down their FICO score.

But don't let that give you a false sense of security. Even though it's off your credit report, the lien is still a public record. Lenders, potential business partners, or anyone else conducting a public records search can easily find it, which could still derail loan applications and other financial opportunities.

This is precisely why getting a tax lien removed remains a critical priority. I’ve seen small business owners in Detroit with excellent credit scores get denied for crucial inventory loans simply because a public lien record spooked the lender. The IRS used to file Notices of Federal Tax Liens for debts as low as $10,000, and while those thresholds have shifted, the chilling effect on business owners is still very real.

Just look at the numbers. In fiscal year 2024, collections from the Treasury Offset Program—an enforcement tool often tied to lien filings—reached a staggering $3.8 billion. This demonstrates just how seriously the government pursues these debts. Successfully removing a lien is the only way to truly clear the path to your financial recovery.

Evaluating Your Strategic Options for Lien Removal

Once you have the full picture of the lien filed against you, it’s time to shift from analysis to action. Seeing a Notice of Federal Tax Lien can feel like hitting a wall, but it’s really just a signal to get strategic. The right path forward depends entirely on your financial reality—whether you're a homeowner in Oakland County trying to refinance or a small business owner in Grand Rapids who needs to free up capital.

The most straightforward solution is, of course, paying the tax debt in full. It’s the cleanest route. Once the IRS or the Michigan Department of Treasury gets the full payment, they have 30 days to issue a Certificate of Release of Federal Tax Lien. This document officially wipes the government's claim from your property. But for many people, coming up with that kind of cash isn't realistic. Fortunately, it's far from the only option.

Release Versus Withdrawal: What’s the Difference?

This is a critical distinction that many people miss. A lien release and a lien withdrawal sound similar, but they have very different impacts on your financial future.

- A Lien Release is what happens automatically after you pay the debt. It shows the debt is satisfied, but the Notice of Federal Tax Lien (NFTL) remains on your public record. Think of it as a resolved issue that still shows up in your history.

- A Lien Withdrawal, on the other hand, completely removes the public NFTL as if it were never filed. This is the gold standard for protecting your credit and financial reputation because it erases the public mark against you entirely.

You have to specifically request a withdrawal. The IRS will often grant one if it's in everyone's best interest—for instance, if withdrawing the lien helps you get a loan that allows you to pay off your tax debt much faster.

Handling Specific Assets with a Discharge or Subordination

What if you can't pay the full debt right now but need to sell a specific asset, like your home? A full release is off the table, but you still have some powerful tools to work with.

A Discharge of Property is the perfect tool for this situation. It removes the tax lien from one particular piece of property, which lets you sell it with a clear title. The IRS will usually grant a discharge as long as the proceeds from the sale go directly to them to pay down your tax debt. We see this all the time with Michigan homeowners who are stuck, unable to sell their house because of a lien.

Then there’s Subordination. This option doesn't remove the lien, but it allows another creditor—like a mortgage lender—to jump ahead of the IRS in the line for payment. This is incredibly useful if you need to refinance. Most lenders won’t touch a refinance unless their new loan is in first position, and subordination is what makes that happen.

Real-World Scenario: Imagine a family in Lansing needs to refinance their home. They want to get a lower interest rate and use the cash to start paying off their tax debt. Their lender, however, insists on being in first priority. By successfully requesting a subordination from the IRS, the family lets the new mortgage take precedence over the tax lien. The loan gets approved, and they now have a clear path to paying off the IRS.

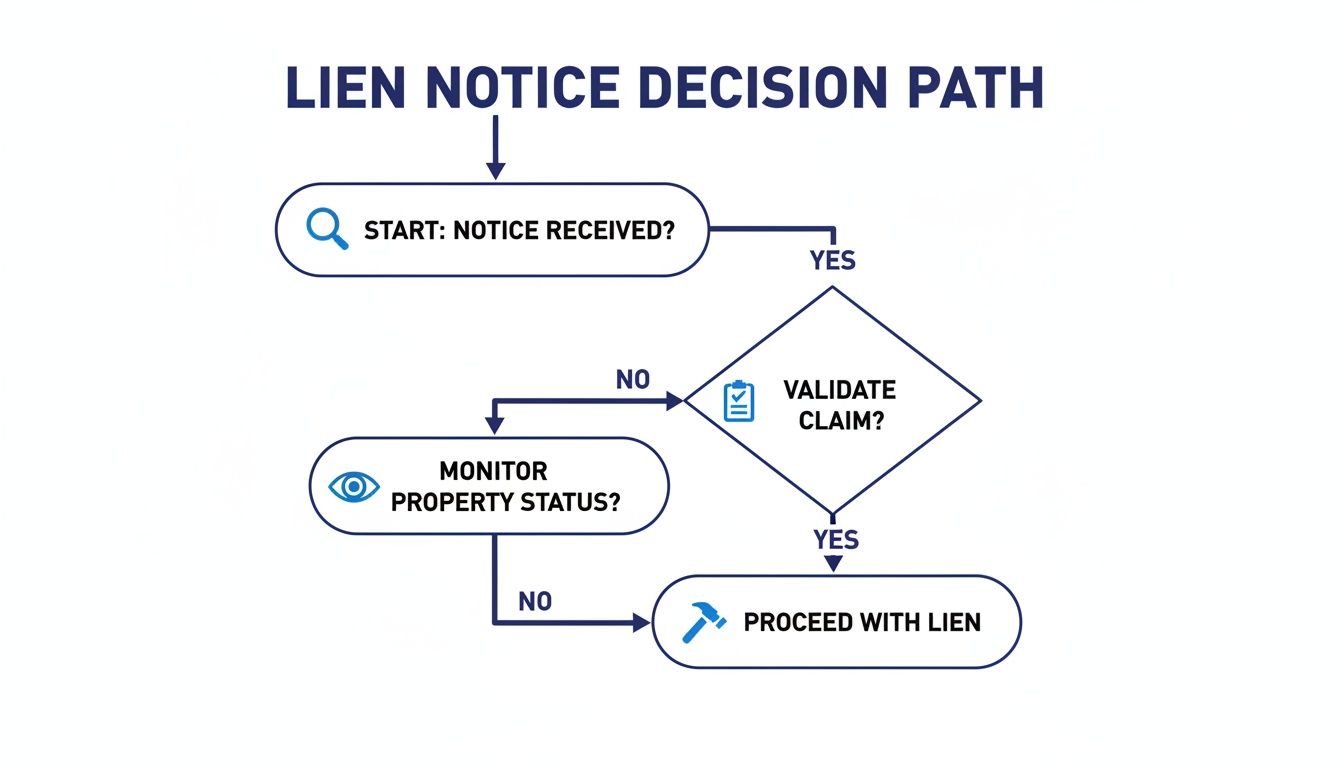

Visualizing the Lien Resolution Process

Knowing what to do right after you receive a notice can be overwhelming. This decision path helps clarify the immediate first steps you should take to get the process started.

As the flowchart shows, the absolute first thing you must do is verify the notice's authenticity. This ensures you're responding to a legitimate government claim before you start exploring your options.

It's also worth knowing that these aggressive lien strategies aren't always the government's only move. For taxpayers with debts between $10,000 and $25,000, research shows that simple monthly reminder letters were nearly as effective as liens in securing payment. This data just goes to show how important it is to communicate proactively and look at all your settlement options before a lien makes everything more complicated.

Beyond just tackling the immediate problem, it's wise to think about the bigger picture and learn how to protect your wealth from future tax issues. Making the right choice now doesn't just clear a current hurdle; it helps build a more secure financial foundation for the years to come.

Tax Lien Removal Options at a Glance

Navigating these options can be complex. This table breaks down the most common strategies to help you see which one might be the best fit for your situation.

| Method | Primary Goal | Best For Taxpayers Who… | Outcome |

|---|---|---|---|

| Full Payment | Settle the debt completely and quickly. | Have the funds to pay the entire tax liability. | Lien is released within 30 days; notice remains on public record. |

| Withdrawal | Remove the public notice of the lien. | Can prove the lien was filed in error or if removal helps pay the debt. | Public Notice of Federal Tax Lien is removed as if never filed. |

| Discharge | Free a specific asset from the lien. | Need to sell a particular piece of property (like a house or car). | The lien is removed from the specified asset, allowing for a clean sale. |

| Subordination | Let another creditor take priority over the IRS. | Need to refinance a loan (e.g., a mortgage) to pay the tax debt. | Another creditor's claim moves ahead of the IRS, enabling refinancing. |

Each path—from a straightforward payment to a strategic subordination—offers a distinct advantage. The key is to match the solution to your specific financial goals and circumstances.

Negotiating a Resolution When You Cannot Pay in Full

For most Michigan taxpayers, the thought of paying off a significant tax debt in one shot is completely unrealistic. When a tax lien is involved, it’s easy to feel backed into a corner. But this is exactly the point where negotiation becomes your best move. Both the IRS and the Michigan Department of Treasury have programs specifically for people who can't pay their full tax bill right away.

These options aren't loopholes; they are legitimate pathways to resolving your debt, stopping aggressive collection efforts, and finally getting that tax lien off your property. The trick is to present your financial situation clearly and honestly.

Settling for Less with an Offer in Compromise

Think of an Offer in Compromise (OIC) as a settlement. It’s an agreement with the IRS to resolve your tax liability for less than the full amount owed. But let's be clear: this isn't for everyone. It’s designed for taxpayers facing genuine financial hardship. You have to prove that paying the full amount would create a legitimate economic crisis for you and your family.

The process starts with IRS Form 656, a package that demands a deep dive into your financial life. You'll need to disclose everything—income, expenses, the equity in your assets, and what you could reasonably earn in the future. The IRS crunches these numbers to determine your "reasonable collection potential" (RCP), which is the absolute most they think they can get from you.

Key Takeaway: The IRS won't even consider an OIC if they think you can pay the debt in full, either now or over time through a payment plan. Your offer has to be at least as much as your calculated RCP.

Successfully getting an OIC approved requires meticulous preparation. For example, a Detroit small business owner I worked with was drowning in payroll tax debt. We had to present a complete financial picture—profit and loss statements, balance sheets, and a compelling story about how a major client's bankruptcy crippled their cash flow. Or consider a family in Lansing I helped whose income was slashed due to an unexpected medical diagnosis. We documented every single medical bill and the reduced paychecks to justify their offer. You can learn more about the specifics of this powerful tool by exploring our detailed guide on what an Offer in Compromise entails.

Paying Over Time with an Installment Agreement

If an OIC isn’t a good fit, an Installment Agreement (IA) is often the next best move. It's a straightforward plan to pay your tax debt through manageable monthly payments, typically stretching up to 72 months. For many people, this is a much more achievable way to get back in compliance and work toward getting the lien removed.

Compared to an OIC, setting up an IA is much simpler. If your total bill (tax, penalties, and interest combined) is under $50,000, you might even qualify for a streamlined agreement online without having to submit a mountain of financial paperwork.

The real game-changer with an IA is the potential for a lien withdrawal. After you’ve made three consecutive, on-time payments, you can actually ask the IRS to withdraw the Notice of Federal Tax Lien. If they agree, the public notice is removed as if it never happened. This is huge for your credit and financial reputation.

Building Your Financial Case

Whether you're aiming for an OIC or an IA, the strength of your argument comes down to your paperwork. You need to paint an accurate and compelling picture of your financial reality for the tax authorities.

Essential Documentation Checklist

- Proof of Income: Your most recent pay stubs, W-2s, 1099s, or if you're a business owner, profit and loss statements.

- List of Monthly Expenses: Think housing, utilities, groceries, car payments, insurance, healthcare—all the necessary costs of living. Be realistic and don't leave anything out.

- Asset Information: A clear list of bank accounts, investments, real estate, vehicles, and any other property of value.

- Liability Records: Gather statements for your mortgage, auto loans, student loans, credit cards, and any other debts you have.

When you pull this all together, complete honesty is non-negotiable. The IRS and the Michigan Treasury can verify nearly everything you submit. Finding discrepancies will get your proposal rejected fast and could even invite more scrutiny. Your best strategy is always to be transparent, organized, and proactive. Show them you're willing to resolve the debt within your means, and you’ll be on the right track.

Are There Special Circumstances That Can Invalidate a Lien?

While most tax liens are the result of straightforward, undisputed debt, some cases are far from black and white. Life is messy. Fortunately, tax laws recognize this and provide specific, powerful avenues to challenge or even completely invalidate a lien under the right circumstances.

Think of these as built-in protections for taxpayers who have been unfairly caught in the crossfire of tax issues they didn't create or are no longer legally on the hook for. For some Michigan residents, understanding these rules is the most direct path to a resolution, sometimes sidestepping the need for payment plans altogether.

Innocent Spouse Relief: When You're Unfairly Held Responsible

Sharing your life and finances with a spouse shouldn't mean being held liable for their tax evasion or deliberate mistakes. That's the principle behind Innocent Spouse Relief, a crucial provision designed to protect people from joint tax liabilities they were completely unaware of. If a tax lien landed on your doorstep because of an understatement of tax on a joint return, you may have a way out.

Qualifying isn't a given, but you stand a good chance if you can show the IRS that:

- You filed a joint return that has an understated tax amount.

- This understatement is entirely due to "erroneous items" from your spouse (or ex-spouse).

- When you signed the return, you genuinely did not know—and had no reason to know—about the understatement.

- Given everything, it would be fundamentally unfair to hold you responsible for the debt.

To start this process, you must file IRS Form 8857, Request for Innocent Spouse Relief. This isn't just a form; it's your opportunity to tell your side of the story, backed by documentation. For instance, if your former spouse was hiding business income from you, providing bank statements or other evidence showing your limited role in their finances can make all the difference. Successfully navigating this can feel like untangling a very complicated knot, but the relief is immense.

If you find yourself dealing with other tax discrepancies alongside this, you may also want to understand how to dispute a tax assessment in Michigan.

Identity Theft: When the Tax Debt Isn't Even Yours

There are few things more alarming than discovering a tax lien you know nothing about. In some cases, the culprit is a criminal. If an identity thief used your Social Security number to earn income or file a fraudulent tax return, the resulting tax debt and lien are not your legal responsibility. But it won't disappear on its own—you have to take specific, immediate action.

Your first move is to file IRS Form 14039, Identity Theft Affidavit. This is the official signal to the IRS that you've been a victim of fraud. It triggers an investigation to clear your name and your tax record. You'll need to work with them to prove your identity and sort out which tax filings are real and which are fake.

Expert Tip: While the IRS is investigating the fraud, it's absolutely critical to keep up with your own legitimate tax obligations. Continue to file your personal tax returns and pay any taxes you actually owe on time. This shows good faith and helps the IRS more easily separate your valid tax history from the criminal activity.

Clearing your record can be a slow process, but it's worth it. Once the IRS confirms the identity theft, they will remove the fraudulent debt and any related tax liens from your account, restoring your good name.

The Statute of Limitations: When the Clock Runs Out

The government doesn't have forever to collect a tax debt. Both the IRS and the Michigan Department of Treasury operate under a strict statute of limitations. For the IRS, this collection window is typically 10 years from the date the tax was officially assessed.

This deadline is known as the Collection Statute Expiration Date (CSED). Once that date passes, the IRS legally loses its authority to collect from you. They can't file new liens or levy your bank accounts. If a lien was already in place, it becomes unenforceable, and you can formally request its release.

It sounds simple, but calculating the CSED can be surprisingly complex. Certain actions can "toll" or pause the 10-year clock, effectively extending the collection period. Common triggers for this include:

- Filing for bankruptcy

- Requesting an Installment Agreement

- Submitting an Offer in Compromise

- Living outside the United States for an extended time

Because of these potential pauses, you can't just add ten years to the date on your first notice. A tax professional can pull your official IRS account transcript to calculate the true CSED, helping you determine if the statute of limitations is your key to finally getting that lien removed.

Your Practical Checklist for the Lien Removal Process

When you're facing a tax lien, the path to removal can feel overwhelming. The key is breaking it down into manageable steps. This checklist is your roadmap, designed to keep you organized from the moment you discover the lien to the day it's finally resolved.

Think of this as more than just paperwork. It's about methodically building a clear, credible case for the tax authorities. Every document you gather and every form you complete tells a piece of your financial story, so let's make sure it's a compelling one.

First, Assemble Your Core Documentation

Before you can even think about negotiating or filing requests, you need a complete and accurate picture of your financial situation. This is where the real work begins—gathering the raw materials for your case. I've seen countless people make the mistake of rushing this step, only to face frustrating delays and rejections later.

Here’s what you need to start gathering:

- All Tax Notices: This is non-negotiable. Find every single letter you've received from the IRS or the Michigan Department of Treasury. The original Notice of Federal Tax Lien (NFTL) is especially critical.

- Proof of Income: Get at least three months of your most recent pay stubs. If you're self-employed, you'll need current profit and loss statements.

- Bank and Asset Statements: Print out recent statements from every account you have—checking, savings, and investments. You'll also need fair market valuations for major assets like your home, vehicles, or other property.

- Expense Records: Create a detailed list of your monthly household expenses. Back this up with actual bills for your mortgage or rent, utilities, insurance premiums, and any loan payments.

Having this information organized and ready will dramatically speed up the process, whether you’re applying for an Installment Agreement yourself or working with a professional. It demonstrates to the tax agency that you are serious and prepared.

Next, Identify and Complete the Right Forms

With your documentation in hand, it's time to translate that information onto the correct government forms for your chosen strategy. Each form serves a very specific purpose, and submitting the right one is absolutely essential. Trust me, sending in the wrong paperwork is one of the quickest ways to get your request denied.

To help you get started, I've put together a quick summary of the most common forms you'll likely encounter.

Required Forms and Their Purpose

This table outlines the key IRS forms used in the tax lien resolution process.

| Form Number | Form Title | Primary Use |

|---|---|---|

| Form 12277 | Application for Withdrawal of Filed Notice of Federal Tax Lien | This is what you use to request the complete removal of the public NFTL notice from your record. |

| Form 656 | Offer in Compromise | Use this form to formally propose settling your tax debt for less than the full amount you owe. |

| Form 9465 | Installment Agreement Request | This is the standard form for setting up a monthly payment plan for your outstanding tax liability. |

| Form 8857 | Request for Innocent Spouse Relief | If your liability was created by a spouse or ex-spouse, this form is used to seek relief. |

Knowing which form to use is half the battle. Filling it out completely and accurately is the other half.

Finally, Know When to Call for Professional Help

While a DIY approach can work for simple, straightforward cases, tax issues can get complicated fast. It's incredibly important to recognize the signs that you're in over your head and need an experienced tax attorney in your corner.

You should seriously consider professional help if any of these apply to you:

- Your total tax debt is over $50,000.

- The IRS has already rejected your Offer in Compromise or Installment Agreement.

- You're dealing with payroll tax liabilities for a business—these are a high priority for the IRS.

- You need to sell property with a lien attached and require an urgent discharge or subordination to close the deal.

Bringing in a firm like Defense Tax Partners gives you an advocate who understands Michigan's specific enforcement trends and can negotiate directly with revenue officers on your behalf. After a lien is removed, ensuring your property is marketable often involves sorting out title health and protections like Lender's Title Insurance—an area where professional guidance is invaluable.

Don't wait until the situation becomes unmanageable. Proactive representation is always your strongest defense.

Common Questions About Michigan Tax Liens

When you’re staring down a tax lien, it’s natural for questions and a sense of uncertainty to start piling up. It's a high-stakes situation, and you need clear, straightforward answers to make the right moves. Let's walk through some of the most common questions we hear from taxpayers here in Michigan.

How Long Does It Take to Remove a Lien After Payment?

This is usually the first thing people want to know. After you've paid off your tax debt in full, the IRS is legally required to issue a Certificate of Release of Federal Tax Lien within 30 days. The Michigan Department of Treasury operates on a similar schedule for state tax liens.

But here’s a crucial detail many people miss: releasing the lien just means the debt is satisfied. It doesn't actually wipe the public record clean. If your goal is to have the Notice of Federal Tax Lien (NFTL) completely removed from your credit history, you'll need to apply for a lien withdrawal. That’s a separate process and, from my experience, it can easily take several months to complete.

What Is the Difference Between a Lien and a Levy?

It’s incredibly important to understand this distinction because the two are often confused, and a levy is a far more immediate threat.

- A Tax Lien is a legal claim the government places on your property. It’s like a public notice that secures their interest in your assets—your house, your car, your business—but it doesn't take them away.

- A Tax Levy is the next step: the actual seizure of your property to pay the debt. This is when the IRS or the state takes money from your bank account, garnishes your wages, or seizes physical assets. A lien almost always precedes a levy.

Can the IRS Refile a Lien After It's Been Released?

Yes, they can, but only in very specific situations. Typically, a lien release is final once the debt is paid off or becomes legally uncollectible, like when the 10-year statute of limitations runs out.

The big exception is when a release was issued by mistake, or if a taxpayer defaults on a settlement like an Offer in Compromise. If that happens, the IRS can revoke the release and put the lien right back in place. This is why it is absolutely critical to stay compliant with any agreement you make.

Will a Tax Lien Stop Me from Selling My House in Michigan?

A tax lien will absolutely complicate a home sale, but it doesn't have to be a complete deal-breaker. The main issue is that you can’t give the buyer a clear title while an active lien is attached to the property.

You have a couple of solid options to get the sale done. The most direct approach is to use the proceeds from the sale to pay the tax debt in full at closing. Another path is to apply for a Certificate of Discharge. This is a great tool that removes the lien from just the house you're selling, allowing the sale to go through while the lien stays attached to any other assets you own.